Editor's note: This article was originally published on Substack on June 6, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

Many investors missed Nvidia’s massive run over the past three years.

So the natural question is:

Where is AI’s next stop?

But if we frame the question as “Who is the next Nvidia?” we are already asking it the wrong way.

Nvidia’s rise was not just about selling more GPUs. The market eventually realized that GPUs were no longer just chips. They had become the core means of production in the AI era.

So the next opportunity will not simply be another company copying Nvidia.

The real question is:

As AI moves from model training to agent execution, where will the next bottlenecks appear? Which companies will become unavoidable in the next phase of the AI value chain?

That is the real lesson from GTC Taipei.

Most people watched Jensen Huang’s keynote and remembered a list of new products: Vera Rubin, Vera CPU, RTX Spark, Cosmos, Isaac GR00T, Alpamayo, Spectrum-X, and DSX.

But if we only focus on product names, we miss the bigger message.

The real message was this:

The customer of computing is changing.

In the past, computing mainly served humans. Now, computing is beginning to serve agents.

If that shift is real, the next decade of AI wealth redistribution will not be about one stock. It will be about a new set of control points across the computing stack.

1. Why “a New Customer” Matters So Much

The biggest opportunities in computing history usually did not come from one product getting better. They came when the primary customer of computing changed.

In the mainframe era, the customers were governments, banks, insurance companies, research institutions, and large enterprises. They were not buying a device. They were buying an entire system: hardware, software, maintenance, compatibility, and long-term service.

That is why IBM controlled the profit pool.

In the early 1960s, IBM held roughly two-thirds of the U.S. computer market. The IBM System/360 later generated more than $100 billion in revenue for the company.

The lesson is simple: when the customer was a large institution, the control point was not an individual component. It was the whole system, long-term service, compatibility, and customer lock-in.

Then came the PC era.

The customer changed from large institutions to individuals and office workers. Computing moved onto every desk. The control point shifted from vertically integrated machines to operating systems, CPU standards, and application ecosystems.

Windows 95 sold 7 million copies in its first five weeks and 40 million licenses in its first year. Microsoft and Intel became the defining winners of that era.

Then came mobile computing.

The customer changed again, from someone sitting in front of a PC to someone carrying a phone all day. The control points moved to smartphones, mobile operating systems, app stores, default search, advertising, payments, and mobile services.

Apple’s revenue grew from about $24 billion in fiscal 2007 to nearly $234 billion in fiscal 2015. By then, the iPhone accounted for roughly two-thirds of total revenue. Android, meanwhile, reached more than 3 billion monthly active devices, helping Google control one of the most important entry points into the mobile internet.

The key point is not that new platforms destroy old platforms.

Mainframes still exist. PCs still exist. Smartphones will not disappear because AI agents arrive.

What really happens is this:

Old platforms continue to operate, but incremental profit, developer attention, and capital market enthusiasm migrate toward the new computing interface.

So when we look at AI today, the real question is not:

Will AI replace all software tomorrow?

The better question is:

If the new customer of computing is no longer just humans, but agents, where are the new control points?

2. Agents Are Not Just Software Features. They Are New Computing Customers.

Many people still understand AI coding as “Copilot makes programmers faster.”

That is true, but it is not deep enough.

Microsoft’s 2023 controlled experiment on GitHub Copilot showed that developers using Copilot completed a JavaScript HTTP server task 55.8% faster. A 2024 enterprise field experiment involving 4,867 developers found that developers with access to AI coding assistants completed 26.08% more tasks.

These numbers matter. They show that AI coding tools can improve developer productivity in certain workflows.

But the deeper change is not that humans became somewhat faster.

The deeper change is that every human developer is starting to have a group of machine workers behind them.

GitHub Octoverse 2025 showed that GitHub saw nearly 986 million commits in 2025, up about 25% year over year, and 518.7 million merged pull requests, up 29%. More importantly, from May to September 2025, Copilot Coding Agent created more than 1 million pull requests.

OpenAI Codex data is even more direct. GPT-5-Codex processed more than 40 trillion tokens within three weeks of launch. Daily Codex usage increased more than 10x from early August 2025. Nearly all OpenAI engineers use Codex internally, and the number of pull requests merged per engineer increased by 70%.

