For years, U.S. investors looking for direct exposure to the memory industry had one obvious choice: Micron Technology.

Samsung Electronics and SK Hynix controlled larger portions of the global memory market, but both remained primarily listed in South Korea. That gave Micron two distinct sources of scarcity. It was one of the world’s three major DRAM manufacturers, and it was effectively the only large pure-play memory producer that U.S. investors could buy easily.

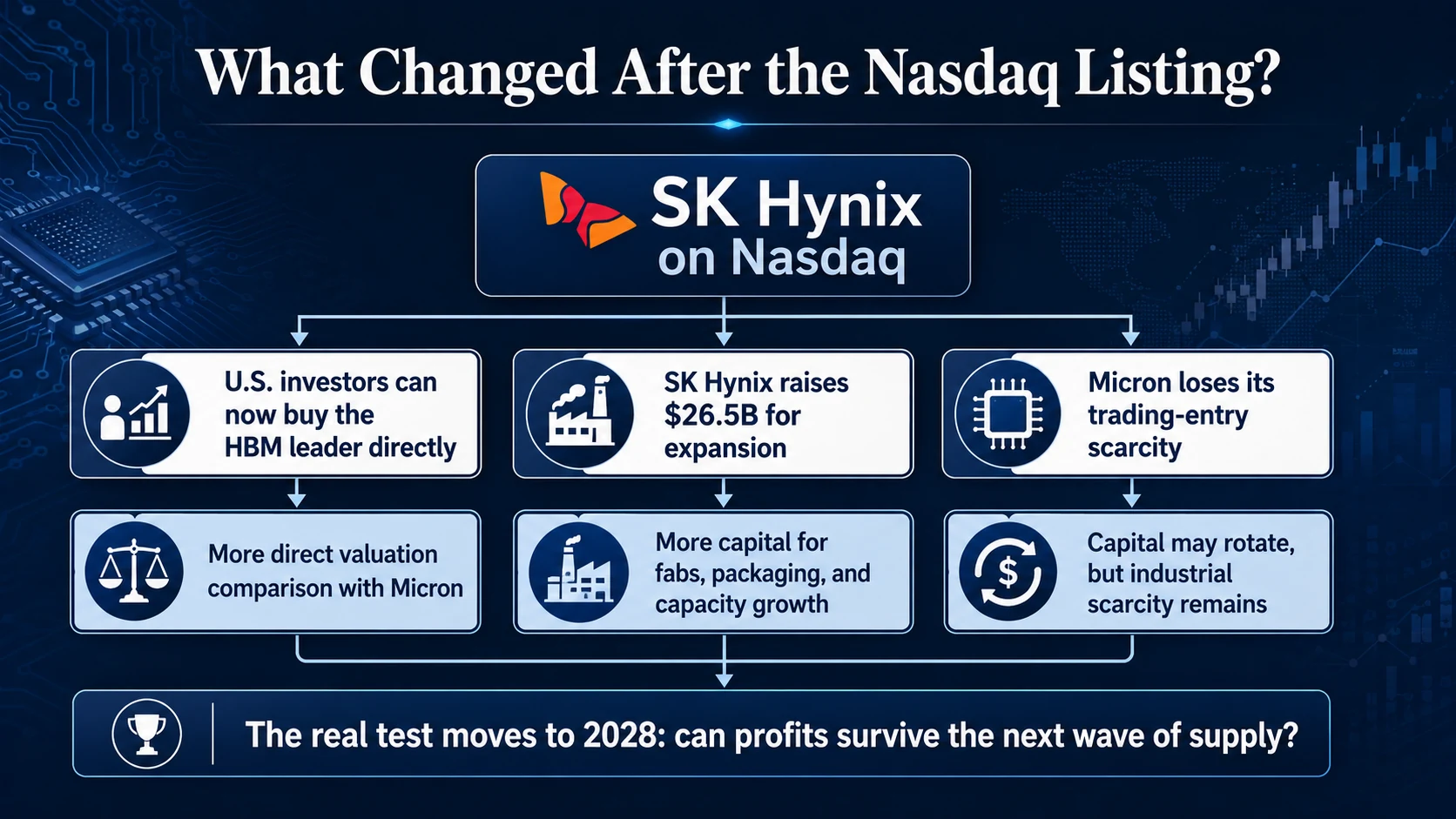

SK Hynix’s Nasdaq listing removes the second advantage.

Readers unfamiliar with the company’s products, ticker and ADS structure can begin with our beginner’s guide to SK Hynix.

The Korean memory manufacturer priced 177.9 million American depositary shares at $149 each, raising approximately $26.5 billion. Ten ADSs represent one Korean ordinary share, meaning the transaction corresponds to 17.79 million newly issued ordinary shares, or roughly 2.5% of the company’s pre-offering share count. Regular trading is set to begin on July 13 under the ticker $SKHY.

This is more than an ADR wrapper placed around existing Korean shares. SK Hynix is issuing new equity and directing the proceeds toward production equipment, new fabrication facilities and advanced semiconductor tools, including EUV lithography systems.

That changes the investment question.

The market is no longer choosing between Micron and indirect exposure to the global memory leaders. U.S. investors can now compare two very different propositions: SK Hynix’s established leadership in high-bandwidth memory and Micron’s combination of rising HBM participation, U.S. manufacturing capacity and strategic importance to American semiconductor policy.

The listing also matters beyond valuation. By raising capital near the top of a powerful memory upcycle, SK Hynix has strengthened its ability to expand wafer production, advanced packaging and NAND capacity. The immediate effect may be a redistribution of investor attention. The more consequential effect may arrive several years later, when that capital turns into additional supply.

Key Takeaways

- SK Hynix’s Nasdaq listing removes Micron’s position as the only easily tradable large memory manufacturer in the U.S. market.

- SK Hynix’s HBM leadership is real, but its earnings still include substantial exposure to conventional DRAM and NAND cycles.

- The key industry risk shifts toward 2028–2029, when new wafer and advanced-packaging capacity begins entering the market.

- Micron retains a distinct advantage as the only U.S.-headquartered DRAM producer building a broad domestic front-end manufacturing platform.

U.S. Investors Can Finally Buy the HBM Leader

SK Hynix’s position in the memory industry is not difficult to establish.

According to market data cited in its U.S. registration documents, the company held approximately 56.4% of the global HBM market by revenue in the first quarter of 2026. Its share of the broader DRAM market, including HBM, was approximately 29.1%, while its NAND share was about 18.5%.

That makes SK Hynix the largest HBM supplier and the second-largest producer in both DRAM and NAND.

The HBM leadership is real, but it has also encouraged investors to think about the company as though it were a pure AI memory business. Its financial structure remains more diversified—and more cyclical—than that description suggests.

In 2025, DRAM products generated approximately 77.1% of company revenue. NAND accounted for about 21.3%, with the remainder coming from other products and services. HBM sits inside the DRAM category, and SK Hynix does not separately disclose HBM revenue, operating profit or capital employed.

Outside investors therefore cannot calculate precisely how much of the company’s earnings comes from HBM, what margins the product earns or whether its returns on invested capital justify a structurally higher valuation.

The company’s record 2025 results were supported by more than HBM. SK Hynix said HBM revenue more than doubled, but it also benefited from strong conventional server DRAM demand and improved enterprise SSD sales.

This distinction matters because the company remains exposed to three overlapping cycles: AI accelerator memory, conventional DRAM and NAND.

HBM can raise the company’s average profitability, but it has not yet removed the historical volatility of commodity memory.

The scale of that volatility is visible in the recent financial record. SK Hynix reported revenue of 32.77 trillion won and an operating loss of 7.73 trillion won in 2023. Its operating margin was negative 24%.

Two years later, 2025 revenue reached 97.15 trillion won and operating profit rose to 47.21 trillion won, producing an operating margin of roughly 49%. In the first quarter of 2026, revenue reached 52.58 trillion won and operating profit climbed to 37.61 trillion won. The quarterly operating margin exceeded 71%.

That extraordinary swing reflects excellent execution in AI memory. It also demonstrates how much operating leverage remains embedded in the memory pricing cycle.

As Micron’s own AI memory test also shows, structural growth and cyclical pricing are appearing in the same income statement. Investors should not assume that every dollar of current profit represents a permanent increase in normalized earnings power.

SK Hynix Has a Real Moat, but the Moat Is Changing

SK Hynix’s HBM advantage was not created by a single successful product launch. It was built through sustained investment in through-silicon vias, die stacking, thermal management, advanced packaging, testing and customer qualification.

HBM also consumes considerably more manufacturing capacity than conventional DRAM. SK Hynix has said that producing the same memory capacity in HBM requires at least twice the production resources needed for standard DRAM. The product demands more wafer area, more complex packaging and significantly tighter yield control.

That helps explain why HBM can support higher margins. The competitive barrier includes more than the underlying DRAM die. It also includes the base die, stacking process, thermal performance, packaging throughput, testing reliability and integration with specific GPU platforms.

Once an HBM product has been qualified for a major accelerator platform, customers cannot switch suppliers as easily as they can in conventional commodity memory.

SK Hynix’s customer relationships reinforce that advantage. Its filings show that the largest customer represented 23.9% of total revenue in 2025. In the first quarter of 2026, the two largest customers represented 14.8% and 12.4% of revenue, respectively.

The company does not identify those customers, so it would be inaccurate to attribute the entire concentration to Nvidia. Jensen Huang has nevertheless described SK Hynix as Nvidia’s largest memory partner, making the commercial connection clear.

Customer concentration again cuts in both directions.

SK Hynix has earned a privileged position inside the most important AI accelerator supply chain. At the same time, a customer responsible for such a large portion of revenue has substantial influence over qualification, order allocation and pricing.

That influence becomes more important as competing suppliers improve.

Samsung has announced mass production of HBM4 for Nvidia’s Vera Rubin platform and has presented products operating at speeds of up to 11.7 gigabits per second. Micron has also entered high-volume production of a 36-gigabyte, 12-layer HBM4 product for Vera Rubin, with bandwidth above 2.8 terabytes per second and claimed power-efficiency improvements over the previous generation.

The competitive structure has therefore moved from near-exclusivity toward a three-supplier HBM4 market.

SK Hynix still holds meaningful advantages in scale, production history and customer engineering. Its future moat will depend increasingly on yield, cost, delivery reliability and the ability to maintain leadership through HBM4E and subsequent generations.

Public disclosures do not yet provide enough information to quantify that advantage precisely.

None of the three manufacturers publishes verified HBM4 production yields, unit packaging costs or Nvidia order allocations. SK Hynix also does not disclose the exact pricing, cancellation rights or minimum purchase commitments contained in its long-term customer agreements.

The industry is moving toward multi-year contracts and take-or-pay arrangements, which should reduce some of the volatility associated with conventional spot memory. Those contracts do not necessarily eliminate price risk.

Industry analysis cited by Reuters Breakingviews suggested that contractual protections may cover only a limited portion of total sales and often extend for approximately three years. That would improve visibility through the current shortage without guaranteeing protection once new capacity begins entering the market.

Statements that near-term production is sold out support the outlook for the next several quarters. They do not prove that current margins will survive the next supply cycle.

A Low Earnings Multiple Can Be a Warning

Ahead of the U.S. offering, SK Hynix traded at approximately 5.5 times forward earnings, compared with roughly 6.7 times for Micron.

On the surface, the comparison looks compelling. SK Hynix has the larger HBM share and stronger current profitability, yet it carries the lower earnings multiple.

Memory stocks, however, often appear cheapest near the top of the cycle.

SK Hynix shares rose by roughly 680% over the preceding year, but earnings estimates increased even faster. Its forward multiple fell from about 7.9 times in late October 2025 to approximately 5.5 times before the offering.

That does not necessarily mean the market failed to appreciate the company. It may mean investors are unwilling to capitalize the current level of earnings as permanent.

Cash investment also needs to be considered.

SK Hynix spent approximately 27.52 trillion won on property, plant and equipment in 2025, up from 15.95 trillion won in 2024. First-quarter 2026 spending reached roughly 7.66 trillion won, and the company has said that full-year capital expenditure will be materially higher than in 2025.

Operating profit, net income and shareholder cash flow are not interchangeable.

Operating profit measures current production economics. Net income can be affected by exchange rates, investments, financing and tax items. The cash that can ultimately be returned to shareholders must also account for the capital required to maintain process competitiveness and build the next generation of capacity.

For a memory manufacturer, much of that spending is not optional. A company that stops investing may preserve cash temporarily, but it will quickly lose ground in process technology, cost per bit and customer qualification.

From SK Hynix’s perspective, selling equity after a major increase in earnings and share price is rational. The transaction reduces dependence on debt and allows the company to finance expansion with relatively expensive equity.

For existing and new shareholders, the equation is more complicated. The offering creates dilution, while the projects it finances will eventually add depreciation and potentially increase industry supply.

A more useful valuation framework would estimate SK Hynix’s normalized free cash flow in 2028 or 2029 rather than simply applying a higher multiple to 2026 earnings.

That analysis should assume that conventional DRAM and NAND pricing returns toward mid-cycle levels, HBM competition becomes more balanced, and depreciation from new facilities begins to enter the income statement. It should also preserve some of the structural benefits created by AI demand and SK Hynix’s technical leadership.

If the company can maintain materially higher free cash flow under those conditions, then HBM has genuinely raised its long-term earnings power. Until that is demonstrated, a forward multiple of five or six times may be less reassuring than it appears.

The Most Important Consequence of the Nasdaq Listing May Arrive Years Later

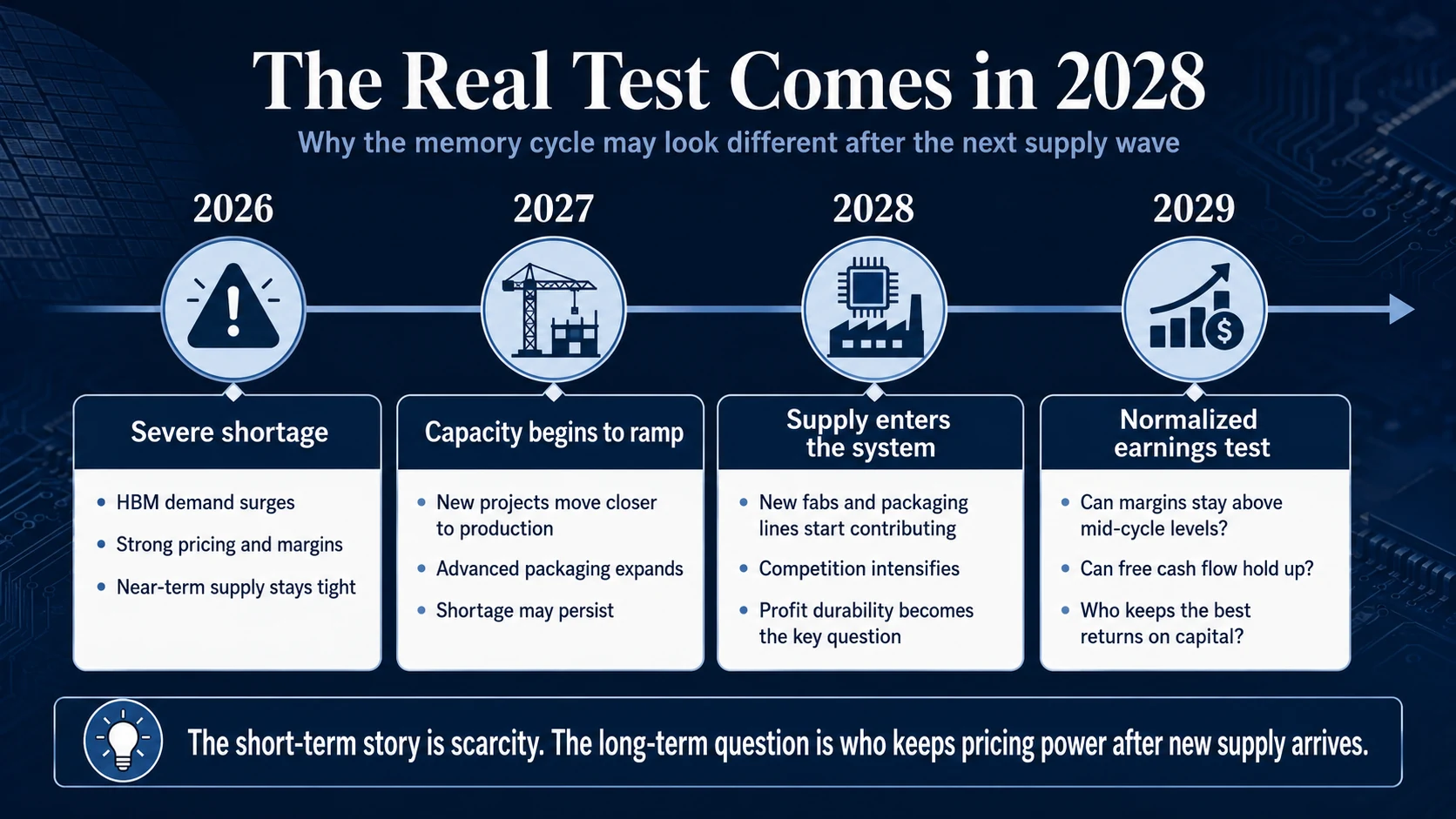

The market is currently focused on severe memory shortages in 2026 and 2027.

SK Hynix management has argued that 2027 could bring the most significant memory shortage in the industry’s history and that demand may continue to exceed the company’s own supply capacity beyond 2030.

That view has a credible foundation.

HBM is already one of the AI semiconductor system’s most visible bottlenecks, and it consumes more wafer and packaging resources than conventional DRAM. AI servers are also increasing demand for conventional server memory and enterprise SSDs. In late 2025, SK Hynix said that expected 2026 DRAM and NAND output was already covered by customer demand and that discussions over HBM supply were largely complete.

Near-term scarcity, however, does not stop the capital cycle.

SK Hynix is expanding advanced DRAM and HBM capacity at M15X in Cheongju, with long-term investment expected to exceed 20 trillion won. The first fab in the Yongin semiconductor cluster is scheduled for completion in 2027 and will produce next-generation DRAM and HBM.

The company is also building the P&T7 advanced packaging facility in Cheongju, scheduled for completion near the end of 2027. Its Indiana HBM production, packaging and research facility is expected to begin operations in the second half of 2028. SK Hynix has also announced plans to invest 80 trillion won in an M17 NAND facility targeted for operation in 2029.

Competitors are expanding as well.

Micron expects initial wafer output from its first Idaho DRAM fab around the middle of 2027, with a second facility expected to begin production near the end of 2028. It has increased its planned U.S. investment through 2035 to more than $250 billion and intends eventually to produce about 40% of its global DRAM output in the United States.

Samsung is also increasing advanced memory and packaging capacity.

The result is a timeline in which severe near-term scarcity and medium-term supply pressure can both be true, which is central to reading the broader AI cycle.

Capacity remains constrained through 2026 and much of 2027. Advanced process transitions and packaging lines require time to qualify and ramp. By 2028 and 2029, new wafer and packaging capacity from SK Hynix, Micron and Samsung should begin reaching the market in larger volumes.

At that point, industry economics will depend on whether AI inference, custom accelerators and data-center storage demand can absorb the additional bit supply.

This is the most important dividing line in the SK Hynix investment case.

Whether earnings reach another record in the next four quarters will matter to the stock. How much the company can earn after new capacity enters the market will determine whether the current multiple represents value or a familiar cycle-top illusion.

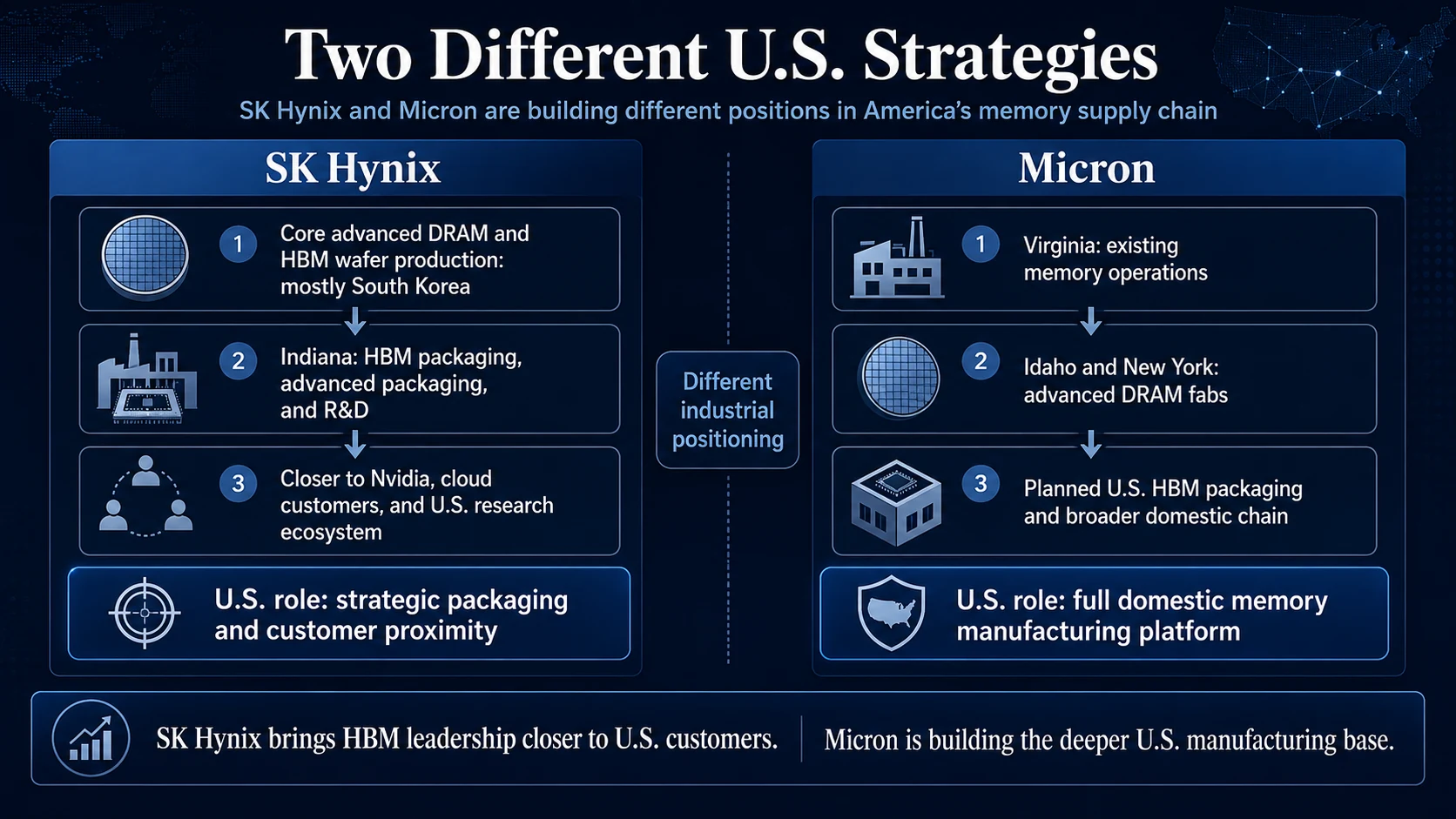

The U.S. Supply Chain Reveals the Difference Between SK Hynix and Micron

SK Hynix’s primary U.S. manufacturing project is located in West Lafayette, Indiana. The facility represents an investment of approximately $3.87 billion and is supported by up to $458 million in direct U.S. government grants and as much as $500 million in loans.

The funding will be distributed according to construction, technology, production and commercialization milestones.

The project will include next-generation HBM production, advanced packaging and research facilities. It is expected to begin operating in the second half of 2028.

The Indiana plant is strategically significant, but it is not currently planned as a complete front-end DRAM wafer fab. SK Hynix will continue producing most advanced DRAM wafers in South Korea, while the Indiana operation focuses on stacking, packaging, testing and research closer to Nvidia, U.S. cloud providers and American research institutions.

Micron’s U.S. strategy reaches further into front-end production.

In addition to its existing Virginia operations, Micron is building two advanced DRAM fabs in Idaho and planning as many as four fabs in New York. It is also developing domestic HBM packaging capabilities.

Micron has signed a ten-year silicon wafer supply agreement with GlobalWafers and committed $500 million to support its 300-millimeter wafer project in Texas. The company is attempting to build a more complete U.S. memory chain extending from silicon wafers and front-end DRAM manufacturing to advanced HBM packaging.

The two companies therefore occupy different positions in the American supply chain.

SK Hynix is bringing the industry’s most mature HBM manufacturing and packaging expertise closer to U.S. customers. Micron is building a broader domestic manufacturing platform that includes the front-end production of advanced DRAM.

This is the industrial scarcity Micron retains.

SK Hynix’s Nasdaq listing removes the obstacle preventing U.S. investors from owning the HBM leader. It does not change Micron’s position as the only U.S.-headquartered member of the global DRAM oligopoly or its importance to Washington’s effort to establish domestic advanced memory production.

That strategic value carries costs.

Construction, labor and operating expenses are generally higher in the United States than in major Asian manufacturing centers. U.S. fabrication projects take longer to build, and government support does not automatically guarantee attractive returns on capital.

Micron deserves a policy premium only if subsidies, customer demand and supply-security value are sufficient to offset those higher costs.

China Remains an Underappreciated Source of Risk for SK Hynix

SK Hynix operates major DRAM facilities in Wuxi, NAND manufacturing assets in Dalian and back-end production in Chongqing.

Reuters reported in 2023 that Wuxi accounted for roughly 40% of SK Hynix’s DRAM production at the time, while Dalian represented approximately 20% of NAND output. The company’s current registration documents still identify the Chinese operations as major manufacturing assets, although they do not provide updated production percentages.

The policy environment has become less predictable.

In 2025, the United States ended the broad Validated End User treatment previously available to Samsung, SK Hynix and TSMC for their Chinese operations. SK Hynix subsequently obtained annual approval to ship certain U.S. manufacturing equipment to its Chinese plants during 2026, but future access will require recurring regulatory review.

The more likely risk is gradual technological aging rather than an abrupt shutdown.

Restrictions on equipment, replacement parts and software upgrades could prevent the Chinese fabs from moving to the most advanced process nodes at the same pace as new Korean facilities. Over time, those plants could be pushed toward older, lower-priced products.

Their cost position and asset returns would then deteriorate even while depreciation continued.

SK Hynix’s acceptance of U.S. CHIPS funding creates additional constraints. Companies receiving awards and their broader corporate groups face restrictions on significant advanced semiconductor expansion in China and other countries of concern for ten years.

Existing facilities can perform ordinary upgrades, but capacity additions involving new clean-room space or production expansion above specified thresholds are restricted. Certain joint research and technology-licensing arrangements are also limited. Serious violations can lead to the recovery of federal funding.

These rules do not force SK Hynix to leave China. They reduce the long-term strategic flexibility of its Chinese asset base.

Micron faces its own global manufacturing risks, but its future DRAM expansion is more clearly centered on the United States, Taiwan and Japan. The two companies therefore carry different geopolitical exposures, and that difference should be reflected in valuation.

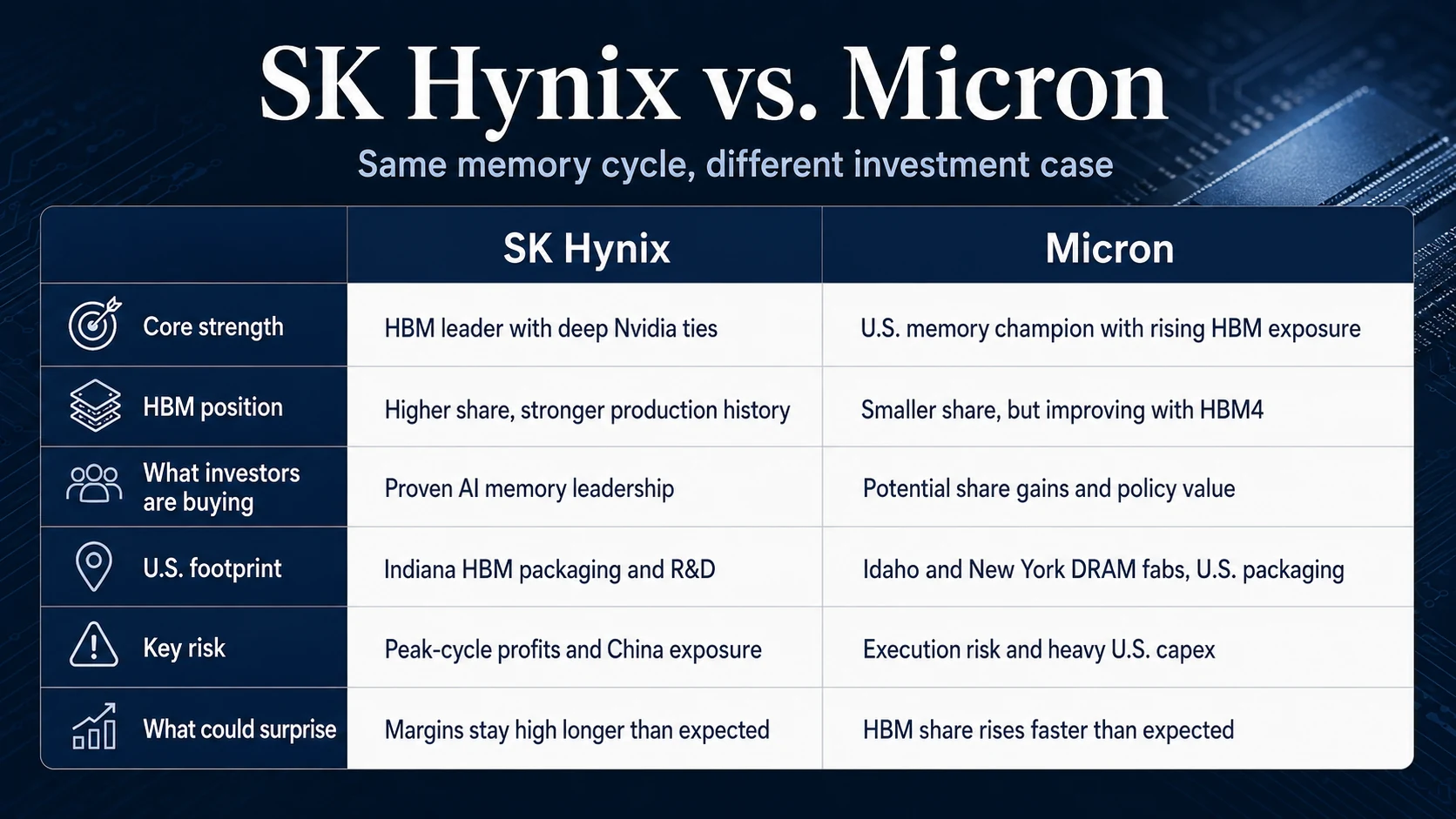

What Micron Loses—and What It Still Keeps

SK Hynix’s Nasdaq listing removes Micron’s scarcity as the default U.S. trading vehicle for memory exposure.

U.S. funds can now buy the company with the largest HBM share, the deepest production relationship with Nvidia and the strongest current profitability. Some capital that previously flowed into Micron because there was no convenient alternative may migrate toward $SKHY.

Micron retains several important sources of potential value.

Its lower HBM market share is a competitive weakness, but it also creates room for positive earnings revisions if the company gains allocation. Micron has entered HBM4 volume production and secured participation in the Vera Rubin platform.

The company does not need the current supplier structure to remain unchanged. It can create upside simply by narrowing the gap.

Micron also retains a more direct role in U.S. industrial policy. Its front-end DRAM fabs, long-lifecycle memory products and planned domestic HBM packaging operations give it a strategic position in defense, automotive, industrial and critical-infrastructure supply chains.

The market is also asking the two companies to prove different things.

SK Hynix is already the HBM leader. Investors will expect it to defend that position. Micron begins from a lower share base, so continued qualification and production improvements can create upside through expectation changes.

SK Hynix is exposed to the risk that its lead narrows. Micron has an opportunity if the lead narrows.

That does not automatically make Micron the better stock. It is also operating with unusually high margins and entering a large capital-spending cycle. Its U.S. projects will create depreciation and execution risk, just as SK Hynix’s expansion will.

Both companies will eventually face the same test: whether returns on invested capital remain attractive after the next wave of capacity is built.

SK Hynix Is a High-Quality Cyclical Manufacturer With a Structural AI Advantage

The most accurate description of SK Hynix is neither a conventional commodity memory producer nor a fully transformed AI platform company.

It is a high-quality cyclical manufacturer that has used HBM to improve its competitive position, product mix and earnings power.

The company has already demonstrated strong technology selection, manufacturing execution and customer coordination. It has not yet demonstrated that those strengths can continue producing exceptional free cash flow after Samsung and Micron fully ramp HBM4 and after the industry’s new fabrication and packaging capacity enters production.

For SK Hynix to deserve a durable valuation premium over traditional memory companies, several conditions must become visible.

The company needs to maintain a leading share through HBM4E and subsequent generations while preserving yield and unit-cost advantages. Customer concentration needs to fall as custom accelerators and additional AI platforms become meaningful sources of demand. HBM profitability must remain large enough to absorb future declines in conventional DRAM and NAND. New factories must generate attractive returns after accounting for depreciation, working capital and the full capital required to remain technologically competitive.

The Nasdaq listing cannot answer those questions.

It makes SK Hynix easier to own and gives the company more capital to prove its strategy. It also makes the memory sector easier to compare.

Micron may lose investor flows that once depended on its trading scarcity. It may also benefit from SK Hynix becoming a higher valuation reference point for the industry.

The decisive comparison will involve technology share, customer concentration, capital intensity, geopolitical exposure and normalized free cash flow.

The most important question is not which company earns more in 2026 or which stock performs better immediately after SK Hynix’s debut.

The real test will come when SK Hynix’s Yongin and P&T7 facilities, Micron’s Idaho fabs and Samsung’s new capacity begin entering the market between 2027 and 2029.

Whichever company can preserve pricing power, free cash flow and returns on invested capital through that supply expansion will deserve the superior valuation.

That outcome will determine whether SK Hynix’s current forward earnings multiple of roughly five to six times represents a genuine opportunity—or another optical illusion created by peak memory profits.

Frequently Asked Questions

Is SK Hynix now a U.S. company?

No. Its ADSs trade on Nasdaq, but the underlying company, cash flows, governance structure, manufacturing base and primary listing remain Korean.

Does SK Hynix’s Nasdaq listing make Micron less attractive?

It removes Micron’s trading-entry scarcity, but Micron retains a distinct position as the only U.S.-headquartered advanced DRAM manufacturer building a broad domestic production base.

Why is 2028 important for the memory cycle?

Several new wafer fabs and advanced-packaging projects are expected to begin contributing between 2027 and 2029. The key question is whether AI demand can absorb that supply without materially reducing pricing and margins.

Is SK Hynix a pure HBM investment?

No. HBM is part of its DRAM business, while conventional DRAM, NAND and enterprise SSDs continue to represent meaningful portions of revenue and earnings.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | SK Hynix U.S. registration statement | SEC EDGAR | 2026 | SEC | Market share, customer concentration, business mix, manufacturing footprint, capital expenditure and risk disclosures. |

| 2 | SK Hynix final U.S. offering document | SEC EDGAR | 2026 | SEC | ADS ratio, offering size, new-share issuance, use of proceeds and ownership structure. |

| 3 | SK Hynix FY2025 financial results | SK Hynix | 2026 | Company IR | Revenue, operating profit, product growth, HBM growth and shareholder returns. |

| 4 | SK Hynix 2023 financial results | SK Hynix | 2024 | Company IR | Historical cycle comparison and 2023 operating loss. |

| 5 | SK Hynix M15X expansion announcement | SK Hynix | 2024 | Company IR | HBM production intensity, M15X expansion and HBM capacity requirements. |

| 6 | SK Hynix Indiana CHIPS award | U.S. Department of Commerce / NIST | 2024-12 | Government | Indiana investment, grants, loans, milestones and project scope. |

| 7 | CHIPS national-security guardrails | NIST | 2023 | Government | Restrictions on expansion in countries of concern and funding clawback conditions. |

| 8 | Micron begins HBM4 high-volume production for Nvidia Vera Rubin | Micron Technology | 2026 | Company IR | Micron HBM4 specifications, Vera Rubin participation and production status. |

| 9 | Samsung unveils HBM4E and Nvidia partnership at GTC 2026 | Samsung | 2026 | Company IR | Samsung HBM4 and HBM4E competition. |

| 10 | Micron accelerates U.S. investments | Micron Technology | 2026 | Company IR | U.S. DRAM investment, Idaho and New York projects and domestic production strategy. |

| 11 | SK Hynix U.S. offering | Reuters | 2026-07-09 | Market reporting | Offering price, investor demand, proceeds and valuation comparison. |

| 12 | Memory giants install limited buffer against slump | Reuters Breakingviews | 2026-07-07 | Market commentary | Long-term contract limitations and post-2028 pricing risk. |

| 13 | Annual U.S. equipment approvals for Chinese fabs | Reuters | 2025-12-30 | Market reporting | Annual U.S. equipment approvals for Chinese fabs. |

Primary filings and company materials support company-specific disclosures; Reuters sources support market reporting, valuation context and regulatory developments.

Related Reading

Micron Is Trying to Escape the Memory Cycle. The Real Test Begins After 2027.

Micron’s AI memory boom is no longer just about one strong quarter. The real question is whether Strategic Customer Agreements, HBM demand, and record capex can turn a memory cycle into a more predictable AI infrastructure business.

How to Read the AI Cycle: CapEx, Supply Bottlenecks, and the Semiconductor Trade

AI infrastructure spending is still expanding, but the semiconductor equity trade is becoming more fragile. The next phase depends on CapEx, supply bottlenecks, usage, pricing, and earnings revisions.

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

AI Semiconductors Are No Longer Just About Compute. They Are About System Bottlenecks.

AI semiconductors are no longer just about raw compute. The real question is which system bottlenecks customers must solve next.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments