Editor's note: This article was originally published on Substack on June 5, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

Most investors still describe the AI infrastructure boom in one simple sentence:

More AI models need more GPUs.

That is true, but it is no longer the full story.

The next bottleneck is not just compute. It is data movement.

As AI data centers scale into what NVIDIA calls “AI factories,” the key question becomes:

How do thousands of GPUs, CPUs, switches, racks, and servers communicate with each other at high speed, low latency, and reasonable power consumption?

That question is moving optical connectivity from a background component into a central AI infrastructure theme.

My view is clear:

NVIDIA remains the platform company. But the higher-beta opportunity may increasingly sit in the suppliers that help AI factories move data — optical components, silicon photonics, CPO, high-speed transceivers, optical DSPs, fiber, and related connectivity silicon.

This is not a buy list.

It is a supply-chain map.

The goal is to understand which companies solve the physical bottleneck before the market fully prices in the business impact.

The Core Thesis

AI factories are not just bigger data centers.

A normal factory turns raw materials into physical products.

An AI factory turns data and electricity into intelligence.

But an AI factory does not work just because it has more GPUs. Those GPUs need to communicate constantly. They exchange model parameters, training data, memory traffic, inference outputs, and networking signals at enormous scale.

The GPU is the engine.

The network is the nervous system.

If the nervous system is too slow, the entire AI factory becomes inefficient.

That is why the AI infrastructure story is shifting from “how many GPUs can you buy?” to “how efficiently can those GPUs talk to each other?”

This is where copper starts to hit a wall.

Why Copper Starts to Lose Advantage

Copper has been the default way to move electrical signals over short distances for decades.

It is cheap, familiar, and deeply embedded in data centers.

But AI clusters are not normal server clusters. They are increasingly dense, power-hungry, and bandwidth-hungry. As systems scale from racks to rows to full AI factories, copper faces four problems:

- Bandwidth demand keeps rising.

- Distance becomes harder to manage.

- Power consumption increases.

- Signal integrity becomes more difficult.

This does not mean copper disappears tomorrow.

It means that as AI factories scale, parts of the connectivity stack need to move toward optical solutions.

That is why optical fiber, silicon photonics, co-packaged optics, and high-speed optical modules matter.

They are not buzzwords.

They are possible solutions to the data-movement bottleneck.

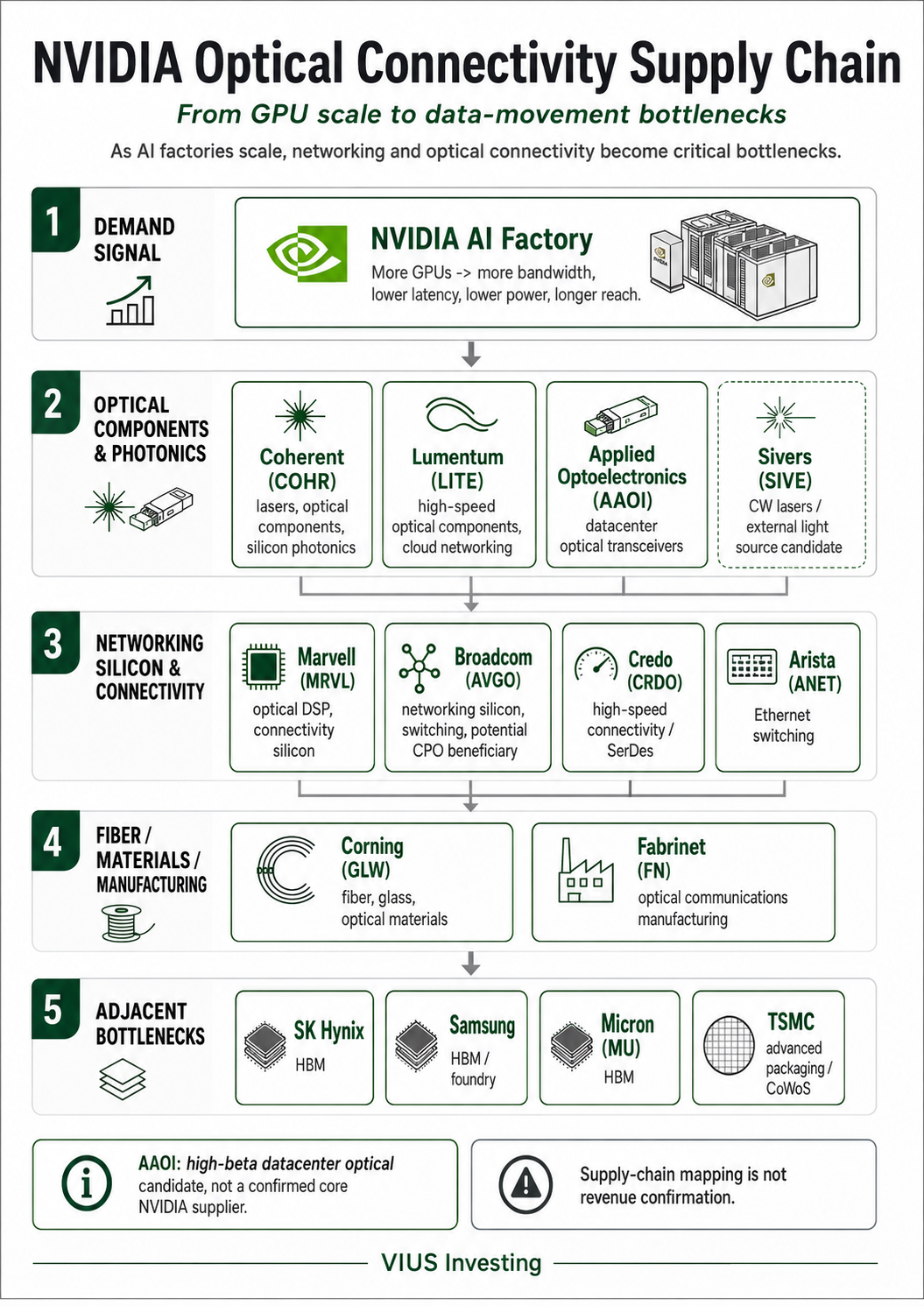

The Supply Chain Map

Here is the simplified map of the NVIDIA optical/connectivity supply chain:

The map above shows the major layers of the NVIDIA optical/connectivity supply chain.

The most important point is that these companies do not play the same role.

Coherent and Lumentum are closer to optical components and photonics.

Marvell, Broadcom, and Credo are closer to connectivity silicon, optical DSPs, SerDes, and networking architecture.

Corning and Fabrinet sit in the fiber, materials, and manufacturing layer.

AAOI is a smaller, higher-beta datacenter optical transceiver candidate. It can benefit from market enthusiasm around AI optical demand, but it should not be treated as a confirmed core NVIDIA supplier without stronger customer evidence.

Sivers is an example of a deeper, less obvious CPO laser chokepoint thesis. It is useful for understanding how investors look for hidden bottlenecks, but customer mapping still needs to be separated from revenue confirmation.

SK Hynix, Samsung, Micron, and TSMC are adjacent bottleneck suppliers through HBM memory and advanced packaging. They are critical to the broader AI factory, but they are not direct optical-connectivity names.

This distinction matters because supply-chain relevance is not the same as confirmed revenue exposure.

The key point is that these companies do not play the same role.

Coherent and Lumentum are closer to optical components and photonics.

Marvell and Broadcom are closer to connectivity silicon, custom chips, optical DSPs, and networking architecture.

Corning is a second-order infrastructure candidate through glass, fiber, and optical materials.

AAOI is a smaller, higher-beta datacenter optical transceiver candidate.

Sivers is an example of a deeper, less obvious CPO laser chokepoint thesis.

SK Hynix, Samsung, and Micron are adjacent bottleneck suppliers through HBM memory, but they are not optical connectivity companies.

A good investor should not put all of these companies in one basket.

The right question is:

Which company solves which bottleneck, and can that bottleneck turn into revenue, margin, and free cash flow?

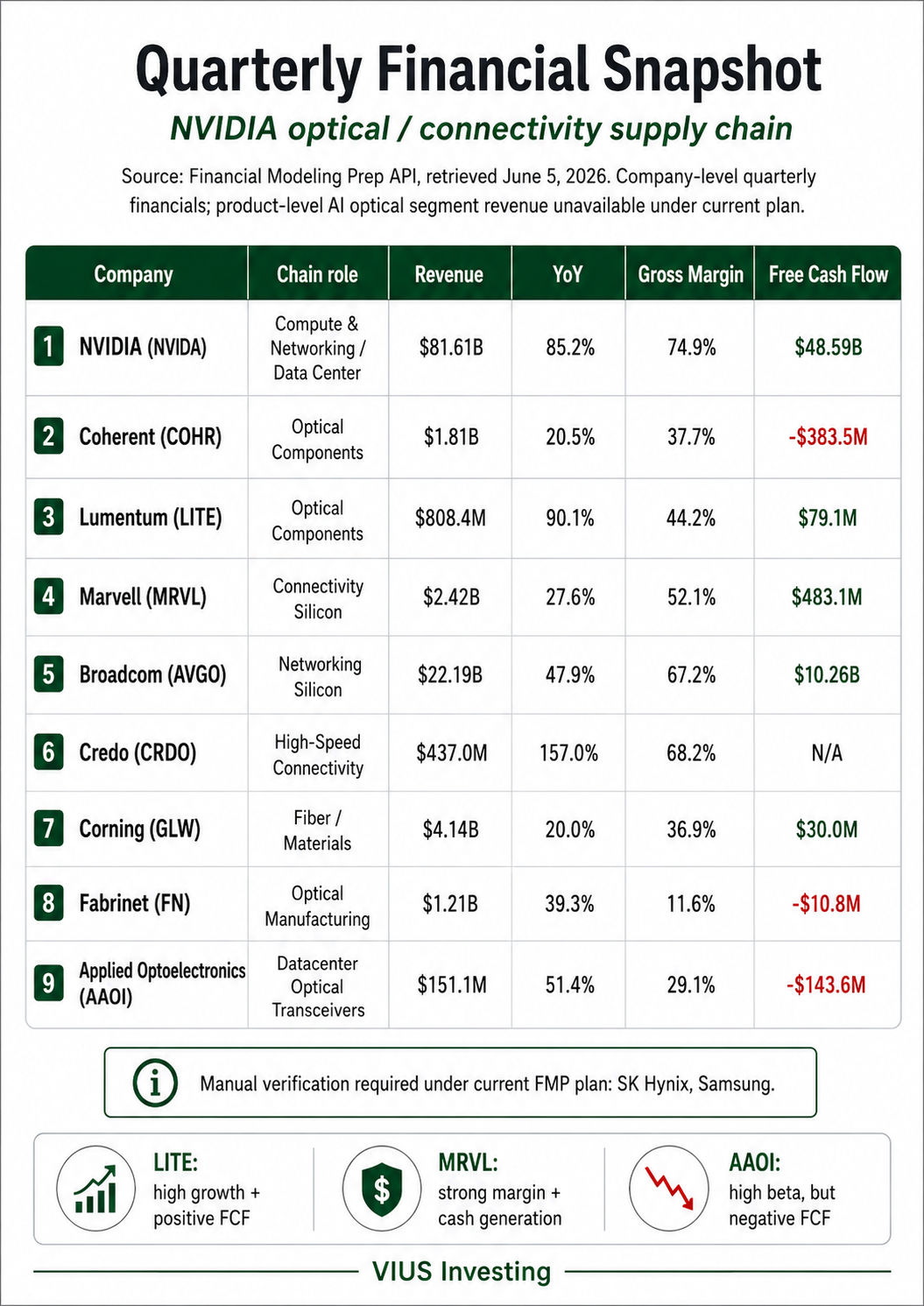

Quarterly Financial Snapshot

The table below uses company-level quarterly financials from Financial Modeling Prep, retrieved on June 5, 2026.

Important limitation: product-level or segment-level revenue was not reliably available under the current FMP plan. That means the revenue numbers below are company-total quarterly revenue, not direct AI optical-connectivity revenue. The “relevant chain” label shows where each company may sit in the NVIDIA optical/connectivity supply chain.

This table tells us something important.

The optical/connectivity theme is real, but the companies inside it have very different business quality.

NVIDIA has extraordinary scale, margins, and free cash flow. It is the platform.

Broadcom has scale, margin quality, and strong free cash flow, but it is not a pure optical-connectivity play.

Marvell has meaningful data-center exposure, good margins, and positive free cash flow.

Lumentum shows strong growth and positive free cash flow, which makes it one of the more interesting optical names to verify.

Credo shows very high growth and strong gross margin, but it is smaller and more volatile.

AAOI shows strong revenue growth, but also negative free cash flow and smaller scale.

Coherent has a larger revenue base, but its reported quarter showed negative free cash flow.

Corning is financially stable, but its AI optical exposure needs more direct verification.

So the conclusion is not “buy every optical stock.”

The conclusion is:

The theme is strong, but company quality varies sharply.

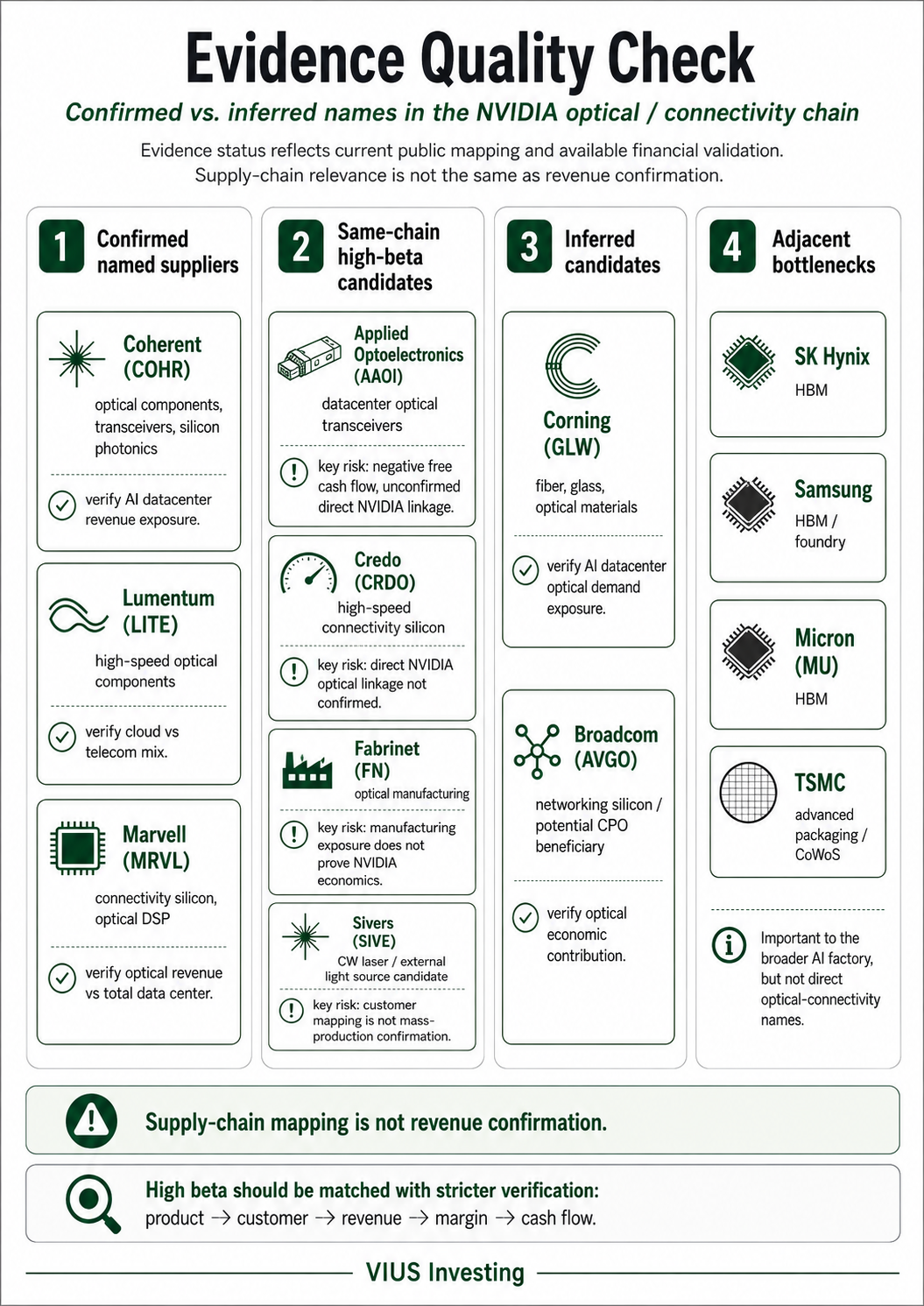

Evidence and Data Quality Check

A stock can be in the right supply chain and still lack confirmed revenue exposure.

That distinction matters.

This is the most important table in the article.

It prevents the biggest mistake in AI investing:

Confusing supply-chain relevance with confirmed revenue.

A company can be relevant to the theme without being a confirmed beneficiary.

A confirmed supplier can still have weak margins.

A high-growth company can still burn cash.

A stock can rally before the business model is proven.

That is why evidence quality matters.

The Confirmed View: Data Movement Is Becoming a Real Bottleneck

There are three conclusions I am comfortable stating clearly.

First, data movement is becoming a real AI infrastructure bottleneck.

AI factories require more than GPUs. They require networking, memory, optical connectivity, power, cooling, and packaging.

Second, optical connectivity is one of the most important second-order themes inside the NVIDIA chain.

The shift from copper toward optical is not just a market story. It is a physical response to bandwidth, distance, power, and signal-integrity constraints.

Third, the highest beta is unlikely to be in the most obvious mega-cap names.

NVIDIA is the platform. Broadcom and Marvell are large strategic players. But the sharper stock moves may come from smaller companies where a single theme can change the growth profile.

That is where names such as Lumentum, Credo, AAOI, Sivers, and other specialized optical suppliers become worth studying.

But high beta is not the same as high quality.

What High-Beta Optical Research Gets Right — and Where It Can Go Wrong

One reason the optical-connectivity theme has become so interesting is that investors are no longer looking only at the obvious winners.

They are moving deeper into the supply chain.

A good example is the recent work from Serenity, who has been widely followed for mapping Sivers into the CPO and photonics supply chain. The Sivers thesis is not simply “AI needs optical.” It goes one layer deeper: if co-packaged optics becomes more important for future AI clusters, then external light sources and CW lasers may become a bottleneck.

That is the kind of thinking worth studying.

The method starts with the mega-cap roadmap, then asks a more specific question:

What small component does the larger system need but the market may not fully understand yet?

In the Sivers case, the argument is built around customer and partner mapping. The thesis connects Sivers to optical ecosystems such as Jabil, POET, Ayar Labs, O-Net, Enablence, Lightium, and other photonics/CPO routes. From there, the mapping extends toward larger end customers and hyperscaler ecosystems such as Apple, AMD, Amazon, Microsoft, Meta, Google, and others.

This is exactly how high-beta supply-chain ideas are often discovered before they become consensus.

The research process is valuable because it does not stop at the headline company. It tries to trace the chain:

NVIDIA or hyperscaler roadmap → CPO / optical architecture → external light source or laser requirement → supplier ecosystem → possible end customer → future revenue opportunity.

That is much more useful than simply asking which optical stock went up the most.

But there is also a serious risk.

Customer mapping is not revenue confirmation.

A company can appear in the right ecosystem and still fail to reach mass production. A supplier can be technically relevant but economically small. A relationship can be real but not material. A product can be designed into a prototype and still never become a major revenue line.

This is the difference between a supply-chain thesis and a business-model thesis.

The supply-chain thesis asks:

Could this company sit in the right place?

The business-model thesis asks:

Can this company convert that position into revenue, margin, free cash flow, and durable competitive advantage?

Both questions matter.

But the second question is what ultimately decides whether the investment works.

This is also how I would frame Applied Optoelectronics.

AAOI is not the core evidence behind the NVIDIA optical-connectivity thesis, and I would not treat it as a confirmed core NVIDIA supplier based on current public evidence. But it is a useful example of how the market trades smaller, higher-beta optical names when a theme becomes hot.

AAOI sits in datacenter optical transceivers. If AI factories need more optical connectivity, then companies exposed to datacenter optics can become thematic proxies. That helps explain why AAOI has attracted strong market attention.

But the same discipline applies:

Strong stock performance does not prove direct NVIDIA revenue exposure.

AAOI may be a valid high-beta same-chain candidate, but investors still need to verify customer qualification, AI datacenter revenue exposure, margin durability, and cash-flow improvement.

The lesson from Serenity’s Sivers research and AAOI’s stock move is not that every optical small-cap should be bought.

The lesson is more important:

When a new AI infrastructure bottleneck emerges, the market first rewards the obvious names. Then it starts searching for smaller, less obvious chokepoints.

That is where high beta lives.

But high beta should come with stricter verification, not looser verification.

The right process is:

Identify the bottleneck. Map the possible suppliers. Separate confirmed relationships from inferred relationships. Verify customer path. Then check revenue, margin, cash flow, and valuation.

That is the difference between discovering a real supply-chain opportunity and chasing a story.

How I Would Rank the Optical Chain Today

Based on evidence quality, business relevance, and financial data availability, I would separate the names into four groups.

1. Core companies to research first

Coherent, Lumentum, and Marvell.

These are the names most directly connected to the optical/connectivity thesis in the current research set.

Lumentum stands out because of its strong revenue growth, positive free cash flow, and optical component exposure.

Marvell stands out because data movement increasingly requires connectivity silicon, optical DSPs, and custom interconnect architecture.

Coherent remains important because of optical components and photonics, but its free cash flow profile needs more work.

2. High-quality but less pure plays

Broadcom and Corning.

Broadcom has scale, margin, and free cash flow, but its business is diversified.

Corning has the right materials and fiber logic, but AI datacenter revenue exposure needs direct verification.

These are not bad names. They are just less pure optical-connectivity bets.

3. High-beta candidates

Credo, AAOI, Fabrinet, and Sivers.

These names can move more sharply because they are smaller, more specialized, or more tied to narrow supply-chain narratives.

But they also require stricter verification.

For these companies, the key question is not whether the theme is exciting.

The key question is whether the company can turn the theme into revenue, margins, and cash flow.

4. Adjacent bottlenecks

SK Hynix, Samsung, Micron, and TSMC.

These are critical to AI factories, but they are not optical connectivity names.

They belong in the broader NVIDIA chain because HBM and advanced packaging are also physical bottlenecks.

But they should not be confused with the optical/CPO thesis.

What Investors Should Verify Next

Before calling any company a true AI infrastructure winner, I would verify eight things:

- What exact product solves the bottleneck?

- Is the company named by a customer, partner, or official source?

- Is there segment-level revenue tied to AI datacenters?

- Are gross margins improving because of AI demand?

- Is free cash flow improving?

- Is capacity constrained?

- Is customer concentration manageable?

- Has the stock already priced in the next several years of growth?

The last question may be the most important.

A real technology trend can still become a bad investment if the valuation already assumes perfection.

The Bottom Line

NVIDIA’s AI story is no longer only about GPUs.

As AI factories scale, data movement becomes a core bottleneck.

That makes optical fiber, silicon photonics, co-packaged optics, high-speed optical modules, optical DSPs, and networking silicon more important.

The companies worth researching are not all the same.

Coherent and Lumentum are closer to optical components.

Marvell and Broadcom are closer to connectivity silicon.

Corning is a fiber and materials candidate.

AAOI is a high-beta datacenter optical transceiver candidate.

Sivers is an example of a deeper CPO laser chokepoint thesis.

SK Hynix, Samsung, Micron, and TSMC remain adjacent bottleneck suppliers through memory and packaging.

My core conclusion is simple:

The next layer of AI infrastructure opportunity is not just compute.

It is the physical system that lets compute scale.

But the investment process must stay disciplined.

Do not buy a stock because it appears in an AI map.

Start with the bottleneck.

Then verify the product, customer, revenue, margin, cash flow, and valuation.

That is the difference between chasing market noise and understanding the business.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-05 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments