Editor's note: This article was originally published on Substack on June 10, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

Over the past few days, AI optical names have suddenly become one of the most sensitive corners of the market.

Stocks linked to optical modules, silicon photonics, co-packaged optics, lasers, and AI networking — including AAOI, LITE, COHR, GLW, MRVL, and SIVE — came under heavy pressure.

On the surface, the selloff looked like a reaction to a bearish report from SemiAnalysis on the CPO timeline. But if we reduce the story to “CPO is being questioned,” we miss the more important signal.

The market is not really debating whether CPO has a future.

The real question is:

Will CPO become a meaningful revenue driver in 2027–2028, or will it remain in a longer phase of introduction, qualification, and production ramp?

That is why this selloff looks less like a breakdown of the AI infrastructure thesis, and more like a repricing of the CPO adoption curve.

1. What Happened: How the Debate Started

The debate appears to have intensified around June 9, 2026.

SemiAnalysis reportedly released a note to institutional clients discussing NVIDIA’s 800V DC and CPO roadmap. According to market summaries, the report suggested that broad adoption of NVIDIA’s 800V DC architecture may be delayed, that CPO shipments in 2027 could fall short of aggressive market expectations, and that mass production may move closer to the 2028–2029 timeframe.

At the same time, 400V DC was still expected to progress, while some NPO projects could potentially accelerate.

After the report, U.S.-listed optical communication names sold off sharply. AAOI, COHR, LITE, GLW, and MRVL all came under pressure. The hardest-hit names were not necessarily NVIDIA or Broadcom, but the higher-beta optical names that had previously rallied on the CPO and AI optical interconnect narrative.

That distinction matters.

The market was not punishing the entire AI data center capex cycle. It was punishing the part of the optical chain that had already priced in a very aggressive CPO ramp.

Then the debate became more heated after NVIDIA-related comments and supply-chain bulls pushed back. NVIDIA networking executives had previously described CPO more positively, arguing that the technology was moving forward rather than being abandoned. At the same time, Serenity — a popular independent AI supply-chain researcher — publicly disagreed with the conservative interpretation.

So the market ended up with two camps.

On one side is SemiAnalysis.

SemiAnalysis is one of the most influential research firms covering semiconductors and AI infrastructure. It follows GPUs, advanced packaging, HBM, data center networking, AI servers, chip supply chains, and cloud capex. Its style is engineering-heavy. It tends to focus on system cost, yield, power, packaging, testing, reliability, serviceability, and the real pace of deployment.

In this debate, SemiAnalysis is not saying that CPO has no future. Its argument is more subtle: CPO may take longer to scale than the market expects.

The reason is that CPO is not simply a better optical module. It moves the optical engine closer to the switch ASIC and pushes more complexity into the package and system architecture. That can improve power efficiency and bandwidth density, but it also makes manufacturing, testing, repair, yield management, and customer qualification more difficult.

On the other side is Serenity.

Serenity is an independent researcher who has become popular in AI supply-chain investing circles. Her style is very different from traditional sell-side research. She looks for early signals across technology roadmaps, supplier announcements, small-cap filings, open-source communities, developer ecosystems, and industry forums.

She became well known because she identified several high-beta AI infrastructure and photonics-related stocks before they were widely discussed by mainstream investors.

Serenity disagrees with the conservative CPO timeline. Her argument is that SemiAnalysis may be underestimating NVIDIA’s ability to compress hardware cycles and coordinate its supply chain. If AI factories are increasingly constrained by networking bandwidth, power consumption, and switching density, NVIDIA has a strong economic incentive to push CPO forward faster than a traditional engineering model would suggest.

So this is not really a debate about whether CPO is real.

It is a clash between two research frameworks.

SemiAnalysis represents the engineering-conservative view: even if the technology direction is right, large-scale deployment must pass through yield, reliability, serviceability, and customer qualification.

Serenity represents the forward-looking supply-chain view: traditional hardware timelines may not fully apply when NVIDIA is driving an AI infrastructure cycle with enormous capex intensity and strong supplier coordination.

The real disagreement is this:

Is CPO a 2027–2028 revenue ramp story, or is it still mainly a qualification and deployment-readiness story?

2. Why Optical Stocks Led the Selloff

Over the past several months, investors did not buy optical stocks for today’s revenue. They bought them for the expected migration of next-generation AI data center networking.

As training and inference clusters scale, communication between GPUs, racks, and data center clusters becomes increasingly important. Networking is no longer just a supporting layer outside the server. It is becoming one of the main bottlenecks of the AI factory.

The larger the model, the more communication matters. The more intensive the communication, the more bandwidth density, latency, power consumption, and signal integrity become system-level constraints.

This is where CPO becomes attractive.

Traditional pluggable optical modules are mature, replaceable, and serviceable. But at higher bandwidth densities, high-speed electrical signals traveling through PCBs, connectors, and copper traces face rising loss, power consumption, and signal-integrity challenges.

CPO tries to move optical engines closer to the switch ASIC. The goal is to shorten the electrical path and bring optics deeper into the system. In theory, this can reduce power consumption, increase bandwidth density, improve signal integrity, and support larger AI clusters.

So the direction of CPO is not the problem.

The problem is that markets often turn “the right long-term direction” into “near-term volume certainty.”

Over the past few months, stocks such as AAOI, LITE, COHR, and SIVE were repriced as if NVIDIA-driven CPO commercialization would quickly translate into volume shipments across optical engines, lasers, silicon photonics, switch chips, pluggable modules, and related materials in 2027–2028.

The SemiAnalysis report challenged that assumption.

It did not kill the CPO thesis. It forced the market to separate the end-state vision from the deployment timeline.

3. The Data Suggests This Was a Timeline Repricing, Not an AI Infrastructure Breakdown

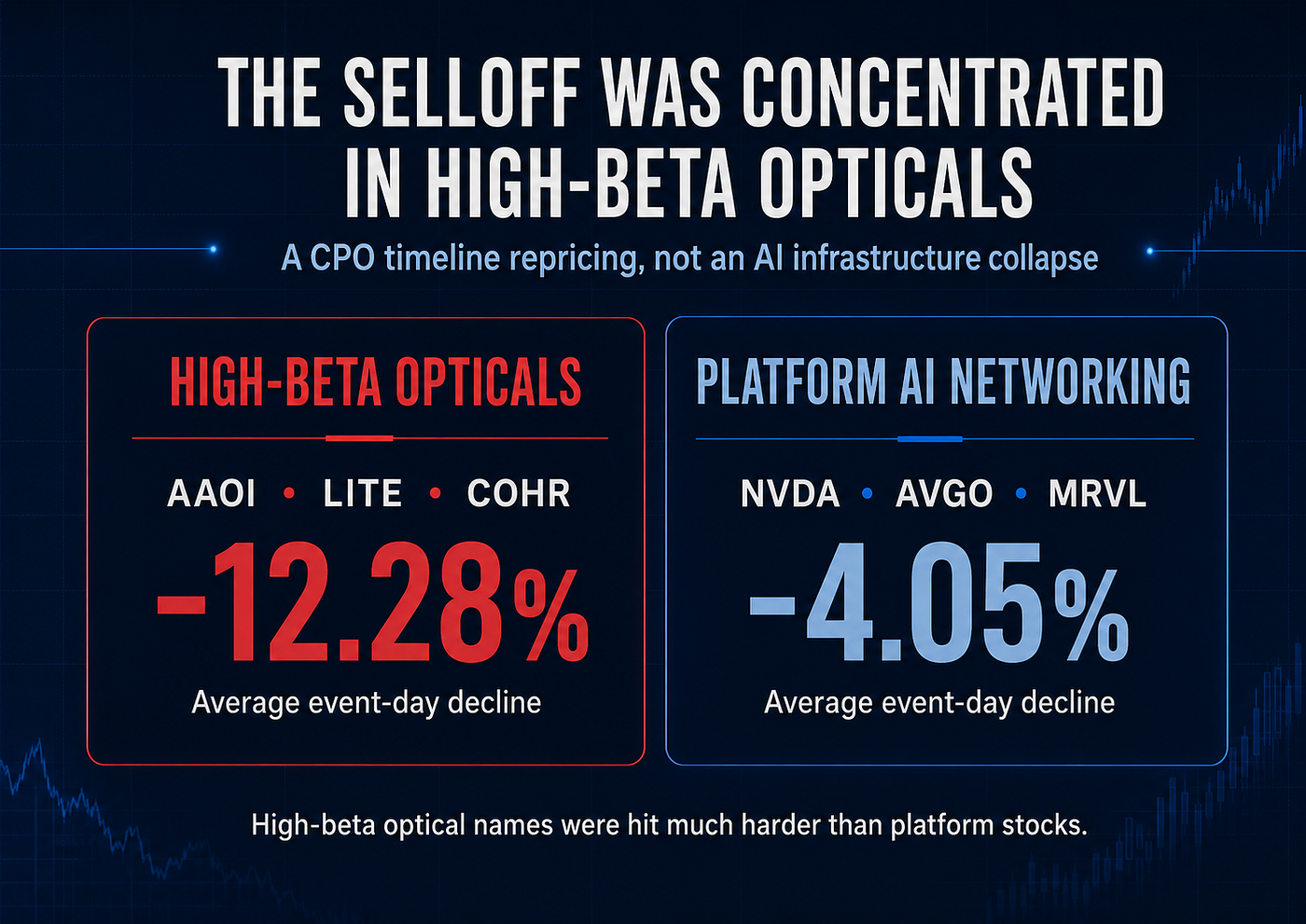

The price action supports this interpretation.

Based on FMP data collected for the event window, the higher-beta optical group — AAOI, LITE, and COHR — fell by roughly 12.28% on average on the event day.

By contrast, the platform-oriented AI networking group — MRVL, AVGO, and NVDA — fell by roughly 4.05% on average.

That gap is important.

If the market were rejecting AI data center capex itself, NVIDIA, Broadcom, and Marvell should have sold off just as aggressively. Instead, the most severe pressure was concentrated in optical names that were most sensitive to CPO timing and had already embedded aggressive expectations.

This suggests the market was not saying:

AI infrastructure demand is gone.

It was saying:

The path from production to volume ramp to revenue recognition may take longer than the stocks had priced in.

Production does not equal mass deployment.

Supplier shipment does not equal customer adoption.

Customer qualification does not equal stable gross margin.

Order visibility does not equal recognized revenue.

That is the core of the recent optical selloff.

4. SemiAnalysis’ Core Point: CPO Is a System Engineering Problem

The difficulty of CPO is not proving that it can work in a lab.

The difficulty is proving that it can be deployed at hyperscale in a way that is reliable, serviceable, manufacturable, and economically attractive.

Traditional pluggable optics have one major advantage: modularity.

If a module fails, it can be replaced. Suppliers can be switched. Inventory can be managed. Customers can test components independently. Pluggable optics may not be the most power-efficient end-state architecture, but they fit the operational needs of large cloud data centers.

CPO changes that equation.

The optical engine moves closer to the ASIC, and in some architectures becomes more deeply integrated into the system. The gains in power and density come from that proximity. But the cost is higher complexity in manufacturing, testing, thermal design, repair, and supply-chain management.

If an optical component fails in a CPO system, the problem may no longer be limited to a replaceable module. It could affect a much more valuable switch ASIC or system-level assembly.

That is the heart of the conservative view.

SemiAnalysis is not saying CPO will not happen.

It is saying that broad deployment requires system-level validation across reliability, yield, field serviceability, and customer operations.

That is why NPO, pluggable optics, DSPs, AEC/ACC, copper interconnects, and power infrastructure suddenly matter more.

They are not the opposite of CPO.

They are the practical tools AI factories still need before CPO is fully mature.

5. Why Serenity’s Pushback Also Makes Sense

Serenity’s strongest point is that NVIDIA is not a normal customer.

NVIDIA defines not only GPU architecture, but also networking architecture, switches, systems, and supplier roadmaps. From Mellanox to Spectrum-X, from NVLink to the AI factory, NVIDIA is no longer just a GPU vendor. It is increasingly defining the full AI infrastructure stack.

If AI factories are constrained by networking bandwidth and power, NVIDIA has a strong reason to accelerate CPO and silicon photonics.

That is why Lumentum’s CPO orders, NVIDIA’s photonics roadmap, GlobalFoundries’ silicon photonics collaboration with Sivers, and Jabil’s 1.6T pluggable work are meaningful signals for bullish researchers.

They suggest that the supply chain is moving.

That should not be ignored.

But supply-chain movement is not the same as full financial realization.

CPO can be the right direction, and supplier activity can be real, while the stocks may still be pricing in revenue too early.

So Serenity’s value is that she reminds investors not to underestimate NVIDIA’s ability to force new hardware cycles forward.

SemiAnalysis’ value is that it reminds investors not to equate production, partner shipment, and customer qualification with mass deployment and revenue recognition.

Those two ideas can both be true.

6. The Real New Hotspot: The Transition Layer

After this debate, investors should not only ask:

Will CPO win?

A better question is:

What must AI factories keep buying before CPO is fully mature?

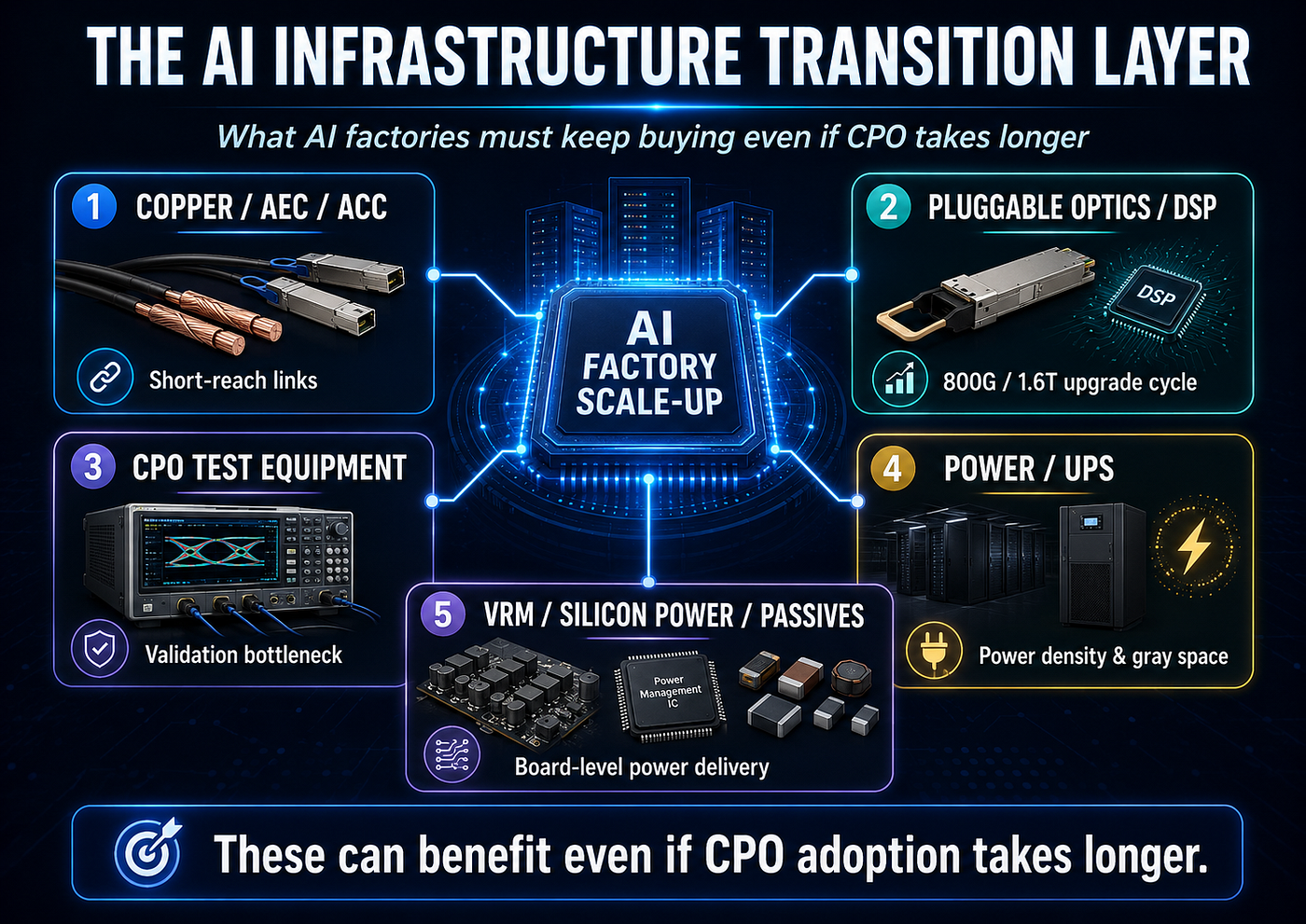

That is where the five “transition-layer” themes become important.

1. Copper / AEC / ACC

Not every connection inside an AI rack will immediately move to optics.

For short-reach, rack-scale, and some scale-up connections, copper, active electrical cables, and active copper cables still have practical value. They solve problems around signal integrity, cost, and deployment simplicity over shorter distances.

If CPO adoption takes longer, the life cycle of copper and active cable solutions could be extended.

This is not the most exciting end-state narrative, but it may be a more immediate revenue opportunity.

2. Pluggable Optics / DSP

Pluggable optics and DSPs are among the clearest beneficiaries of a longer CPO transition period.

If CPO does not broadly ramp in 2027–2028, then 800G and 1.6T pluggable optical modules will continue to carry much of the AI data center networking upgrade cycle.

DSPs will also remain important. They help manage signal integrity, modulation, power, and link quality in high-speed optical modules.

So the industry should not be framed as “CPO wins, pluggables lose.”

The more realistic outcome is that CPO, NPO, pluggable optics, and copper interconnects coexist across different layers of the network.

3. CPO Test Equipment

The more complex CPO becomes, the more important testing becomes.

Optical engines, lasers, silicon photonics, electrical chips, packaging, thermal management, burn-in, and system-level reliability all need to be validated.

The more integrated the system, the more expensive it becomes to discover problems late in the process.

This makes CPO test equipment an interesting “picks and shovels” theme.

If CPO ramps quickly, testing benefits.

If CPO ramps slowly, the qualification period lengthens, and testing can still benefit.

This theme is less dependent on one specific architecture winning and more dependent on the rising complexity of silicon photonics and optical packaging.

4. Power Gray Space / UPS

AI data centers are not only constrained by networking. They are constrained by power.

More GPUs mean higher rack power density. Higher rack power density means more pressure on UPS systems, power distribution, thermal management, gray-space upgrades, and energy efficiency.

This is a more fundamental bottleneck than CPO.

Whether the industry uses CPO, NPO, pluggable optics, or copper, AI factories still need more power infrastructure.

That is why companies involved in UPS, electrical distribution, data center power equipment, and thermal infrastructure deserve a place in the AI investment framework. Investors should not only look at GPUs and optical modules.

5. Board-Level VRM / Silicon Power / Passives

As AI servers move from standalone systems to rack-scale architectures, power pressure flows down to the board level.

VRMs, power management ICs, MLCCs, inductors, capacitors, SiC/GaN devices, and MOSFETs may not be glamorous, but they are indispensable.

Many of the best AI infrastructure opportunities are not in the hottest buzzwords. They are in the components that cannot be removed, cannot fail, and gain value as every new generation of AI hardware consumes more power.

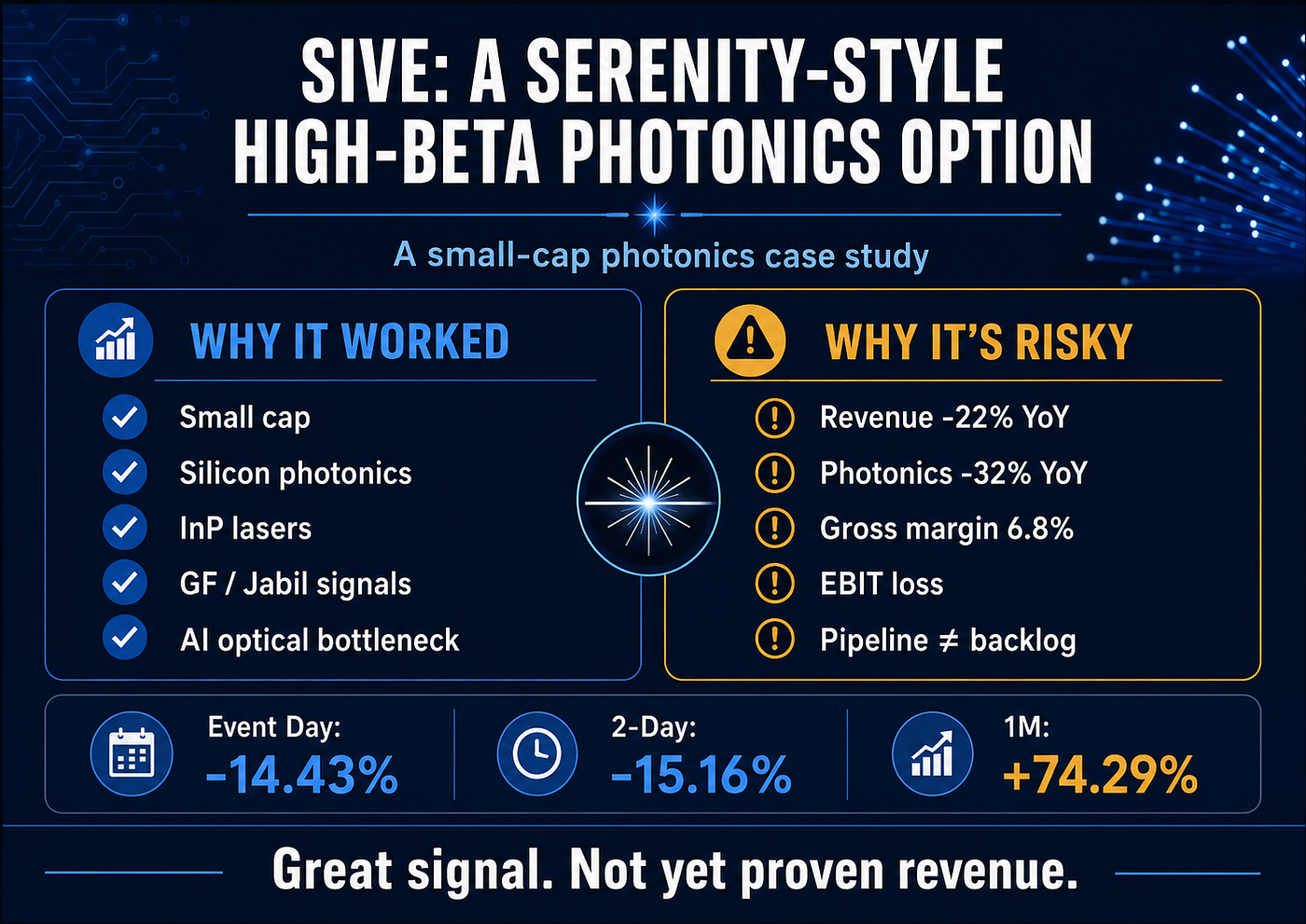

7. SIVE: A Classic Serenity-Style High-Beta Case Study

SIVE deserves a separate discussion.

It should not be included in the same U.S. event-window average as AAOI, LITE, and COHR, because its primary listing is in Stockholm, its trading currency is SEK, and its liquidity and data sources are different. SIVEF is only a U.S. OTC reference and should not be mixed with SIVE.ST.

But SIVE is a very useful case study for understanding Serenity’s method.

According to Yahoo Finance data collected for SIVE.ST, the stock had already been dramatically repriced before the CPO debate:

One-month return: approximately +74.29%. Three-month return: approximately +1,965.63%. Six-month return: approximately +1,930.25%. Year-to-date return: approximately +1,725.95%. One-year return: approximately +1,599.91%.

But after the CPO timeline debate emerged, SIVE.ST fell roughly 14.43% on the event day and roughly 15.16% over two days.

This tells us something important.

Serenity’s method can identify extremely high-beta small-cap photonics names. But these stocks can move far ahead of current revenue. When the timeline is challenged, the volatility can be severe.

From a technology perspective, SIVE is not just a random CPO story.

Sivers’ collaboration with GlobalFoundries explicitly involves silicon photonics reference designs, including CPO, LPO, and the GF SCALE optical engine architecture. Sivers’ laser arrays support these silicon photonics designs, which places the company in the AI data center optical interconnect, silicon photonics, InP laser, and optical engine ecosystem.

Sivers’ work with Jabil on 1.6T pluggable optical transceivers is also important. It shows that SIVE’s opportunity is not limited to the CPO end-state. It may also participate in the transition layer through 1.6T pluggables, silicon photonics, laser arrays, and optical I/O.

But the financial risk is just as clear.

In Q1 2026, Sivers reported group net sales of SEK 61.9 million, down 22% year over year. Photonics sales fell 32% year over year. Gross margin was only 6.8%, and EBIT was a loss of SEK 41.5 million.

That means the stock’s move was not driven by current revenue acceleration. It was driven by a repricing of future AI optical connectivity optionality.

This is the double-edged nature of Serenity’s approach.

The strength of the method is that it can identify small-cap companies sitting near important technical bottlenecks before they are widely covered by mainstream institutions.

The risk is that the stock price can run far ahead of revenue conversion.

Sivers disclosed a roughly $799 million opportunity pipeline, but that is not backlog. ALL.SPACE’s $8.2 million production order shows that Sivers can move into commercial production, but that order relates to SATCOM and defense, not AI data center CPO. The market speculation linking Sivers to POET or Celestial AI has not been confirmed by Sivers officially, so it should be treated as low-confidence supply-chain inference.

Therefore, the most accurate way to describe SIVE is not:

a proven CPO revenue stock.

It is:

a Serenity-style early photonics option.

It shows why Serenity’s research process can be valuable: she looks for small companies connected to major technical bottlenecks before the market fully prices them.

But it also shows the risk: the earlier the company, the smaller the market cap, and the more dependent the thesis is on future deployment timing, the more violently the stock can react when that timing is questioned.

8. How to Reclassify the Stocks

After this debate, it is too simplistic to call everything a “CPO beneficiary.”

A better framework is to divide the chain into four groups.

1. CPO End-State Options

These companies are most directly exposed to CPO, silicon photonics, optical engines, lasers, optical packaging, and AI optical interconnects.

Examples include LITE, COHR, AAOI, SIVE, and other silicon photonics or laser-related names.

They have high upside, but they are extremely sensitive to timeline risk.

2. Transition-Layer Cash Flow

These companies benefit from the upgrade cycle before CPO is fully mature. This includes pluggable optics, DSPs, 1.6T modules, AEC, ACC, NPO, and related connectivity solutions.

Examples include MRVL, AVGO, COHR, LITE, and parts of the high-speed interconnect chain.

The end-state narrative may be less explosive, but the medium-term revenue path could be more visible.

3. Power Infrastructure Certainty

These companies do not need to bet on how fast CPO ramps. They benefit from rising AI data center power density.

This includes UPS, power distribution, gray-space upgrades, liquid cooling, power management, VRMs, silicon power, and passive components.

The narrative is less glamorous than CPO, but the demand may be more certain.

4. AI Networking Platforms

NVDA, AVGO, and MRVL are closer to the platform layer. They are not only exposed to one component. They sit across AI networking, switch silicon, custom silicon, system architecture, and ecosystem control.

Their volatility may be lower than small-cap photonics names, but they may also have less explosive upside.

9. Final View: CPO Is the End-State Option, the Transition Layer Is the Medium-Term Cash Flow

I do not think this selloff means the CPO thesis is dead.

In fact, the long-term direction is becoming clearer. As AI factories scale, networking power, bandwidth density, and signal integrity will only become more important. Optical interconnects are not optional. They are a likely requirement for continued AI infrastructure scaling.

But I also do not think investors should treat NVIDIA’s production language, Lumentum’s CPO orders, or Sivers’ silicon photonics partnerships as proof of risk-free mass revenue in 2027–2028.

The market is repricing the slope.

CPO is coming. The question is how steep the adoption curve will be.

If CPO ramps quickly, optical engines, lasers, silicon photonics, CPO test equipment, and switch-chip ecosystems should benefit the most.

If CPO ramps more slowly, then NPO, pluggable optics, DSPs, AEC/ACC, power infrastructure, and board-level power components may have a longer window.

If investors continue to chase Serenity-style small-cap photonics names, stocks like SIVE may still offer extreme upside. But they will also remain highly vulnerable to any change in the timeline narrative.

So the right question is not:

Who is right, SemiAnalysis or Serenity?

The better question is:

Before CPO is fully mature, what must AI factories keep buying anyway?

The answer is probably not one stock or one technology. It is a full transition infrastructure stack:

Copper / AEC / ACC. Pluggable optics / DSP. NPO. CPO test equipment. Power gray space / UPS. VRM / silicon power / passive components.

CPO is the end-state option.

The transition layer is the medium-term cash flow.

Small-cap photonics names like SIVE are timeline options.

The real new hotspot is not that CPO has been rejected.

It is that the market is starting to look for the parts of AI infrastructure that must be purchased even if CPO takes longer than expected.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-10 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments