Key Takeaways

- CXMT is a credible future competitor in conventional DDR and LPDDR, but it has not yet changed the near-term HBM supply structure.

- Samsung’s blowout earnings failed to lift the shares, showing that exceptional memory pricing and profits were already reflected in expectations.

- Korea’s rate increase, leveraged ETF restrictions and record retail borrowing explain why the adjustment became concentrated and violent.

- TSMC’s higher capital spending confirms AI demand while increasing future depreciation, wafer costs and margin pressure for fabless customers.

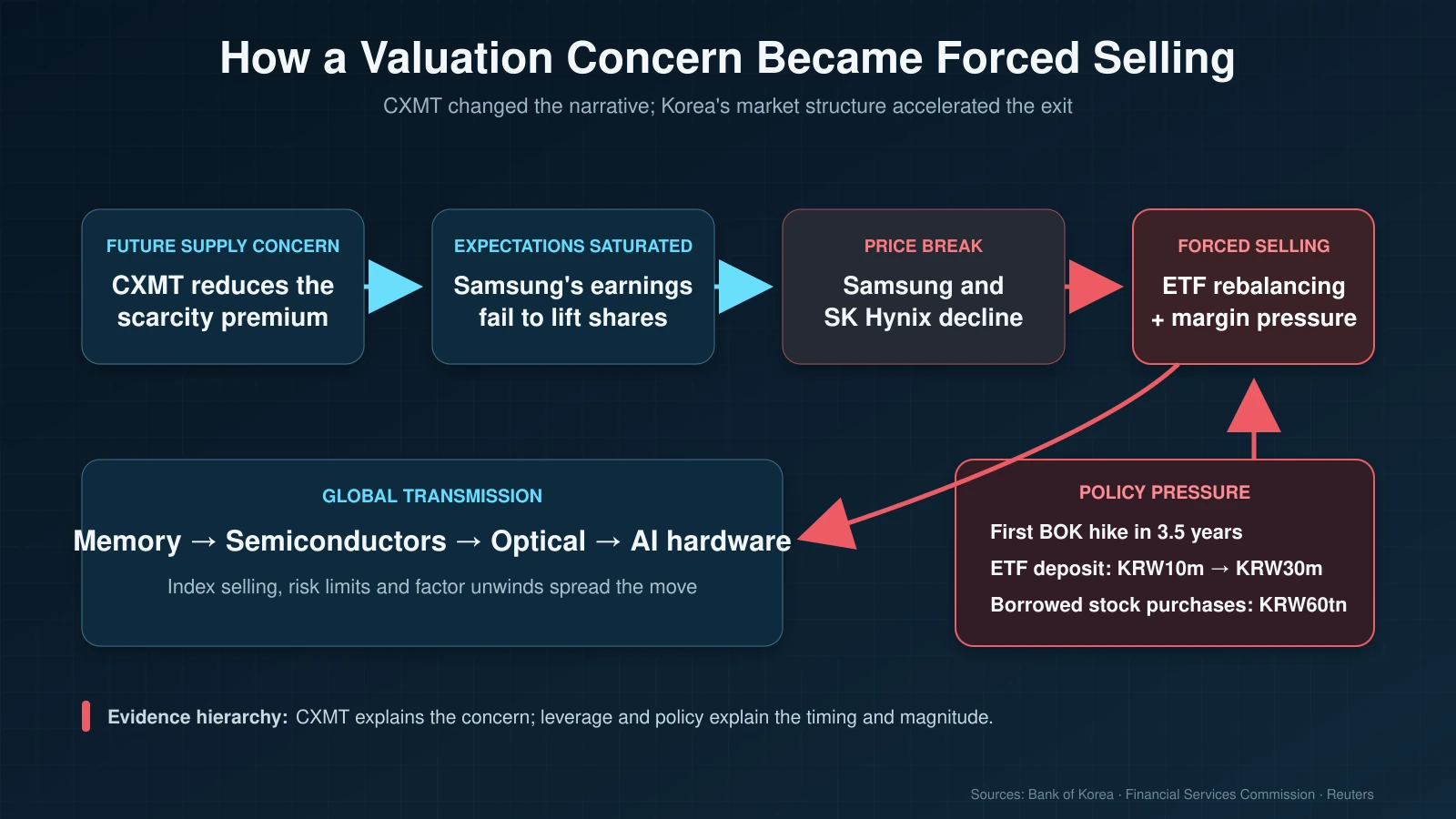

The market has settled on a convenient explanation for the sudden decline in semiconductor stocks: ChangXin Memory Technologies, China’s largest DRAM producer, is raising enough capital to threaten the pricing power of Samsung Electronics, SK Hynix and Micron Technology.