Cursor’s data points in the same direction. Average tool calls per agent session rose from about 114 to 145, a roughly 30% increase in tool-call depth within two months.

Put these numbers together, and the message is clear:

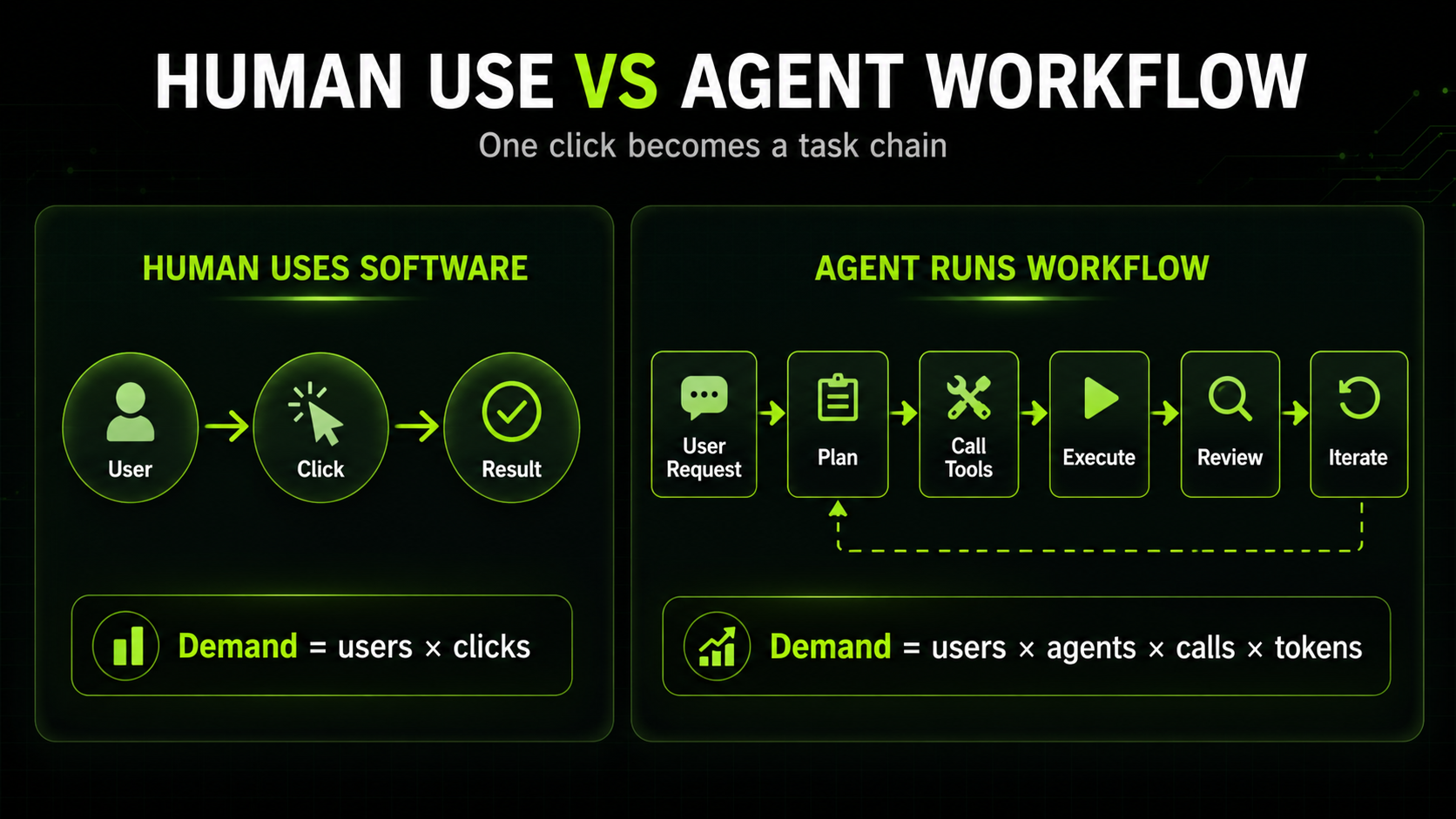

Agents are no longer just a feature that appears after a human clicks a button. They are beginning to read code, call tools, run tests, create pull requests, trigger CI, and participate in code review.

In the past, software compute demand looked roughly like this:

Human users × time spent × clicks.

In the agent era, compute demand looks more like this:

Human users × number of agents × task-chain length × tool calls × token depth.

That is the real shift.

Humans have biological limits. We sleep, eat, rest, hesitate, and get tired. Human clicks and inputs are naturally limited.

Agents do not have those limits.

They can reason continuously, run in parallel, operate in the background, call tools repeatedly, check their own work, and correct their own errors.

So AI agents are not merely new software features.

They are a new class of computing customer.

3. Why Agents Can Keep Pushing Compute Demand Higher

Some people argue that models are becoming more efficient, inference is getting cheaper, and AI infrastructure demand may soon peak.

That is an important argument.

The Stanford AI Index 2025 showed that GPT-3.5-level inference costs fell from $20 per million tokens in November 2022 to $0.07 per million tokens in October 2024, a decline of more than 280x in 18 months.

That is real bearish evidence for AI infrastructure.

But the problem is that agents are not ordinary chatbots.

A chatbot usually takes one input and produces one output.

An agent is different. An agent is a variable-length reasoning program.

It may plan first, then call tools. After the tool returns results, it reads them, reasons again, retries if necessary, generates multiple candidate paths, verifies them, filters them, and revises the answer.

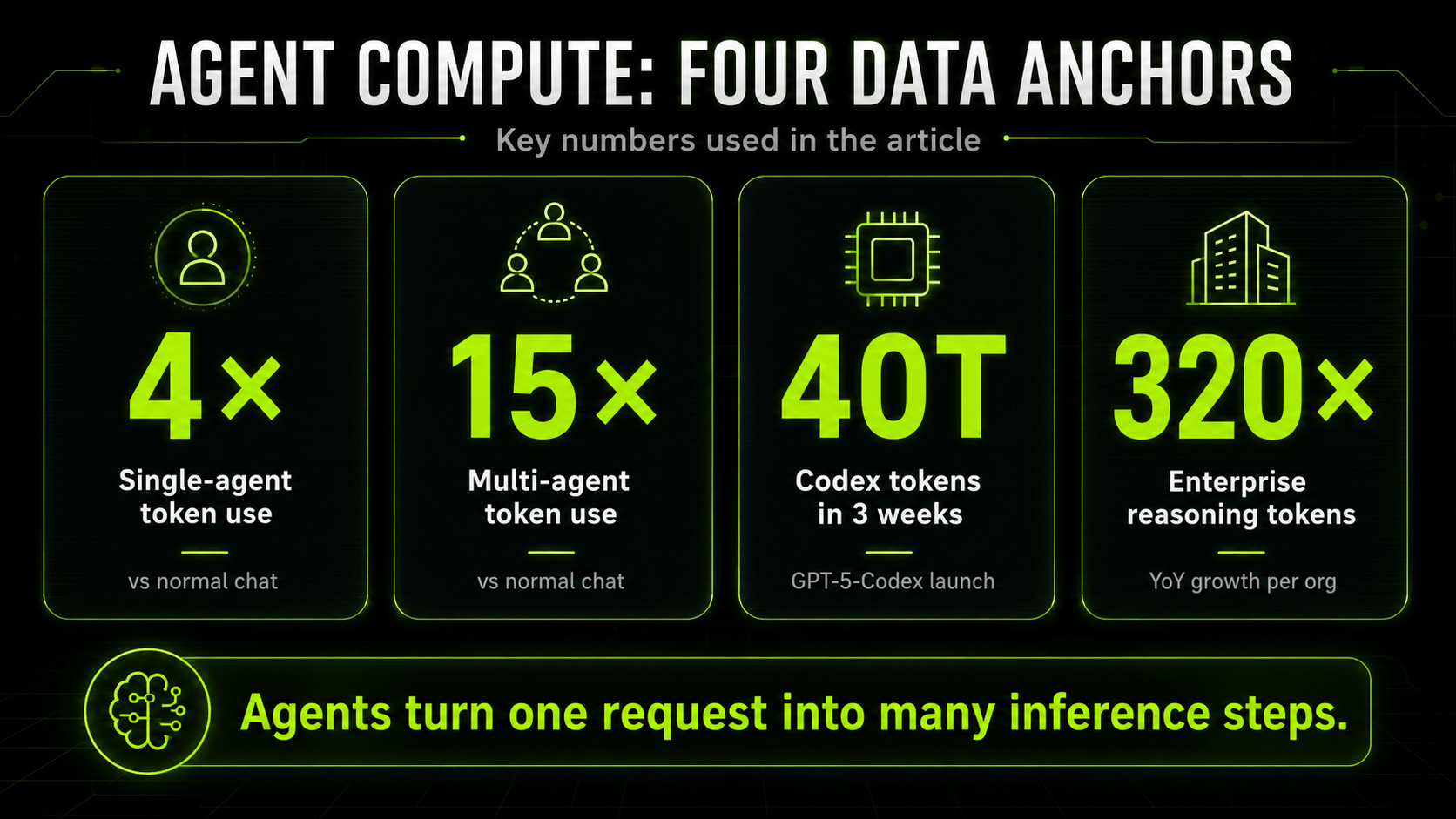

Anthropic’s multi-agent system found that a single agent typically uses about 4x more tokens than a normal chat interaction. A multi-agent system can use about 15x more tokens. Anthropic also found that token usage alone explained about 80% of performance differences in internal evaluations, while token usage, tool calls, and model choice together explained about 95%.

OpenAI’s enterprise AI report showed that reasoning-token consumption per organization increased roughly 320x year over year. More than 9,000 organizations processed over 10 billion tokens, and nearly 200 organizations processed more than 1 trillion tokens.

This means the next phase of AI is not just more people chatting with models.

It is more machines executing tasks in the background.

Even more importantly, one path to better AI performance is to spend more compute at inference time. OpenAI’s reasoning models, Google DeepMind’s Deep Think, multi-candidate reasoning, and test-time compute all point to the same idea:

Intelligence does not only come from training. It also comes from how much compute a model is allowed to spend while solving a task.

So falling inference prices do not automatically mean falling total compute demand.

If each inference call becomes cheaper, companies may embed agents into more workflows: coding, customer support, finance, marketing, search, data analysis, design, robotics, and autonomous driving.

This is the old technology rule:

When the unit cost falls, usage can explode.

Therefore, the key question for AI’s next phase is not whether people will keep using AI.

The real question is:

When agents start running at scale, which physical bottlenecks will be pushed to the front?

4. The Real Signal From GTC Taipei: Nvidia Is Rebuilding the Computing Stack Around Agents

Now we can understand GTC Taipei more clearly.

Vera Rubin is not just a new GPU platform. It is an AI-factory system. Nvidia says it delivers 10x higher agent throughput at scale compared with Grace Blackwell, and it is designed around compute, CPU, storage, and networking as one integrated system.

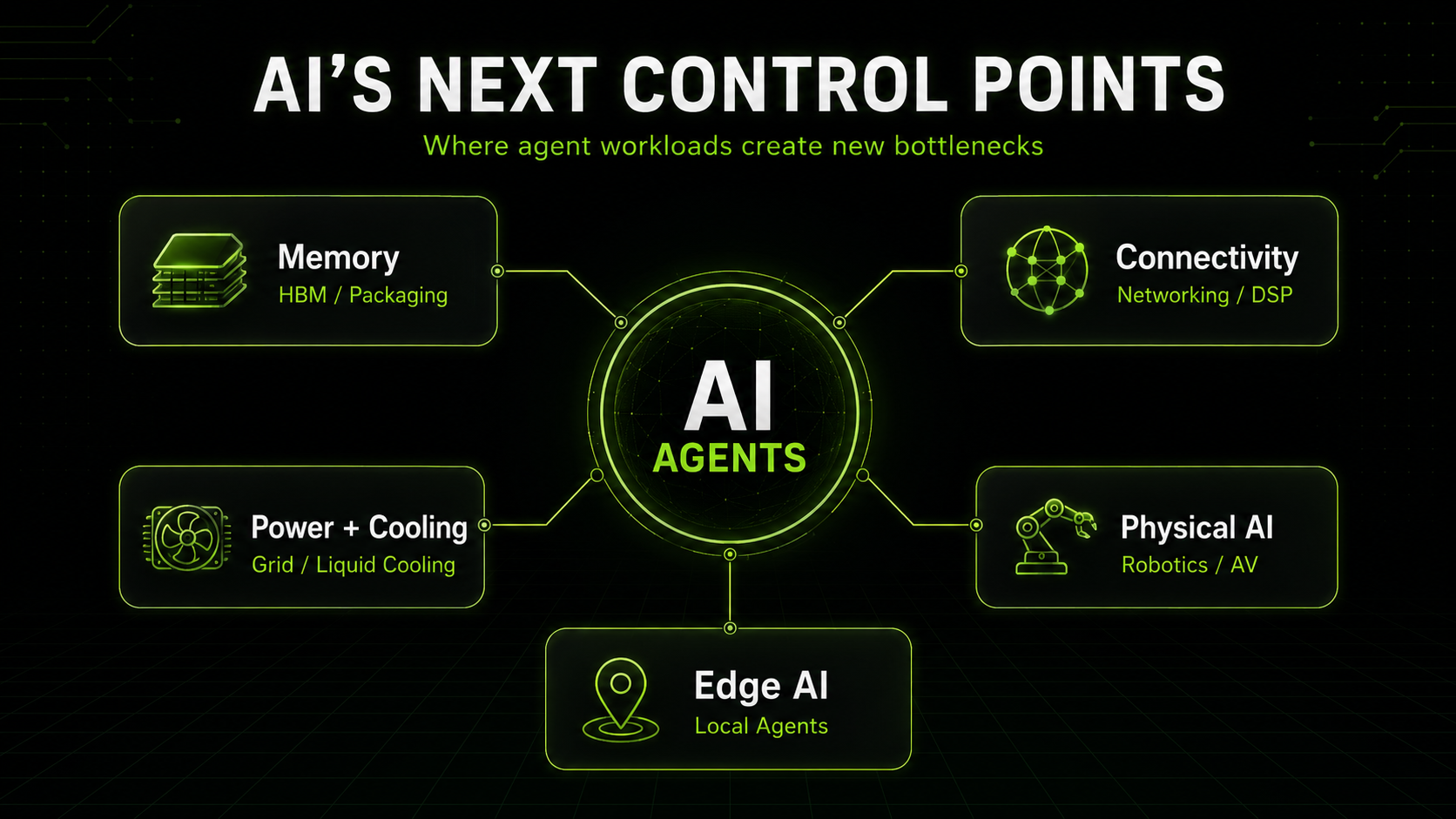

Vera CPU is even more important. Nvidia calls it the first CPU built for AI agents. It is designed to handle CPU-intensive tasks around GPU inference: Python execution, sandboxes, tool calls, orchestration, databases, and analytics.

It has 88 custom Olympus CPU cores, up to 1.2 TB/s memory bandwidth, and 1.8 TB/s coherent CPU-GPU bandwidth through NVLink-C2C.

This shows that agents do not only need GPUs.

They also need CPU scheduling, database access, tool execution, code execution, and secure sandboxes. Parts of the server architecture that used to look secondary may become critical bottlenecks in agent workflows.

RTX Spark points to the personal-computing layer. It is designed for local personal agents, with up to 1 petaflop of AI performance, up to 128GB unified memory, the ability to run 120-billion-parameter models locally, and support for context windows up to 1 million tokens.

That suggests the PC may not remain just a machine for human clicks and typing. It may become a local workstation for personal agents.

Cosmos and Isaac GR00T point to robotics. Alpamayo and DRIVE Hyperion point to autonomous driving. Spectrum-X Ethernet Photonics points to massive AI networking. DSX pushes AI-factory optimization toward tokens per megawatt.

These products may look scattered, but they are all serving the same new customer:

Cloud agents. Personal agents. Vehicle agents. Robot agents.

So GTC Taipei was not just a product launch.

It was Nvidia showing how the computing stack must be redesigned when agents become the largest new users of computing.

5. AI’s Next Stop: Do Not Look for Cheap AI Stocks. Look for Unavoidable Companies.

If agents become the new computing customer, the next opportunity will not only be in GPUs.

The real task is to identify the unavoidable control points of the agent era.

And here, valuation alone is not the first filter.

An expensive company may still be a core winner. A cheap company may still be a value trap.

The first questions should be:

Is this company unavoidable? Is it in a position that customers must buy, ecosystems must support, and competitors cannot easily replace? Can it turn demand growth into revenue, profit, and free cash flow?

Valuation determines the entry point. It does not determine strategic importance.

From this perspective, there are three major AI infrastructure lines to watch.

The first is HBM, memory bandwidth, and advanced packaging.

Agents need long context, multi-step reasoning, KV cache, tool calls, and persistent state. The longer the task chain, the more important memory bandwidth and capacity become.

SK hynix expects HBM demand to grow roughly 30% annually through 2030. Counterpoint forecasts HBM bit demand from AI accelerators to increase 35x from 2024 to 2028. TrendForce expects HBM consumption growth above 70% in 2026, after more than 130% growth in 2025.

The unavoidable companies here include SK hynix, Micron, Samsung, TSMC, ASE, Lam Research, Applied Materials, and KLA.

But memory is still cyclical.

HBM is a real bottleneck, but it is not a risk-free perpetual-growth machine. Samsung qualification, the transition from HBM3E to HBM4, capacity expansion, and yield improvement can all change the supply-demand balance.

So in this layer, the goal is not to chase the hottest small-cap name. It is to identify companies with real technical leadership, customer relationships, and manufacturing advantage.

The second line is AI networking, optical connectivity, and the connection layer.

If the last phase of AI was about GPUs, the next phase may be about connectivity.

The reason is simple: an AI cluster is not just a pile of GPUs.

As GPU counts move from thousands to tens of thousands, hundreds of thousands, and eventually million-GPU AI factories, the bottleneck shifts from whether a single chip is fast enough to whether data can move fast enough across the whole system.

This is especially true for agent workloads. Model state, context memory, KV cache, tool results, storage access, and distributed inference data all need to move across chips, servers, racks, and data centers.

At that point, AI-factory efficiency is not only about GPU compute. It is also about system-level data movement.

That is where Marvell becomes important.

Marvell is not just a generic optical-module company. It sits at the intersection of custom AI silicon, optical DSPs, data-center networking, silicon photonics, and AI-cluster interconnect.

Jensen Huang’s comment in Taipei that Marvell could become the next trillion-dollar company should not be treated as a buy signal. But it does tell us what Nvidia sees as the next major bottleneck: not just GPUs, but the connection layer.

Broadcom belongs on the same map. Its strength lies in custom AI ASICs, Ethernet switching, and custom silicon programs for large cloud customers. Arista represents high-quality AI Ethernet networking. Coherent, Lumentum, Fabrinet, Ciena, Credo, and AAOI sit in different parts of the optical components, manufacturing, transport, and module chain.

But this layer cannot simply be summarized as “optical stocks are good.”

The real question is who controls unavoidable parts of data movement inside AI clusters:

Custom AI silicon. Optical DSPs. Ethernet switching. High-end lasers. Optical-electrical conversion. System-level networking architecture.

Marvell’s position should be understood correctly: it is a core watchlist company in the AI connection layer.

But investors should not chase it blindly just because it was named by Huang.

The valuation data shows that Marvell already has a market cap above $230 billion, with a forward P/E around 65x and EV/Sales above 26x. Its strategic importance has risen, but the stock still needs earnings delivery, durable orders, and a better margin of safety to justify aggressive entry.

The third line is power, cooling, and data-center infrastructure.

The IEA estimates that global data-center electricity consumption will rise from roughly 415 TWh in 2024 to about 945 TWh by 2030. U.S. data centers may account for nearly half of electricity-demand growth through 2030.

Meanwhile, AI-optimized racks are moving from tens of kilowatts toward 100–200 kW or more, which increases the need for liquid cooling.

This is the most basic and longest-duration bottleneck.

No matter which GPU generation wins, no matter which model architecture wins, electricity, cooling, transformers, switchgear, grid connection, construction, and land are unavoidable physical constraints.

The key companies here include Vertiv, Eaton, Schneider Electric, GE Vernova, Siemens Energy, Quanta Services, Hubbell, Trane, Caterpillar, and Cummins.

But the market has already noticed this theme. Vertiv is up nearly 14x over the past three years. Eaton and GE Vernova have also been heavily rerated.

So the conclusion is not that these companies are uninvestable. The conclusion is that investors cannot treat today’s strong order cycle as permanent growth at any price.

Great companies still need good entry points.

6. From Cloud Agents to Personal Agents: Why AI PCs Matter

So far, the strongest bottlenecks are still inside the AI infrastructure stack: memory bandwidth, networking, power, cooling, and advanced packaging.

But GTC Taipei also pointed to another direction.

Agents will not stay inside cloud data centers forever.

If agents become a new class of computing customer, they will eventually move closer to the places where work actually happens. And for many high-value tasks, that place is still the PC.

This is why AI PCs matter.

Not because the PC is a new platform after the smartphone. It is not. The PC came first. The smartphone became the dominant consumer interface later.

The real point is different:

The smartphone is the best device for short consumer interactions. The PC is still the main device for complex productivity work.

Coding, writing, spreadsheets, research, presentations, design, finance, data analysis, browser workflows, enterprise software, file management, and internal tools still mostly live on the PC.

That matters because the first high-value agent workloads are not entertainment tasks.

They are work tasks.

A phone can answer a quick question. But an agent that reviews a contract, rewrites a presentation, analyzes a spreadsheet, searches company files, edits code, automates a browser workflow, or coordinates multiple applications needs access to files, permissions, windows, browsers, terminals, IDEs, office software, and enterprise systems.

That environment is the PC.

This is why AI PCs became one of the first consumer-device themes in the agent era.

The technical path is relatively clear: stronger NPUs and GPUs, more memory, higher bandwidth, local models, safer permission systems, and software that allows agents to operate across applications.

Gartner once forecast about 114 million AI PCs in 2025, or around 43% of PC shipments. Omdia forecasts edge AI acceleration hardware to grow from roughly $43 billion in 2024 to about $89.7 billion in 2029.

Those numbers show the potential market is large.

But for investors, shipment volume is not the key question.

The key question is incremental profit.

If AI PCs simply add NPUs to existing devices, but users do not pay more and enterprises do not change upgrade behavior, then AI PC may become a replacement-cycle label rather than a new profit pool.

The real investment question is:

Will the PC become the operating surface for personal and enterprise agents?

If yes, value may flow to the companies that control the productivity stack: operating systems, local AI chips, memory, enterprise software, identity, security, and developer tools.

So AI PCs are not a science problem.

They are a commercialization problem.

They may become the first mainstream device category where agents create real workflow value. But the market still needs to prove that local agents can drive upgrade demand, software monetization, and enterprise adoption.

7. From Digital Agents to Physical Agents: Why Robotics Is Harder

If AI PCs are where agents return to the productivity terminal, robotics is where agents try to leave the screen entirely.

That is a much harder problem.

A software agent operates inside files, browsers, code, documents, APIs, and enterprise permissions.

A robot operates inside kitchens, factories, warehouses, roads, hospitals, and homes.

The underlying loop is similar:

perceive, reason, plan, act, observe, and correct.

But the physical world makes every step harder.

A robot cannot just generate an answer. It has to see the environment, understand spatial relationships, identify objects, predict human behavior, plan motion, control its body, use hands, avoid accidents, and stay safe around people.

That requires more than a language model.

It requires world models, vision AI, motion control, tactile feedback, dexterous hands, low-cost actuators, reducers, batteries, sensors, edge inference, simulation, and massive amounts of real-world training data.

This is why robotics belongs in the same long-term agent thesis, but not in the same near-term certainty bucket as AI PCs.

AI PCs bring agents into an existing digital work environment. Robotics brings agents into the physical world.

The market potential is enormous.

The IFR recorded about 542,000 industrial robot installations in 2024, with annual industrial robot installation value around $16.7 billion. Goldman Sachs projects a potential $38 billion humanoid market by 2035. McKinsey estimates autonomous-driving revenue could reach $300–400 billion by 2035.

Those numbers are exciting, but the constraints are still serious.

Many humanoid robots still operate only 2–4 hours per charge, while an industrial shift usually requires 8–12 hours. Advanced safe systems can cost around $150,000 to $500,000 in the U.S., while mass adoption may require costs to fall toward $20,000 to $50,000.

And the hardest market is not the factory.

It is the home.

Factories are structured environments. Homes are messy, unpredictable, and full of edge cases. A robot that works in a warehouse does not automatically become a robot that can enter millions of households.

That is why useful household robots are more likely a 10-year journey than a near-term consumer cycle.

So robotics should stay in the article, but in the right position.

It is not a near-term AI PC story. It is not just another endpoint device. It is the long-term physical extension of the agent thesis.

For investors, the safer way to study physical AI is not to blindly chase humanoid stories. It is to track the unavoidable components underneath: vision AI, world models, sensors, dexterous hands, actuators, reducers, batteries, edge compute, and simulation platforms.

Robotics may become one of the biggest AI markets of the next decade.

But investors should not price a 10-year household robot story as if it were today’s profit.

8. The Biggest Risk: AI Usage Can Explode While Stocks Still Disappoint

This article should not be read as blindly bullish on every AI infrastructure stock.

The biggest risk is not that nobody uses AI. AI usage will most likely keep growing.

The real risk is different:

AI usage growth does not guarantee good returns for every infrastructure supplier at today’s valuation.

First, capex may be running ahead of revenue.

Sequoia’s “AI’s $600B Question” raised the issue of a massive revenue gap implied by AI infrastructure investment. Microsoft’s 2025 annual report showed property and equipment additions rising from $44.5 billion to $64.6 billion, while depreciation expense rose from $15.2 billion to $22.0 billion. Microsoft also warned that AI investment may pressure operating margins.

AI growth is not cost-free.

Second, inference prices are falling quickly.

GPT-3.5-level inference cost fell more than 280x in 18 months. If token demand does not grow faster than price declines, revenue growth for parts of the infrastructure stack may disappoint.

Third, custom silicon can take share from general-purpose GPUs.

Meta MTIA, AWS Trainium, and Google TPU all show that large cloud companies will not rely only on Nvidia forever. Stable, large-scale, specific inference workloads may gradually move to custom chips.

Fourth, enterprise agent adoption is still shallow.

McKinsey’s State of AI 2025 found that 62% of organizations were experimenting with agents, but only 23% reported scaling an agent system somewhere. In any individual function, no more than 10% were scaling agents. Gartner also expects more than 40% of agentic AI projects to be canceled by the end of 2027 because of cost, unclear value, or insufficient controls.

So the right conclusion is not “AI is a bubble” or “AI stocks can only go up.”

The more accurate conclusion is:

AI agent demand will grow, but infrastructure returns will diverge.

Some companies will control real bottlenecks and earn pricing power. Some will be rerated at the top of a cycle. Some will generate revenue without strong profits. Some will have the right story but already price in five years of growth.

9. Conclusion: If You Missed Nvidia, Do Not Chase Every AI Story. Find the Control Points.

Missing Nvidia’s massive run does not mean missing AI.

But if you are still trying to find “the next GPU company,” you may miss the real next stop.

The last phase of AI rerated GPUs.

The next phase will likely rerate the bottlenecks of the agent era:

Memory bandwidth. Network bandwidth. Power. Cooling. Advanced packaging. Edge compute. Physical sensing and actuation.

But investors should not simply buy cheap AI names. They also should not reject core companies just because they look expensive.

The real goal is to find unavoidable high-quality companies.

They must sit in a required part of the agent workflow. Without them, agents cannot run fast enough, cheaply enough, or reliably enough.

They must have supply constraints or technical barriers. When demand rises, can they raise prices? Are customers forced to compete for capacity? Is the technology hard to replicate?

They must turn revenue into profit and free cash flow. AI revenue is not enough. AI profit matters.

They must not rely only on distant stories. AI PCs and robotics may become huge, but if near-term revenue is unclear, investors cannot pay today for a future that has not yet arrived.

Finally, valuation determines the entry point. It does not determine strategic importance.

Marvell is expensive, but it is a core watchlist company in the AI connection layer. Vertiv is expensive, but power and cooling remain unavoidable. Micron may look cheaper, but memory cyclicality cannot be ignored. AAOI may have huge upside, but its customer concentration and financial quality make it more of a high-volatility trade than a core holding.

So AI’s next stop is not one ticker.

The next stop is the migration of control points in computing.

In the past, computing served humans. Now, computing is beginning to serve agents.

When the customer changes, the control points change. When the control points change, the profit pool gets redistributed.

That is the real lesson from GTC Taipei.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-06 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments