ChangXin Memory Technologies, better known as CXMT, is China’s largest producer of DRAM memory chips. It is also becoming an increasingly important competitor to Samsung Electronics, SK Hynix and Micron Technology, the three companies that have traditionally dominated the global DRAM market.

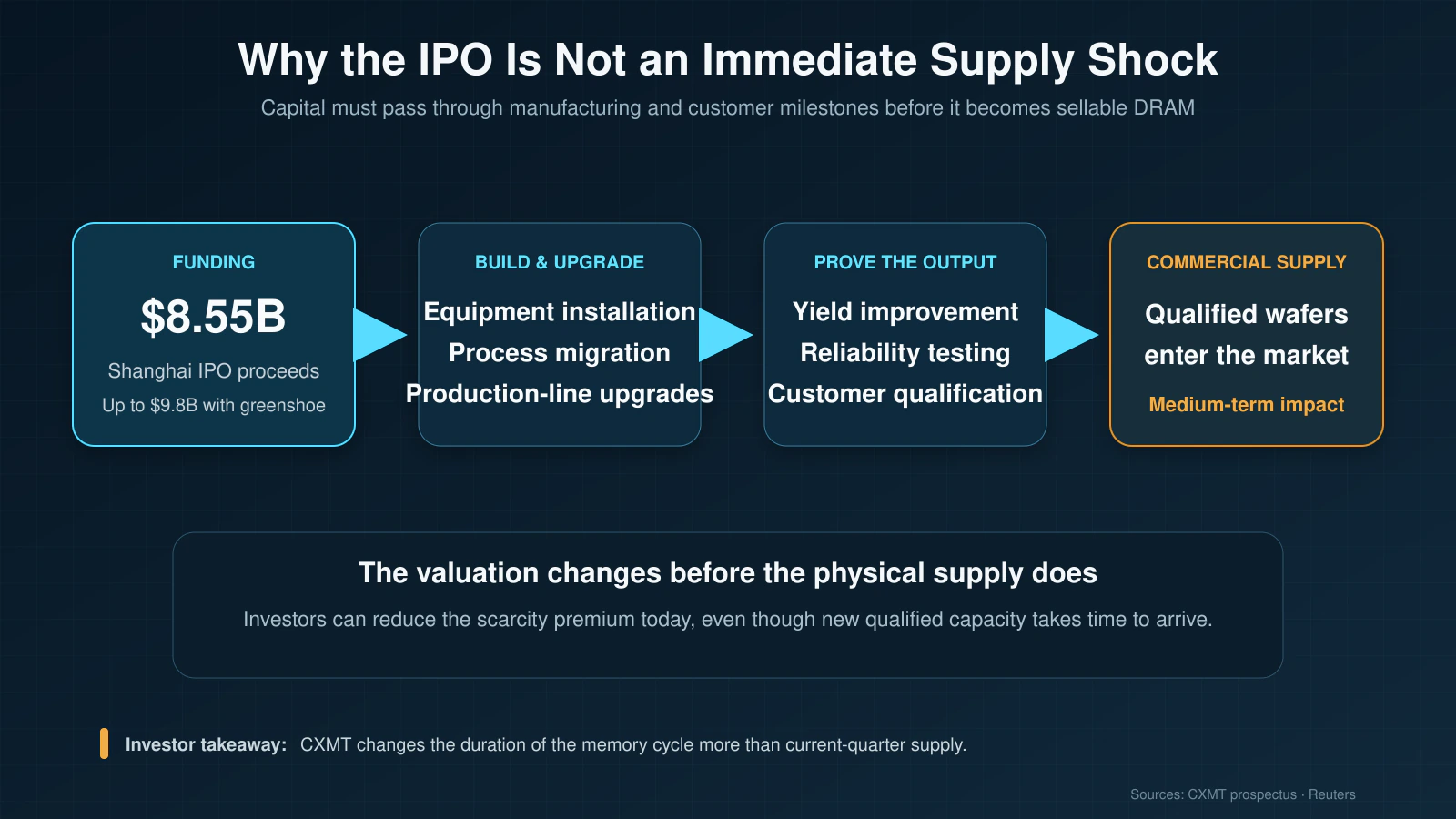

CXMT is preparing for a major listing on the Shanghai Stock Exchange. The IPO could raise about $8.55 billion, or as much as approximately $9.8 billion if the overallotment option is exercised. That would give the company more capital to expand production and improve its technology.

But CXMT should not be confused with an immediate replacement for the established memory leaders. Its strongest products are mobile and conventional DRAM, while the AI memory boom is being driven mainly by high-bandwidth memory, or HBM. That distinction is essential for understanding both CXMT’s opportunity and its limitations.

Key Takeaways

- CXMT is China’s largest DRAM producer and was the world’s fourth-largest supplier by 2025 market share.

- The company’s strongest business is LPDDR mobile memory, followed by conventional DDR memory.

- CXMT has entered mass production of products including DDR5, LPDDR5 and LPDDR5X.

- It does not yet have disclosed commercial HBM production comparable with SK Hynix, Samsung or Micron.

- Its planned IPO could accelerate future capacity growth, but new funding will not create qualified supply overnight.

- CXMT presents the greatest competitive pressure in Chinese mobile, PC and conventional server memory markets—not yet at the leading edge of AI memory.

What Does CXMT Do?

CXMT designs and manufactures DRAM, the working memory used by smartphones, personal computers, servers and other electronic devices. Unlike NAND flash, which stores data after power is removed, DRAM provides the high-speed temporary memory that processors need while applications are running.

The company is an integrated device manufacturer. That means it performs both chip design and manufacturing rather than outsourcing all production to an external foundry.

CXMT’s strategic importance extends beyond its current revenue. China remains heavily dependent on imported advanced semiconductors, and memory is one of the largest segments of the global chip market. A domestic DRAM manufacturer therefore supports both China’s industrial policy and its effort to reduce reliance on overseas suppliers.

How Large Is CXMT?

According to information disclosed in its Shanghai Stock Exchange prospectus, CXMT held approximately 7.7% of the global DRAM market in 2025, making it the fourth-largest producer after Samsung, SK Hynix and Micron.

That position is meaningful, but the gap between fourth place and the three leaders remains substantial. Samsung, SK Hynix and Micron still control most global DRAM production, possess deeper customer relationships and lead in important advanced products.

CXMT’s scale is nevertheless large enough to affect pricing and purchasing decisions, particularly in China. Its significance should therefore be measured not only by global market share but also by where its capacity competes most directly.

What Memory Products Does CXMT Sell?

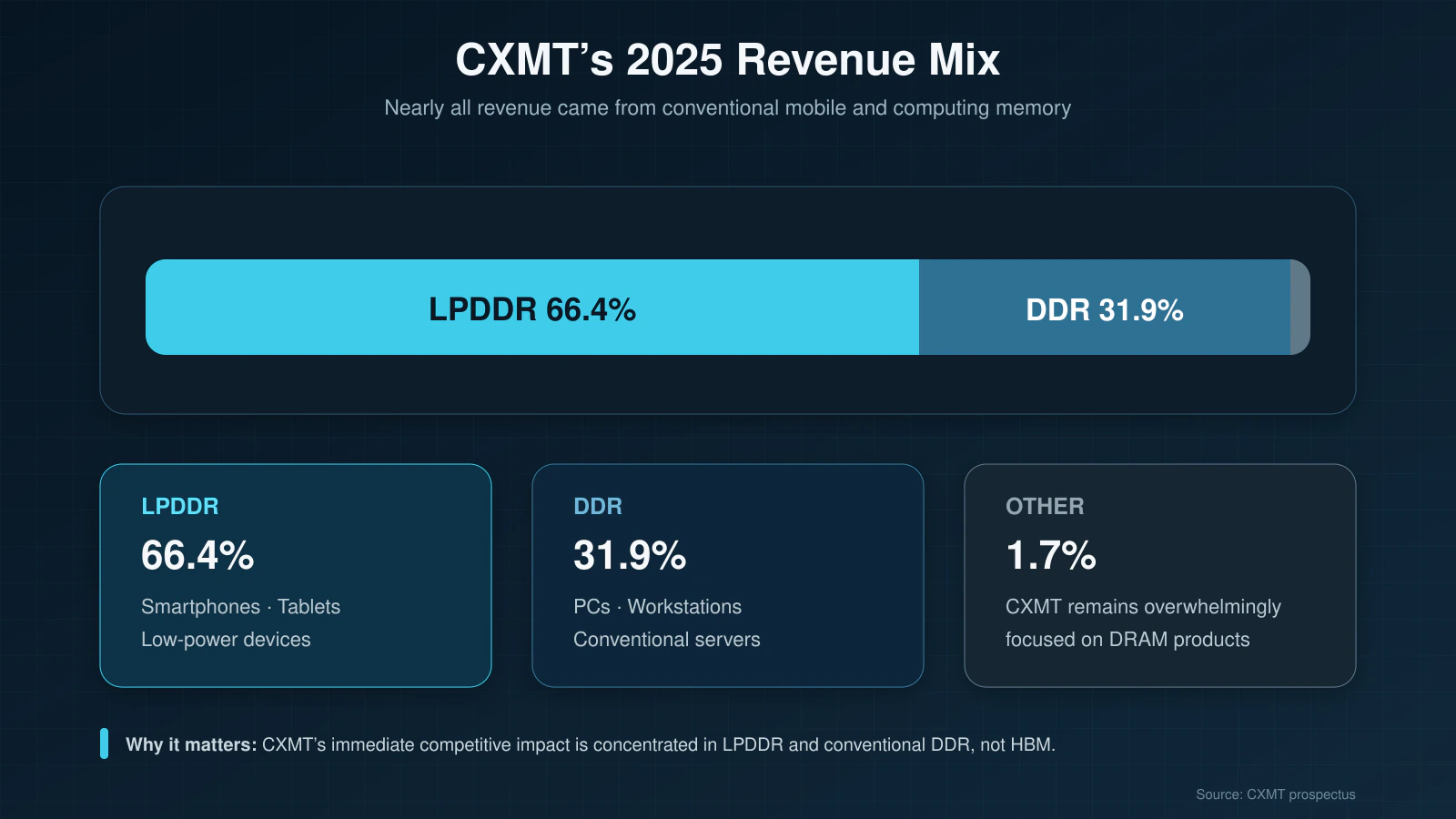

CXMT’s revenue mix shows that it is primarily a mobile and conventional DRAM supplier. LPDDR products, which are designed for smartphones and other power-sensitive devices, generated 66.4% of its 2025 revenue. Standard DDR products, the conventional DRAM used in PCs, workstations and many servers, contributed another 31.9%, while other products accounted for only 1.7%.

The company has announced mass production of newer products including DDR5 and LPDDR5X. These developments narrow part of the technology gap with international competitors and allow CXMT to address higher-performance phones, computers and servers.

However, product labels alone do not prove equal performance or economics. Investors must still consider manufacturing yield, power efficiency, chip density, customer qualification and the ability to produce consistently at large scale.

Does CXMT Produce HBM?

CXMT has discussed advanced memory development, but it has not disclosed commercial HBM production on a scale comparable with SK Hynix, Samsung or Micron.

HBM is not simply ordinary DRAM sold at a higher price. It requires advanced dies, complex stacking, through-silicon vias, sophisticated packaging and close qualification with AI accelerator companies. Success depends on an ecosystem of manufacturing and supply bottlenecks that extends beyond the DRAM fabrication process itself.

This is why CXMT’s expansion does not automatically imply an immediate oversupply of AI memory. It can increase competition in DDR and LPDDR before it becomes a major threat in HBM.

SK Hynix currently has the strongest competitive position in HBM, while Samsung and Micron are spending heavily to expand their own advanced-memory businesses. CXMT remains more relevant to conventional DRAM pricing than to the near-term supply of memory used with leading AI accelerators.

Who Buys CXMT Memory?

CXMT primarily serves the Chinese market, where domestic electronics manufacturers and technology companies have strong incentives to diversify their semiconductor supply chains.

Reuters reported that CXMT secured a memory supply agreement with Tencent worth more than RMB20 billion, or approximately $2.9 billion. A contract of that size would provide demand visibility and demonstrate that large Chinese cloud companies are willing to qualify domestic memory products.

The company can also target smartphone manufacturers, computer producers and other device makers that need LPDDR or DDR memory. Its high LPDDR revenue share shows why mobile customers are especially important.

These orders matter because semiconductor competition depends on more than announced capacity. A memory supplier must prove that its products can satisfy customers’ standards for performance, reliability, volume and delivery consistency.

Why Does Apple Want Access to CXMT?

Apple has reportedly sought permission from the Trump administration to purchase memory from CXMT for devices sold in China. The request has attracted political scrutiny because CXMT is subject to US restrictions and is viewed as strategically important to China’s semiconductor ambitions.

For Apple, using a Chinese memory supplier could reduce costs, diversify sourcing and support products manufactured or sold in China. For CXMT, winning even limited Apple business would be an important validation of its product quality and manufacturing reliability.

The political obstacles are substantial. US lawmakers have urged the administration to prevent American companies from strengthening Chinese semiconductor manufacturers. The outcome will therefore depend on trade and national-security policy as much as on product performance.

The Apple discussion is important, but it should not be interpreted as proof that CXMT has already displaced Samsung, SK Hynix or Micron across Apple’s global supply chain.

When Will CXMT Go Public?

CXMT is expected to list on Shanghai’s STAR Market on July 27 under stock code 688825. The offering is expected to raise approximately $8.55 billion before any additional proceeds from the overallotment option.

The size of the deal reflects both the capital intensity of memory manufacturing and the strategic importance Chinese policymakers attach to domestic semiconductor production.

The IPO could finance new facilities, manufacturing equipment, research and development, and process upgrades. However, investors should distinguish financing from productive capacity. A new factory must be built and equipped, manufacturing yields must improve, and chips must complete customer qualification before they become reliable commercial supply.

The IPO therefore changes the medium-term competitive outlook more than the amount of DRAM available today.

How Could CXMT Affect Samsung, SK Hynix and Micron?

CXMT is likely to create the most direct pressure in mature and mainstream DRAM categories. Its growth could reduce the Chinese market share available to foreign suppliers, make pricing more competitive and limit the benefits of conventional DRAM shortages.

Micron may face particular exposure because US restrictions have already complicated its position in China. Samsung and SK Hynix also sell significant volumes into Chinese electronics and computing markets, although their scale and advanced-memory portfolios provide more diversification.

The competitive effect is not equal across every product:

- In LPDDR, CXMT is already a meaningful competitor because mobile memory represents most of its revenue.

- In conventional DDR, rising Chinese capacity could eventually pressure pricing and market share.

- In server DDR5, CXMT’s position is developing but depends on qualification by demanding enterprise and cloud customers.

- In HBM, the established leaders retain a large technology, packaging and customer-qualification advantage.

That product-by-product distinction is more useful than treating every additional CXMT wafer as an immediate threat to the entire global memory industry.

Could CXMT Cause a DRAM Oversupply?

CXMT could contribute to future oversupply in conventional DRAM, especially if its capacity expands faster than demand in smartphones, PCs and traditional servers. Memory is a cyclical industry, and relatively small changes in supply can produce large movements in prices and profits. Our SK Hynix and Micron memory-cycle analysis examines how those supply decisions can change the investment case.

But an IPO is not itself a supply shock. The timing depends on construction, equipment installation, process yields, product mix and customer acceptance. Export restrictions on advanced semiconductor equipment may also limit the speed at which CXMT can improve manufacturing technology.

Meanwhile, the largest international memory companies are shifting investment toward HBM and other higher-value products for AI systems. That can tighten some conventional DRAM categories even while the industry adds advanced-memory capacity.

The likely outcome is not one uniform memory market. HBM can remain structurally tight while selected DDR or LPDDR products face greater Chinese competition.

What Should Investors Watch Next?

The first issue is CXMT’s capital-spending plan after the IPO. The amount allocated to new wafer capacity matters more than the headline amount raised.

The second is product qualification. Large orders from cloud providers, handset manufacturers or global electronics companies would demonstrate that CXMT can convert manufacturing output into dependable commercial supply.

The third is technology. Investors should watch its progress in DDR5, LPDDR5X, advanced process nodes and eventually HBM. Announcing a product is different from producing it economically at scale.

The fourth is trade policy. US restrictions on equipment, technology and customer relationships could influence CXMT’s growth as much as market demand.

Finally, investors should monitor conventional DRAM prices separately from HBM pricing. CXMT’s near-term influence is much greater in the former.

The Bottom Line

CXMT is no longer a small experimental memory producer. It is the world’s fourth-largest DRAM company, has meaningful mobile and conventional-memory revenue, and is raising enough capital to become a more serious long-term competitor.

However, the company’s current strength should not be mistaken for leadership across the entire memory market. CXMT competes most directly in LPDDR and standard DDR. Samsung, SK Hynix and Micron retain major advantages in HBM, advanced manufacturing, packaging and relationships with global AI customers.

The IPO strengthens China’s ability to challenge the established DRAM industry over time. It does not create an immediate flood of AI memory supply. For deeper analysis of how CXMT changed the market narrative while Korean deleveraging amplified the semiconductor selloff, read CXMT Was the Headline. Korea’s Deleveraging Drove the Selloff.

Frequently Asked Questions

What does CXMT stand for?

CXMT stands for ChangXin Memory Technologies. It is a Chinese semiconductor company that designs and manufactures DRAM memory chips.

Is CXMT publicly traded?

CXMT is expected to list on the Shanghai Stock Exchange’s STAR Market on July 27 under stock code 688825.

Can US investors buy CXMT stock?

CXMT is listing in mainland China rather than on a US exchange. Direct access generally depends on an investor’s broker, jurisdiction and eligibility to trade Shanghai-listed shares.

Who are CXMT’s main competitors?

Its principal global competitors are Samsung Electronics, SK Hynix and Micron Technology. The degree of competition varies by memory product.

Does CXMT manufacture HBM?

CXMT has pursued advanced-memory development, but it has not disclosed commercial HBM output comparable in scale with SK Hynix, Samsung or Micron.

What is CXMT’s global DRAM market share?

CXMT held approximately 7.7% of the global DRAM market in 2025, according to information disclosed around its listing.

Could CXMT hurt Micron?

CXMT could increase competition for Micron in China and in conventional DRAM products. Its near-term threat is less direct in HBM, where Micron and the two Korean leaders remain technologically ahead.

Is CXMT’s IPO an immediate DRAM supply shock?

No. IPO proceeds can finance future expansion, but factories, process yields and customer qualifications take time. The offering has a greater effect on medium-term supply expectations than on current production.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | ChangXin Memory Technologies prospectus | Shanghai Stock Exchange | May 2026 | Prospectus | Company business, 2025 market share, revenue mix and offering disclosures. |

| 2 | China memory chipmaker CXMT sets July 27 listing date | Reuters | July 14, 2026 | News | IPO size, listing date, stock code and estimated DRAM market share. |

| 3 | China’s CXMT wins $3 billion memory supply deal with Tencent | Reuters | June 29, 2026 | News | Tencent supply agreement and customer validation. |

| 4 | Apple seeks approval to buy chips from blacklisted Chinese company | Reuters | June 27, 2026 | News | Apple’s reported request to purchase CXMT memory. |

| 5 | US lawmakers urge Trump administration to ban Chinese memory chips | Financial Times | July 2026 | News | US political response to potential purchases from CXMT. |

| 6 | CXMT launches LPDDR5X | ChangXin Memory Technologies | Current | Company information | LPDDR5X product and mass-production announcement. |

Primary company materials and reputable financial reporting support the market-share, product, customer, policy and IPO details in this guide.

Related Reading

CXMT Was the Headline. Korea’s Deleveraging Drove the Selloff

Why semiconductor stocks fell after strong earnings: CXMT changed the memory supply narrative, while Korea’s leveraged unwind amplified the selloff.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments