Every major AI investment cycle eventually moves beyond the most obvious winner.

The first wave focused on compute. The next moved into high-bandwidth memory, networking, power and cooling. Now investors are searching farther down the infrastructure stack, where the physical movement of data is becoming almost as important as the processing of data itself.

That search has brought optical connectivity into the investment mainstream.

GlobalFoundries describes its silicon photonics platform as supporting current pluggable transceivers and the transition toward near-packaged and co-packaged optics. Its recently introduced SCALE platform is designed to integrate optical connectivity more closely with advanced AI compute systems. (GlobalFoundries)

Sivers Semiconductors occupies a small but potentially important position in that transition. Its Photonics business develops high-power indium phosphide, or InP, distributed-feedback lasers and laser arrays that can provide the light source for optical interconnects. Its Wireless business develops millimeter-wave beamforming chips and modules for satellite communications, defense and fixed wireless systems. (Sivers Semiconductors)

The company has attracted attention because it offers exposure to several themes that investors currently value highly:

- AI data-center optics

- co-packaged optics, or CPO

- external laser sources

- satellite communications

- defense electronics

- a possible future U.S. listing

But the most useful way to describe Sivers today is not “undiscovered.”

It is discovered, but not yet commercially proven.

At the end of 2025, the company had a market capitalization of approximately SEK 1.29 billion. By June 2026, Sivers was able to raise SEK 700 million at SEK 57 per share in a placement that was multiple times oversubscribed by Swedish and international institutional investors. That contrast does not establish fair value, but it shows that Sivers has already moved from obscurity into active institutional price discovery. (Sivers 2025 Annual Report)

The investment question has therefore changed.

It is no longer:

When will the market discover Sivers?

It is now:

How much future business is the market pricing before the operating evidence has appeared?

The investment conclusion

Sivers has real technology, real customers, an internal photonics manufacturing facility and credible industry partners. It is not merely a social-media narrative.

However, the largest revenue scenarios circulating around the company begin with theoretical manufacturing capacity and end with hundreds of millions of dollars in sales. They usually spend far less time on the steps between those two figures.

Those steps determine whether the revenue ever appears:

Technology

→ process transfer

→ reliability qualification

→ customer qualification

→ qualified capacity allocation

→ commercial yield

→ production orders

→ revenue

→ operating cash flow

→ diluted per-share value

The bullish case is credible because Sivers is positioned in markets with substantial potential demand and currently has a small revenue base. A successful transition to repeatable product shipments could change its financial profile quickly.

The risk is that investors are treating ecosystem participation as customer adoption, foundry capacity as Sivers capacity, pipeline as backlog and theoretical output as saleable production.

Those concepts are related. They are not interchangeable.

What does Sivers actually sell?

Sivers operates through two reportable businesses.

Its Wireless division develops millimeter-wave beamforming integrated circuits, transceivers, antenna modules and related systems. These products are primarily aimed at satellite communications, defense, fixed wireless access and future wireless networks.

Its Photonics division develops and manufactures laser components based on III-V compound semiconductors. The portfolio includes DFB lasers, laser arrays, gain chips and semiconductor optical amplifiers for data communications, sensing and LiDAR. (Sivers 2025 Annual Report)

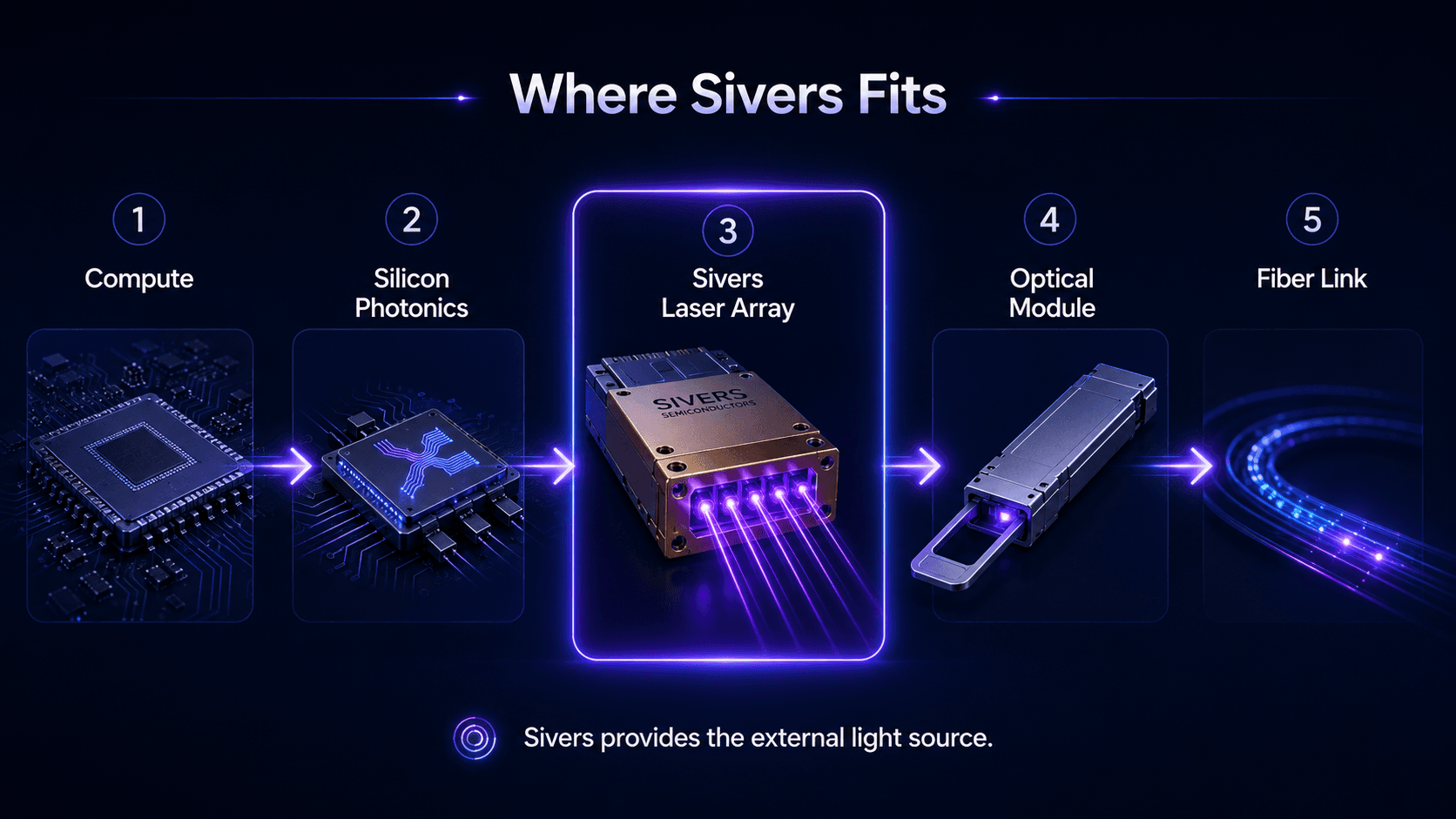

For investors focused on AI, the relevant product is principally the laser or laser array.

A simplified optical data path looks like this:

GPU, ASIC or network switch

↓

silicon photonics or optical engine

↓

external laser source

↓

optical module and packaging

↓

fiber connection

Sivers does not sell the entire switch, optical engine or transceiver system. It supplies one of the critical active components within that system: the light source.

That position can be valuable, but it also limits the portion of the total system economics that Sivers can capture. Its revenue will depend on:

- the number of lasers or arrays required per system

- the number of channels in each array

- Sivers’ share of the final design

- whether the product is sold as a bare die, packaged device or integrated source

- production yield

- volume pricing

- the customer’s own deployment schedule

A large CPO market does not automatically create a large Sivers business. Sivers must first win a meaningful portion of that market and manufacture the product economically.

Today’s financial statements are not yet an AI-photonics earnings story

The present financial baseline matters because it shows how much of the investment case depends on future execution.

Sivers generated SEK 306.6 million of revenue in 2025. Wireless contributed SEK 213.1 million, or roughly 70% of the total, while Photonics contributed SEK 93.4 million, or roughly 30%. The company reported an operating loss of SEK 177.8 million and a net loss of SEK 222.6 million. (Sivers 2025 Annual Report)

Customer concentration was also substantial. Three customers each accounted for more than 10% of group revenue in 2025. Together they generated SEK 183.4 million, and all three belonged to the Wireless segment. (Sivers 2025 Annual Report)

The first quarter of 2026 did not yet show an AI-photonics inflection. Group revenue declined 22% year over year to SEK 61.9 million, Photonics revenue declined 32%, adjusted EBITDA was negative SEK 13.8 million and operating cash flow was negative SEK 49.2 million. (Sivers Q1 2026)

Management attributed some of the weakness to delayed U.S. defense spending and exchange-rate effects. Those factors may explain quarterly timing, but they do not change the central observation: the current income statement remains heavily influenced by Wireless projects, while the large AI-photonics thesis is still primarily forward-looking. (Sivers Q1 2026)

Sivers also reported that its opportunity pipeline had increased 77% from the end of 2025 to $799 million. Management said the growth was driven by both wireless beamformer opportunities and interest in InP lasers. (Sivers Q1 2026)

That is a positive commercial indicator. It is not an order book.

An opportunity pipeline can contain projects at widely different stages:

initial customer discussion

→ technical evaluation

→ sample order

→ design-in

→ qualification

→ production decision

→ purchase order

Until the company discloses the probability, timing and stage of each opportunity, the $799 million figure should be treated as evidence of customer engagement—not as contracted future revenue.

Is Sivers a fabless company?

The common description of Sivers as purely fabless is too simplistic.

The company’s annual report states that it operates a production facility in Glasgow, Scotland, which manufactures customized lasers and semiconductor optical amplifiers. Its first-quarter report also identifies the Scottish operation as a Photonics research, development and fabrication site. (Sivers 2025 Annual Report)

At the same time, Sivers is pursuing a fab-light or hybrid model for larger-volume production. In March 2025, it announced that WIN Semiconductors would become an outsourced manufacturing partner for its high-power DFB lasers and arrays. The official release described the partnership as paving the way for high-volume manufacturing and bringing the products toward high-volume production. (Sivers-WIN partnership)

Both sides of the debate therefore need refinement.

Sivers does not have no manufacturing capacity. It possesses an internal photonics facility and an external manufacturing route.

But the existence of those routes does not prove that Sivers already has enough qualified, allocated and customer-approved capacity to support the largest revenue forecasts.

The correct question is not:

Does Sivers have a fab?

It is:

How much capacity can produce Sivers’ products at commercial yield, within customer specifications and on a repeatable schedule?

That number has not yet been publicly quantified.

What the latest Sivers announcements actually change

Not all corporate announcements move a company equally far toward revenue.

An effective way to evaluate each Sivers announcement is to ask which operating variable it changes—and which variables remain unresolved.

| Development | What it supports | What it does not yet prove |

|---|---|---|

| WIN Semiconductors manufacturing partnership | Establishes an external route toward higher-volume laser production. | Sivers-specific wafer allocation, current production yield, commercial output or customer-approved volume. |

| GlobalFoundries collaboration | Places Sivers laser arrays in reference designs for GF’s silicon-photonics platform and makes them available within the SCALE optical-engine ecosystem. | A production purchase order, hyperscaler deployment or committed annual volume. |

| Jabil 1.6T transceiver collaboration | Validates Sivers lasers as an input to a planned 1.6T linear-receive optical module. | Completed module qualification, volume production or contracted laser sales. |

| O-Net and Enablence external-light-source project | Moves Sivers from a stand-alone laser array toward a more complete external light-source module with an ODM and optical-coupling partner. | End-customer adoption, deployment timing or revenue scale. |

| Automotive LiDAR ramp | Provides a relatively specific Photonics production milestone, with qualification builds and readiness work targeting a fourth-quarter 2026 ramp. | Whether the ramp will occur on time, at what volume, margin and cash-conversion profile. |

| ALL.SPACE production order | Demonstrates that Sivers can move a customer from development into scaled production; the 2027 order is worth $8.2 million. | AI-photonics demand or laser-array manufacturing economics—the order belongs to Wireless. |

| 2026 capital raises | Improves the balance sheet and funds InP capacity, customer support and R&D. | Customer demand, manufacturing yield or per-share value creation. |

| Potential U.S. dual listing | Could widen the investor base and improve access to U.S. technology capital markets. | Any direct improvement in products, orders, revenue or margins. |

This distinction is central to the investment case.

GlobalFoundries, Jabil, WIN, O-Net and Enablence are meaningful relationships. They reduce the probability that Sivers’ technology is irrelevant.

They do not eliminate the possibility that commercialization is slower, smaller or less profitable than investors currently expect.

The market is building revenue models from the wrong end

One widely discussed Sivers capacity scenario uses assumptions similar to the following:

The result is approximately:

The arithmetic is internally consistent.

The evidence chain is not yet complete.

Even assuming the 35,000-wafer figure accurately describes WIN’s total InP nameplate capacity, the official Sivers–WIN announcement does not disclose how much of that capacity is reserved for Sivers, how many production wafers have been started, what yield has been achieved or how much output has passed customer qualification. (Sivers-WIN partnership)

The calculation is therefore best understood as a capacity sensitivity case, not a base-case forecast.

Total foundry capacity is not Sivers capacity

A foundry’s company-wide InP capacity can serve multiple customers, products and process flows.

The relevant capacity for Sivers is the subset that is:

- compatible with Sivers’ specific manufacturing process

- qualified for the required product specifications

- allocated to Sivers

- scheduled when Sivers needs it

- supported by customer demand

Calling a 10% allocation “conservative” merely because 10% appears small is a mistake.

A percentage is conservative only relative to supporting evidence. For an emerging product without a publicly disclosed long-term wafer-allocation agreement, 10% of a large foundry’s total capacity could be an aggressive assumption.

Evidence that would support the 10% input could include:

- an explicit capacity-reservation agreement

- annual wafer-start guidance

- a take-or-pay arrangement

- a long-term customer-backed supply contract

- disclosed production batches at relevant volume

None of those has yet been publicly disclosed in connection with the WIN arrangement.

Gross arrays per wafer are not saleable arrays

The assumption of 3,000 arrays per wafer may or may not be physically reasonable. That depends on wafer diameter, array dimensions, scribe lanes, edge losses, test structures and the number of channels per array.

But even a reasonable gross die count does not equal saleable output.

Saleable production must account for:

- wafer-process yield

- individual laser performance

- wavelength consistency

- output-power specifications

- array-level channel matching

- reliability screening

- dicing and packaging losses

- final optical and electrical testing

This distinction may be particularly important for multi-channel arrays. A product containing several lasers can have different final-yield economics from a single laser die because failure or underperformance in one channel can reduce the value of the complete array.

The 65% yield assumption therefore needs a definition.

Is it wafer yield? Die yield? Optical-test yield? Or final saleable-array yield after every required test?

Without that definition and actual production data, it remains a scenario input.

ASP cannot be separated from volume

The $50–$75 average selling-price assumption may be a reasonable range for a scenario model, but price is not independent of scale.

A customer buying prototypes, qualification units or small batches may pay a materially different price from a customer ordering millions of units.

Realized ASP will depend on:

- the number of channels

- optical power

- wavelength requirements

- bare-die versus packaged delivery

- who pays for testing and packaging

- customer concentration

- annual volume

- negotiated price reductions over the product life cycle

A model that increases volume dramatically while keeping ASP fixed may overstate revenue unless the product retains strong differentiation and negotiating power.

Production capacity does not create customer orders

Even if Sivers could produce 6.8 million saleable arrays annually, revenue would still require customers to purchase them.

The more accurate formula is:

Where:

This formulation forces an investor to model both supply and demand.

It also prevents four distinct concepts from being merged into one:

foundry nameplate capacity

≠ qualified process capacity

≠ capacity allocated to Sivers

≠ customer-ordered output

Why the gross-profit shortcut is also dangerous

Some capacity models take the resulting $341–$512 million revenue estimate and apply a 50%–60% gross margin.

That can produce more than $200 million of hypothetical annual gross profit.

It is a useful terminal-state sensitivity. It is not a complete equity valuation.

New semiconductor products frequently experience less favorable economics during initial production than after a mature ramp. Potential costs include engineering wafers, repeated process runs, low initial yield, additional reliability testing, smaller packaging volumes, customer-support expenses and inventory risk.

A fab-light model can reduce the capital burden of building a large internal foundry. It does not remove manufacturing risk. It transfers part of that risk into process qualification, supplier economics, capacity access and production scheduling.

Gross profit also sits far above the metric that ultimately belongs to shareholders.

The full chain is:

Revenue

→ gross profit

→ operating profit

→ free cash flow

→ diluted free cash flow per share

→ equity value

Sivers must continue funding research and development, sales, engineering support, administration, public-company costs and potential U.S.-listing expenses.

A market-cap-to-gross-profit comparison can therefore make the shares appear much cheaper than a valuation based on operating income or free cash flow.

Financing has reduced one risk while increasing another

Sivers entered 2026 with a genuine financing constraint.

At March 31, the company reported SEK 26.6 million in cash after using SEK 49.2 million in operating cash flow during the first quarter. (Sivers Q1 2026)

It subsequently completed several significant capital transactions.

In April, Sivers issued 8.62 million shares at SEK 14.50, raising approximately SEK 125 million. In June, it issued another 12.28 million shares at SEK 57, raising SEK 700 million before transaction costs. The June placement was multiple times oversubscribed, and management said the proceeds would support InP manufacturing capacity, customer resources and research and development. (April placement)

In July, Bootstrap Europe converted its entire $12 million convertible loan into 22.85 million new ordinary shares. The conversion reduced outstanding debt but diluted existing holders by approximately 6.4%. (Convertible conversion)

These transactions materially strengthen the company’s ability to execute.

They also reinforce a second analytical principle:

Enterprise growth and per-share growth are not the same thing.

The registered share count increased from approximately 311.3 million at March 31 to 355.1 million following the July conversion—an increase of roughly 14%. (Sivers Q1 2026)

The financing should not be viewed only as negative dilution. Raising capital at favorable prices can create value when the funds finance high-return manufacturing capacity, customer wins or profitable growth.

But investors must model the number of shares required to reach scale.

A company can become substantially larger while generating less value per original share than a headline revenue forecast implies.

Financial reporting quality is part of the investment case

Sivers is evaluating a dual listing on Nasdaq New York while retaining its Swedish domicile and Stockholm listing. As part of that process, it upgraded the audit work on its 2024 and 2025 financial statements toward U.S. PCAOB standards. (Potential dual listing)

That process resulted in several adjustments.

The company reallocated revenue between reporting periods, revised inventory values, changed assumptions for share-based compensation and impaired previously capitalized development expenses. Its reported 2025 operating loss was revised from SEK 141.3 million to SEK 177.8 million, while the net loss was revised from SEK 186.5 million to SEK 222.6 million. The 2024 financial statements were also restated. (Restated 2025 Annual Report)

The annual report identified material weaknesses in internal control over financial reporting, and management said it was implementing remediation measures. The auditor also described significant deficiencies and errors affecting financial reporting. (Sivers 2025 Annual Report)

At the 2025 reporting date, the auditor highlighted a material uncertainty related to financing and the company’s ability to continue operations to the planned extent. The subsequent equity raises and debt conversion have materially changed that liquidity picture, so the year-end warning should not be treated as an unchanged assessment of the company today.

Still, the reporting history deserves a valuation discount until controls are demonstrably improved.

For an early-stage public company, financial controls are not an administrative detail. They affect:

- investor confidence

- revenue-recognition reliability

- forecasting quality

- access to capital

- readiness for a U.S. listing

- management’s ability to scale operations

Sivers has moved its second-quarter report to August 27, 2026, as part of its work to strengthen reporting processes and prepare for possible U.S. regulatory requirements. (Updated reporting calendar)

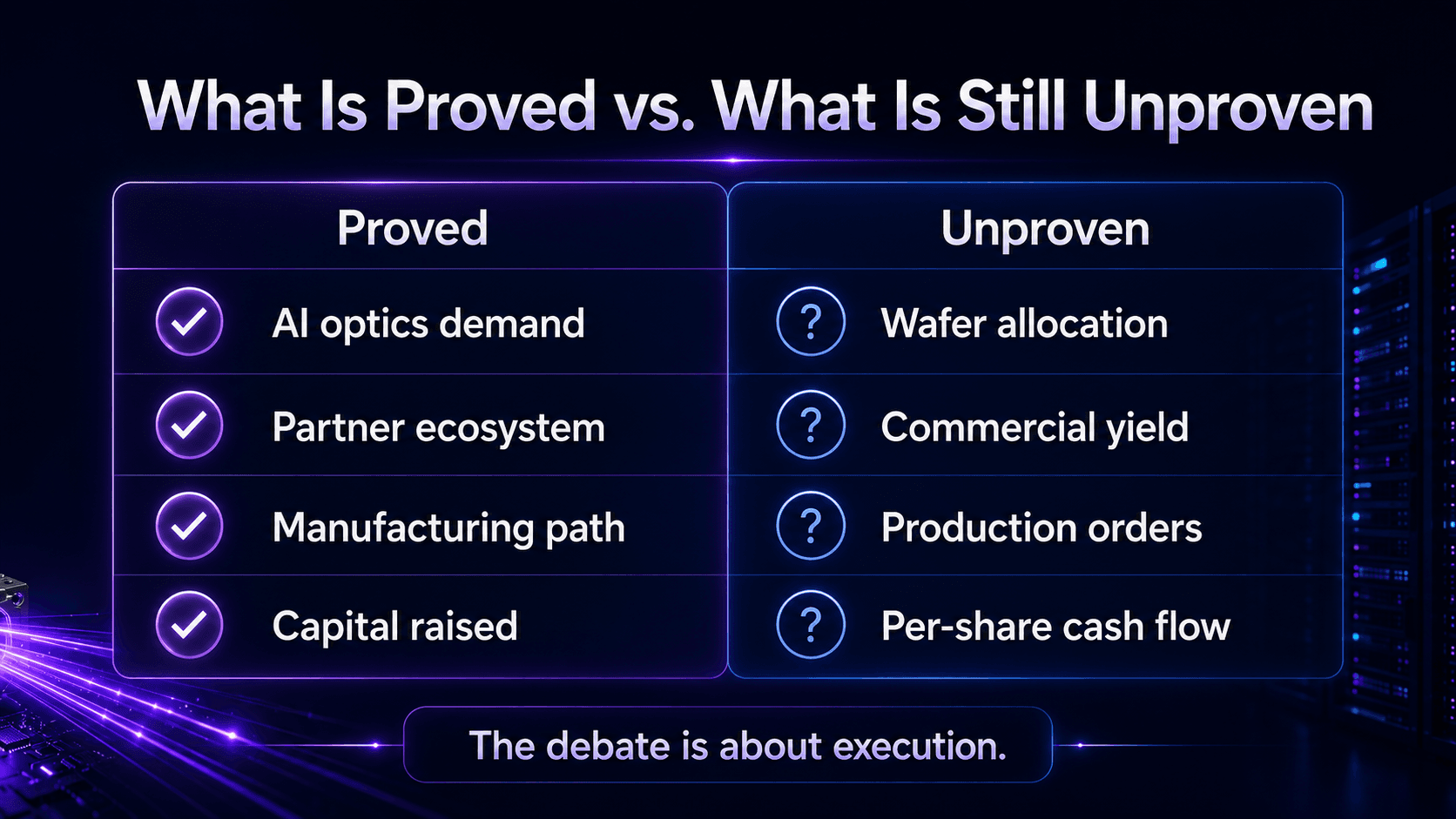

What has been proved—and what has not?

| Operating variable | Evidence today | Assessment |

|---|---|---|

| Demand for more efficient AI optical connectivity | GF is investing in silicon-photonics and CPO platforms; several Sivers partners are developing next-generation optical products. | Supported at the industry level. |

| Technical relevance of Sivers lasers | Sivers has been selected for GF reference designs, a planned Jabil transceiver and an O-Net/Enablence external-light-source project. | Strong ecosystem validation. |

| Manufacturing route | Internal Glasgow facility plus WIN outsourced manufacturing partnership. | Established. |

| Sivers-specific high-volume wafer allocation | No annual allocation or wafer-start figure has been disclosed. | Unproven. |

| Commercial final yield | No saleable-array yield has been publicly disclosed. | Unproven. |

| AI data-center production orders | Current announcements principally concern partnerships, designs and development. | Not yet sufficiently demonstrated. |

| Near-term Photonics production ramp | Automotive LiDAR qualification and readiness work target a Q4 2026 ramp. | Specific and testable. |

| Ability to convert development into production | ALL.SPACE has placed an $8.2 million Wireless production order for 2027. | Demonstrated in Wireless, not yet in AI Photonics. |

| Capital availability | Approximately SEK 825 million raised across the April and June placements, followed by debt conversion. | Substantially improved. |

| Protection of per-share value | Repeated equity issuance and debt conversion have increased the share count. | Mixed. |

| Financial reporting controls | Restatements and identified material weaknesses are being remediated. | Requires continued evidence. |

The table leads to a balanced conclusion.

The Sivers thesis is not unsupported. The company has credible products, industrial partners, a manufacturing strategy and growing customer engagement.

But the assumptions most responsible for the largest revenue estimates—allocation, yield, production orders, realized ASP and cash conversion—remain the least visible.

The strongest bull case

The strongest bullish argument is not that WIN owns a certain number of wafers.

It is that Sivers could become a broadly used independent light-source supplier across multiple silicon-photonics, pluggable-optics and CPO platforms.

That outcome becomes plausible if several conditions converge:

- Sivers’ products continue to receive technical validation

- its partners convert reference designs into customer products

- WIN and the Glasgow operation supply reliable qualified output

- large customers place repeat production orders

- product economics remain attractive after volume pricing

The company’s small Photonics revenue base creates substantial operating convexity. A single meaningful volume program could materially alter its revenue mix. Several successful platforms could transform the company.

The recent capital raise also gives Sivers more resources to invest before customer ramps begin. That matters in a market where equipment lead times, customer support and qualification work may require spending ahead of revenue.

Under that scenario, today’s business would not simply grow. Its composition would change from Wireless-led project revenue toward a larger base of repeatable Photonics hardware shipments.

That is the pathway to a genuinely high-multiple outcome.

The strongest bear case

The strongest bearish argument is not that AI will stop needing optical connectivity.

It is that industry demand may be real while Sivers captures less of it than investors expect.

The company could remain technically relevant but commercially subscale. Partnerships may generate samples and design activity without becoming large production programs. Customer qualification could take longer than expected. A larger supplier could win the final production award. Yield could be lower, ASP could fall at volume, or capacity could arrive before customer demand.

Sivers also has to fund the period between product development and cash generation.

If commercial ramps are delayed while operating expenses, capital expenditure and U.S.-listing costs continue, future financing could again become necessary. In that case, the enterprise might continue progressing while original shareholders absorb further dilution.

The bear case therefore does not require technological failure.

It only requires the path from technology to cash flow to be slower, smaller or more capital-intensive than the market has priced.

The operating evidence that matters next

Photonics revenue growth. The most useful signal will be several consecutive quarters of higher hardware revenue, rather than another increase in the opportunity pipeline.

The automotive LiDAR ramp. The planned fourth-quarter 2026 ramp is the clearest near-term test of whether Sivers can turn Photonics qualification into repeatable production. (Sivers Q1 2026)

AI data-center production orders. The critical transition is from collaboration language to production purchase orders with disclosed timing or commercial scale.

Manufacturing disclosure. Actual wafer starts, allocated capacity, production batches or yield trends would make the large revenue models substantially more credible.

Gross margin and cash conversion. Revenue growth will matter less if it arrives with poor yields, high incremental costs or continued operating cash burn.

Diluted share count. Investors should track value per share, not only total company revenue or enterprise value.

Internal-control remediation. Stable reporting, fewer revisions and progress toward PCAOB-ready processes would reduce the governance discount.

Is Sivers a U.S. stock?

Sivers’ primary listing is on Nasdaq Stockholm under the ticker SIVE. (Sivers Investors)

The company also has U.S. over-the-counter trading under SIVEF. OTC Markets classifies SIVEF as ordinary shares; it is not currently a Nasdaq-listed U.S. stock or a conventional sponsored ADR. (OTC Markets)

Sivers is evaluating a dual listing on Nasdaq New York while retaining its Swedish domicile and Stockholm listing. The company says the objective is to gain access to U.S. technology-focused capital markets and broaden its international investor base, but the process had not been completed as of this article’s publication date. (Potential dual listing)

Global institutional investors can already buy the Stockholm-listed shares when their mandates and trading infrastructure permit it. The participation of Swedish and international institutions in the June financing demonstrates that professional capital is not structurally excluded.

For many individual investors, however, access remains less convenient than buying a standard U.S.-listed stock. Broker support, foreign-exchange costs, market hours, custody and OTC liquidity can create friction.

A Nasdaq New York listing could improve accessibility and liquidity.

It would not solve customer qualification, manufacturing yield or order conversion.

Final assessment: discovered, but not proved

Sivers Semiconductors is neither an empty AI promotion nor a finished AI-photonics business.

It has real laser products, a photonics manufacturing facility, an outsourced foundry relationship and partnerships with important companies across the optical ecosystem. It has also secured capital to support capacity expansion and commercial execution.

But the current financial statements remain Wireless-heavy, loss-making and cash-consuming. The largest AI-photonics revenue estimates depend on operational parameters that have not yet been publicly demonstrated.

The most important misunderstanding surrounding Sivers is the idea that AI demand and foundry capacity naturally become company revenue.

They do not.

AI demand creates an opportunity.

Technology creates eligibility.

Qualification creates access.

Allocated capacity and yield create saleable supply.

Production orders create revenue.

Cash conversion and dilution determine shareholder returns.

Sivers may eventually become an important independent supplier of light sources for AI optical systems.

It may also remain a technically impressive company whose commercial scale arrives later and at lower margins than investors expect.

The next chapter will not be decided by another partnership announcement or another spreadsheet multiplying wafers by ASP.

It will be decided by whether qualification, manufacturing and customer adoption begin appearing—consistently—in the financial statements.

Frequently Asked Questions

What does Sivers Semiconductors do?

Sivers develops high-power DFB lasers and laser arrays for optical communications, AI data centers and sensing, as well as millimeter-wave beamforming chips and modules for satellite communications, defense and wireless networks.

Is Sivers a pure AI-photonics company?

No. Sivers operates both Wireless and Photonics businesses. Wireless generated roughly 70% of 2025 revenue, and the company’s three largest customers during the year were all Wireless customers.

Is Sivers fabless?

Not entirely. Sivers operates a Photonics manufacturing facility in Glasgow but is also using WIN Semiconductors as an outsourced manufacturing partner to pursue larger-volume production. “Hybrid” or “fab-light” is more accurate than purely fabless.

Does Sivers’ $799 million pipeline equal backlog?

No. The figure represents an opportunity pipeline across Wireless beamformers and InP lasers. It includes potential business at different stages and should not be treated as contracted revenue or an order backlog.

What is the biggest risk to the Sivers investment thesis?

The central risk is commercialization: converting technical partnerships into qualified products, qualified products into allocated high-yield production, and production into customer-backed orders and positive per-share cash flow.

What would provide the strongest evidence for the bull case?

Disclosed AI data-center production orders, quantified qualified manufacturing capacity, demonstrated final product yields, sustained Photonics revenue growth and improving operating cash flow would materially strengthen the thesis.

Related Reading

CPO Isn’t Dead. The Timeline Is.

After the CPO Selloff: The Real Story Is Not the Death of Optical Stocks, but a Repricing of AI Infrastructure’s Transition Layer

NVIDIA’s Next Bottleneck Isn’t GPUs. It’s Data Movement.

Why AI factories are moving from copper to optical connectivity — and which suppliers deserve deeper research

AI Semiconductors Are No Longer Just About Compute. They Are About System Bottlenecks.

AI semiconductors are no longer just about raw compute. The real question is which system bottlenecks customers must solve next.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for informational and research purposes only and does not constitute investment advice. Small-cap semiconductor companies can involve substantial technology, execution, liquidity and dilution risks.

Comments