The concern is credible. CXMT expects to raise approximately $8.55 billion in its Shanghai IPO, nearly twice its original target, and could raise as much as $9.8 billion if the overallotment option is exercised. The company was already the world’s fourth-largest DRAM producer in 2025, with an estimated global market share of 7.7%. Its expansion weakens the assumption that the current memory shortage will remain permanent. Reuters

That explains why investors began reconsidering long-term memory valuations. It does not explain why the selloff erupted within a few trading sessions, why Samsung and SK Hynix fell much more than most global peers, or why Marvell Technology and optical-networking companies collapsed alongside DRAM producers.

The evidence points to a more specific sequence. CXMT changed the market’s view of future supply. Samsung’s blowout earnings then revealed that current strength was already fully priced. South Korean monetary and regulatory tightening subsequently forced leveraged investors to reduce exposure, spreading the decline across the global AI-infrastructure trade.

CXMT provided the headline. Korean deleveraging determined the timing and magnitude.

CXMT Challenges the Scarcity Premium, Primarily in Conventional DRAM

CXMT has become a genuine competitor, but the threat varies significantly by product.

CXMT already competes directly in mobile and conventional DRAM. It has achieved mass production of DDR5 and LPDDR5-class products, while its customer base increasingly includes major Chinese smartphone, computer and cloud companies. The company has also reportedly signed a long-term memory supply agreement with Tencent worth more than RMB20 billion, or approximately $2.9 billion. Reuters

This matters because Samsung, SK Hynix and Micron have been redirecting advanced production capacity toward high-bandwidth memory. That shift has tightened the supply of conventional DDR and LPDDR, allowing prices to rise beyond the HBM market. CXMT can fill part of the conventional-memory gap left by the incumbents, eventually limiting their pricing power.

The immediate HBM threat remains much smaller. Competitive HBM production requires advanced DRAM dies, stacking, packaging, thermal management, high yields and lengthy customer qualification. CXMT has not disclosed commercial HBM output on a scale comparable with the three market leaders. Its IPO therefore weakens the broad DRAM scarcity thesis without ending the current shortage of advanced AI memory.

The timing also matters. CXMT is scheduled to list on July 27. IPO proceeds will finance future production upgrades and process development; they will not become finished wafers this quarter. New capacity requires equipment installation, yield improvement and customer validation. The market is reducing the value assigned to future scarcity rather than responding to an immediate surge in supply.

The political debate in Washington has made that future threat more visible. Apple has reportedly sought approval from the Trump administration to purchase memory from CXMT as it looks for relief from rising memory costs. At the same time, bipartisan US lawmakers are urging the administration to block American companies from buying chips from CXMT and NAND producer Yangtze Memory Technologies. Reuters, Financial Times

The two sides are arguing for opposite policies, yet both validate the same investment conclusion: CXMT has become commercially important enough to attract a major US customer and politically significant enough to provoke a bipartisan response. That justifies a lower long-term scarcity premium for conventional memory. It still does not account for the violence of this week’s market move.

Samsung’s Earnings Exposed Saturated Expectations

The next signal came from Samsung. The company estimated second-quarter revenue of KRW171 trillion and operating profit of KRW89.4 trillion, with operating profit rising roughly nineteenfold from a year earlier and exceeding expectations. Estimates cited by Reuters suggested that DRAM and NAND average selling prices increased 44% and 53% quarter over quarter, respectively.

Samsung nevertheless fell 6.9% on the day of the announcement, while SK Hynix lost 6% and the KOSPI declined 4.9%. Samsung had traded down as much as 10% during the session. Reuters

That reaction was more important than the earnings beat. It showed that investors had already priced in extraordinary current conditions. Samsung confirmed that memory pricing and profits were exceptionally strong, but the market had moved on to a harder question: how long could those conditions last once high returns attracted additional supply?

Samsung and CXMT represented two sides of the same cycle. Samsung demonstrated how profitable the shortage had become. CXMT demonstrated how those profits were beginning to finance a competitive response.

The failure of record earnings to generate further upside also indicated that the trade had become crowded. Once a near-perfect quarter could no longer attract incremental buyers, momentum investors began protecting gains and leveraged investors became more vulnerable to any additional decline.

Valuation pressure explains why the stocks were ready to fall. South Korea’s market structure explains why the decline became disorderly.

South Korea Turned Repricing Into Forced Selling

Samsung and SK Hynix are more than the country’s largest technology companies. They are dominant index weights and the underlying assets for a fast-growing group of single-stock leveraged exchange-traded funds approved in late May.

These funds use derivatives and daily rebalancing to produce multiples of the underlying shares’ daily returns. When Samsung or SK Hynix declines, the funds may need to reduce exposure to maintain their target leverage. That selling pushes the stocks lower, potentially triggering another round of rebalancing.

The leverage extended beyond ETFs. Retail investors’ borrowed stock purchases had reached a record KRW60 trillion by the end of May. Once the two chipmakers began falling, leveraged ETF rebalancing, margin pressure, index selling and foreign outflows began reinforcing one another.

Policy then tightened on two fronts. On July 16, the Bank of Korea raised its benchmark rate by 25 basis points to 2.75%, its first increase in three and a half years, and indicated that further increases could follow. The KOSPI fell more than 6% during the session, led by renewed selling in chipmakers. Reuters

On the same day, South Korea’s Financial Services Commission suspended new listings of single-stock leveraged ETFs and announced that the minimum cash balance required to trade them would rise from KRW10 million to KRW30 million. Regulators acknowledged that the products had been approved too hastily and identified frequent, large rebalancing trades as a contributor to market volatility. Reuters

Neither institution ordered investors to sell. The central bank nevertheless raised the cost of money just as the securities regulator increased the cost of maintaining leveraged exposure. Investors had a clear incentive to reduce positions before the new requirements took effect.

This sequence explains why the largest declines appeared in South Korea and why they were concentrated within a few trading sessions. CXMT had changed the long-term supply narrative, but no equivalent change had occurred in current memory demand. The sudden variable was the funding environment surrounding two heavily leveraged index leaders.

The second phase of the selloff was therefore better understood as policy-induced deleveraging than as a conventional earnings downgrade.

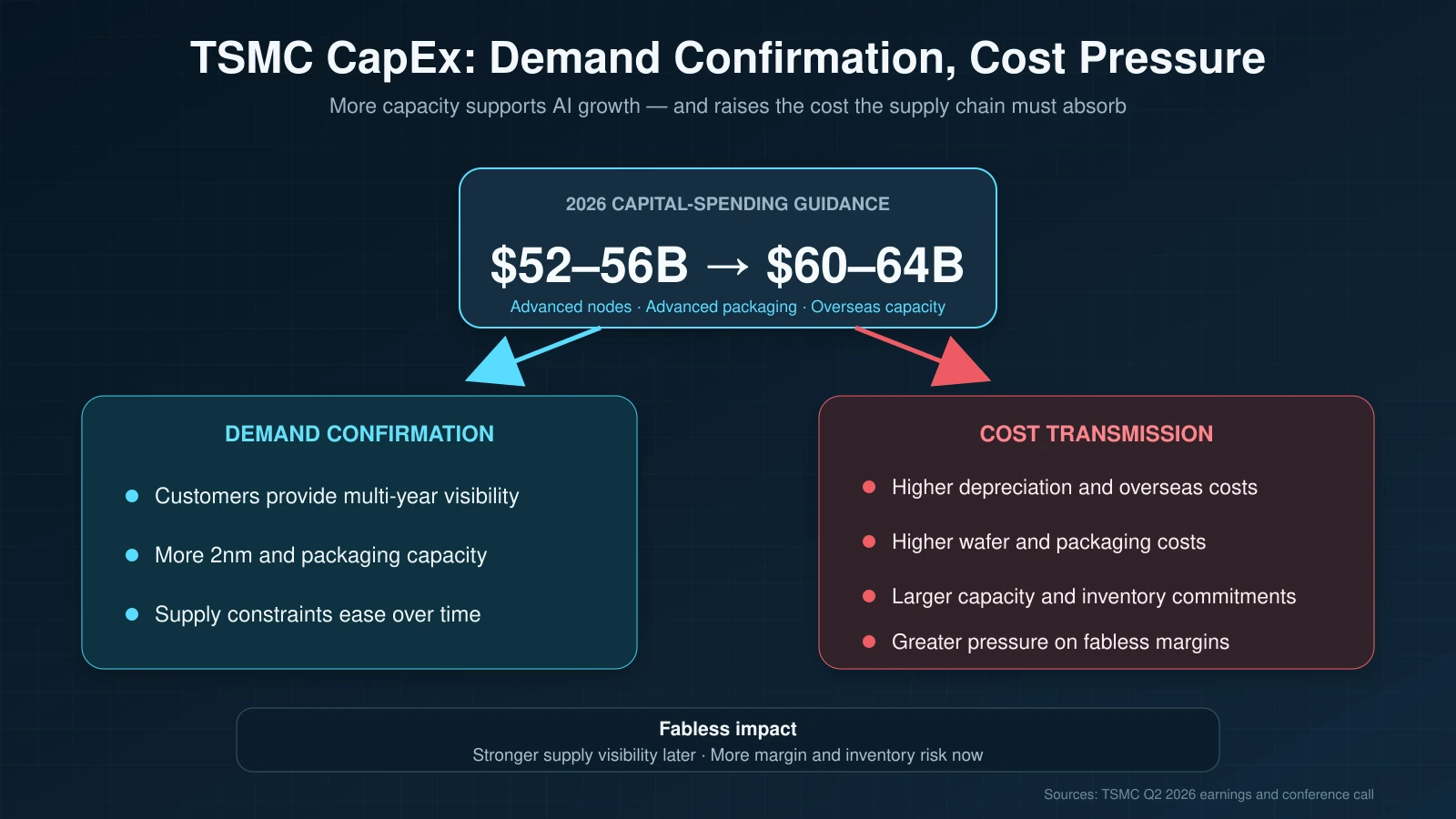

TSMC’s Beat Came With a Cost Warning

Taiwan Semiconductor Manufacturing Company’s results confirmed that leading-edge AI demand remains strong. Second-quarter revenue rose 36%, net profit increased 77%, and the company raised its full-year revenue growth outlook. High-performance computing accounted for 66% of revenue, while advanced nodes represented 77% of wafer sales.

The more consequential signal was the increase in 2026 capital-spending guidance from $52–56 billion to $60–64 billion, alongside another $100 billion commitment to US production. TSMC

For TSMC, the spending confirms that customers are providing enough visibility to justify further investment in 2-nanometer production, advanced packaging and overseas capacity. It also increases future depreciation and exposes the company to the higher cost of manufacturing in the United States. TSMC’s current 67.7% gross margin remains exceptional, but investors are beginning to question how much further it can rise as overseas capacity expands.

The implications extend to fabless customers such as Nvidia, AMD, Broadcom and Marvell. Additional capacity should eventually ease supply constraints, but it may come with higher wafer and advanced-packaging costs, larger capacity commitments and greater inventory risk. Companies with strong pricing power can pass those costs through; those relying on future custom-chip volumes are more exposed to margin pressure.

TSMC’s report therefore carried two messages. Current AI demand remains strong, while the cost of serving that demand is rising across the supply chain. That supports a lower valuation for some future fabless earnings, particularly where margins and order visibility are less secure.

It still does not support the idea that AI orders have suddenly collapsed. ASML reached a similar conclusion from the equipment side: quarterly revenue was €9.3 billion, full-year guidance was raised, and memory-related revenue is expected to grow approximately 75% this year. Customers continue to accelerate capacity additions in both DRAM and advanced logic. ASML

The financial reports provide a reason to debate future returns and supply. They provide little evidence of an immediate demand shock large enough to match the stock-price declines.

Marvell and Optical Stocks Reveal a Broader Unwind

The breadth of the selling provides the strongest evidence against the view that CXMT or memory supply alone caused the decline.

If investors were reacting primarily to future Chinese DRAM capacity, the largest losses should have remained concentrated in conventional memory producers. Instead, the selloff spread to optical components, networking chips, custom AI silicon and semiconductor equipment.

Marvell fell about 9% on July 16 and was down approximately 37% for the month. Coherent, Lumentum and other optical-networking companies also suffered large declines. MarketWatch

These companies do not compete with CXMT, and their businesses are not determined by conventional DRAM supply. Their simultaneous decline indicates that investors were reducing a broader AI-infrastructure factor.

Global portfolios commonly hold memory, foundry, semiconductor equipment, networking and optical-interconnect companies as beneficiaries of the same hyperscaler capital-expenditure cycle. Once Samsung and SK Hynix broke down and risk limits were breached, investors reduced the entire basket.

Marvell was especially vulnerable because a substantial portion of its valuation depends on profits expected from future custom AI accelerators, switching chips and optical-connectivity programs. TSMC has already captured manufacturing profits, and Nvidia has already converted AI demand into substantial revenue. Much of Marvell’s expected upside still depends on future program ramps. A higher discount rate therefore produces a much larger valuation effect.

This does not mean that every AI hardware stock is mispriced. Optical and networking companies still face legitimate questions about customer concentration, competition, capacity expansion and how much 2027 demand is already reflected in their valuations. The price action nevertheless moved far faster than company-specific earnings estimates, which is consistent with factor liquidation and forced selling.

Hyperscaler Earnings Will Decide the Next Phase

The major cloud companies’ earnings at the end of the month will provide the first meaningful test of whether this remains a positioning correction or develops into a fundamental downturn.

Headline capital expenditure alone will not settle the issue. Investors need to know whether incremental AI spending is still accelerating, whether that spending is being funded by operating cash flow or greater borrowing, and whether AI revenue and utilization are increasing quickly enough to absorb depreciation, energy and operating costs.

Guidance will matter more than the reported quarter. If the hyperscalers maintain their infrastructure plans, disclose stronger AI monetization and continue making firm forward commitments, the argument for an immediate semiconductor downturn will weaken. The current selloff would then look increasingly like a valuation reset amplified by Korean deleveraging.

If they begin delaying data-center projects, reducing chip orders or emphasizing capital discipline, the market will finally have evidence that the weakness is moving from positioning into earnings.

For now, the available evidence supports a more precise conclusion. CXMT has reduced confidence in the permanence of conventional-memory scarcity. Samsung’s earnings showed that exceptional current profits were already priced in. TSMC’s capital-spending increase raised legitimate concerns about future depreciation, wafer costs and fabless margins.

Those developments explain why investors were willing to reduce semiconductor valuations. South Korea’s rate increase, leveraged ETF restrictions and concentrated market structure explain why they were forced to do so at once.

CXMT changed the narrative. TSMC raised the cost question. Korean deleveraging drove the selloff. The hyperscalers will determine whether the fundamentals eventually follow.

Frequently Asked Questions

Did CXMT cause the semiconductor selloff?

CXMT weakened the market’s long-term memory scarcity thesis, particularly in conventional DDR and LPDDR. Its future capacity does not explain the speed, timing or breadth of the decline. Korean policy tightening and leveraged selling were the more immediate amplifiers.

Is CXMT already a major threat in HBM?

CXMT is a meaningful competitor in conventional DRAM, but it has not disclosed commercial HBM production comparable with SK Hynix, Samsung or Micron. Its near-term impact is therefore greater in LPDDR and DDR5 than in advanced AI memory.

Why did TSMC fall after strong earnings?

TSMC confirmed strong AI demand but raised 2026 capital-spending guidance from $52–56 billion to $60–64 billion. The higher spending increases future capacity while also raising depreciation, overseas manufacturing costs and potential wafer and packaging costs for fabless customers.

What will determine whether this becomes a fundamental downturn?

The next evidence will come from hyperscaler earnings, DRAM and HBM contract prices, equipment orders and foundry utilization. Order cancellations, delayed data-center projects or sustained cuts to cloud capital expenditure would indicate that the weakness is moving from positioning into earnings.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | China memory chipmaker CXMT aims to raise $8.6 billion in Asia’s biggest IPO of 2026 | Reuters | July 14, 2026 | News | IPO size, listing date and estimated DRAM market share. |

| 2 | China’s CXMT wins $3 billion memory supply deal with Tencent | Reuters | June 29, 2026 | News | Tencent supply agreement and customer validation. |

| 3 | Apple seeks approval to buy chips from blacklisted Chinese company | Reuters | June 27, 2026 | News | Apple’s reported request to purchase CXMT memory. |

| 4 | US lawmakers urge Trump administration to ban Chinese memory chips | Financial Times | July 16, 2026 | News | Bipartisan pressure to restrict purchases from CXMT and YMTC. |

| 5 | Samsung flags 19-fold jump in profit, but shares slump | Reuters | July 7, 2026 | News | Samsung earnings, memory pricing and post-earnings share reaction. |

| 6 | BOK hikes rates for first time in three and a half years | Reuters | July 16, 2026 | News | Bank of Korea rate increase and market reaction. |

| 7 | South Korea to ban new listings of single-stock leveraged ETFs | Reuters | July 16, 2026 | News | ETF restrictions, higher minimum deposits and borrowed stock purchases. |

| 8 | Quarterly Results | TSMC | Q2 2026 | Company IR | Revenue, margins, HPC mix, advanced-node mix and capital-spending guidance. |

| 9 | Financial Results | ASML | Q2 2026 | Company IR | Revenue outlook, memory demand and equipment-capacity expansion. |

| 10 | Semiconductor stocks slump with Marvell under heavy selling pressure | MarketWatch | July 16, 2026 | News | Marvell’s decline and broader semiconductor selling. |

Inline citations remain visible in the article. The table below records the source, publication date, and claim supported.

Related Reading

SK Hynix Comes to Nasdaq. What It Means for Micron

SK Hynix’s Nasdaq debut ends Micron’s trading scarcity. The harder question is which company can preserve pricing power when new memory supply arrives in 2028.

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

AI Semiconductors Are No Longer Just About Compute. They Are About System Bottlenecks.

AI semiconductors are no longer just about raw compute. The real question is which system bottlenecks customers must solve next.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security.

Comments