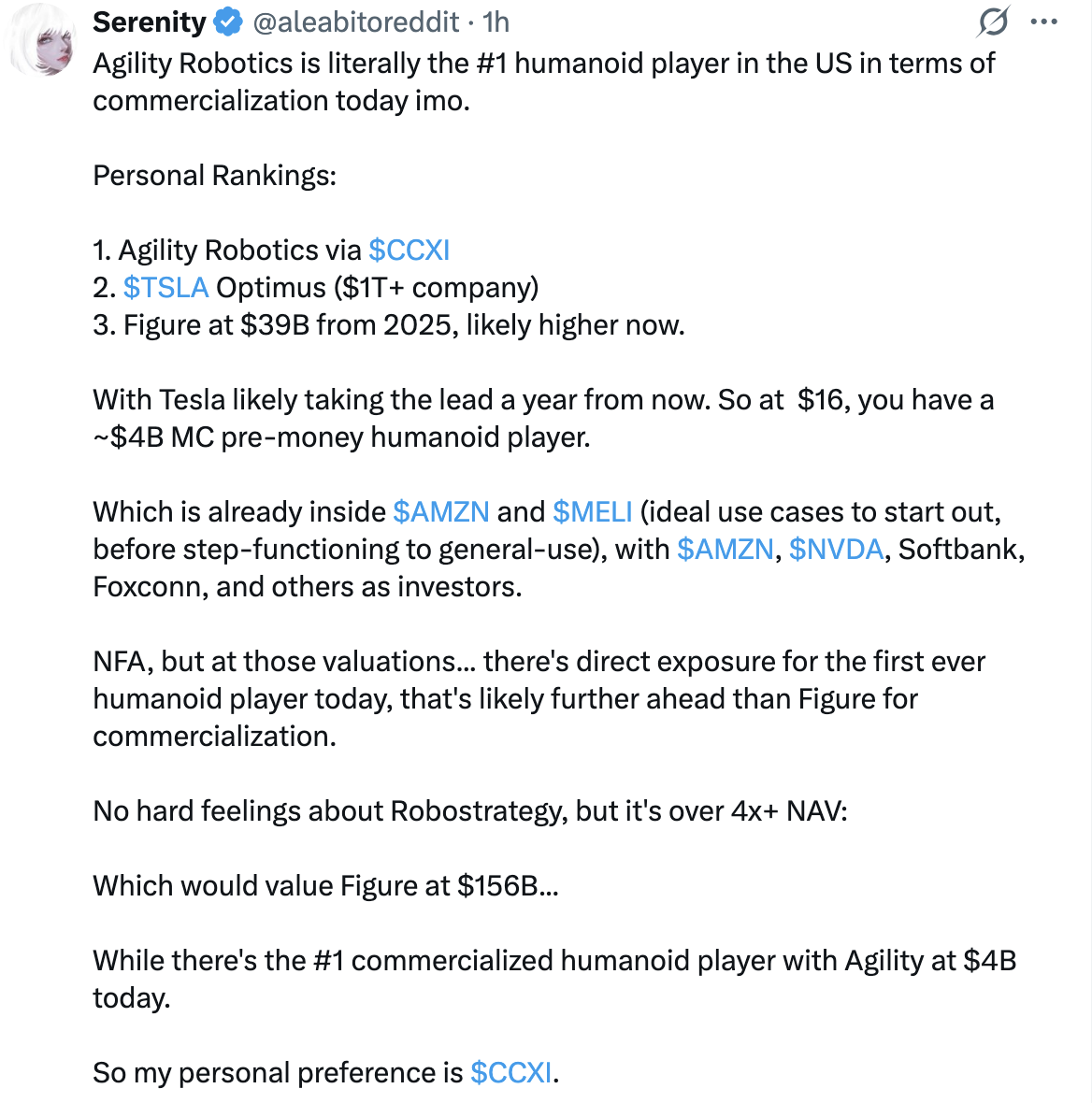

Serenity recently mentioned a stock called CCXI.

If this is the first time you have seen the ticker, the initial reaction is probably confusion. It does not carry an obvious robotics label like Tesla, Nvidia, or Figure. It does not look like a company making motors, sensors, or factory automation systems. At first glance, CCXI looks more like an unfamiliar financial shell.

That is exactly why it has started to attract attention.

The excitement around CCXI is not about the shell company itself. It is about the company it plans to bring to the public market: Agility Robotics. Agility makes humanoid robots, and its core product is called Digit. In simple terms, CCXI is a public-listing vehicle. If the transaction closes, public-market investors may finally have a way to buy exposure to a relatively pure humanoid robotics company, instead of accessing the theme indirectly through Tesla or simply watching private-market headlines about Figure.

That is the real reason Serenity is paying attention.

Humanoid robots have been one of the hottest ideas in AI, but for public-market investors, the theme has remained strangely hard to own. Tesla Optimus is compelling, but it is only one long-term option inside a much larger company. Figure has attracted a very high private-market valuation, but it is not public. Boston Dynamics sits under Hyundai. Many Chinese robotics companies are either not listed in the U.S. or are not pure humanoid plays. CCXI is unusual because it may bring Agility, a company with real commercial deployments, directly in front of U.S. public-market investors.

That is where the story becomes more complicated.

A tradable entry point is not the same thing as a position worth building aggressively. A robotics company can have customers, orders, and deployments without having proved that the business model works. This is where investors can easily make mistakes in humanoid robotics: they confuse technical progress with financial certainty, and they confuse "relatively cheaper" with "truly undervalued."

So the real question is not just whether CCXI can rise. The more important question is this: if Physical AI becomes the next major AI investment theme, should investors buy the robot makers themselves, or should they look at the platforms, components, industrial software, and automation infrastructure behind them?

Agility plans to go public through Churchill Capital Corp XI in a transaction that values the company at about $2.5 billion pre-money and is expected to bring in more than $620 million of gross proceeds. The company says Digit has already been deployed with companies including Schaeffler, GXO, Toyota Motor Manufacturing Canada, and Mercado Libre, handling repetitive physical tasks in manufacturing, distribution, and logistics. Agility also says Digit has accumulated more than 65,000 hours of runtime across nine customer facilities. This is not just a polished robot demo video. It is Agility trying to show the market that Digit has started to enter real operating environments.

That is why Agility deserves more attention than many humanoid robotics projects. Over the past few years, too many robotics stories have been driven by videos. A robot walks, picks something up, waves at the camera, and investors immediately imagine a future labor-replacement market. But commercialization is not measured by a launch event. It is measured by whether customers keep deploying the product. Agility has at least moved beyond the stage of zero customers and zero field operations. Toyota Motor Manufacturing Canada signed a Robots-as-a-Service agreement with Agility after a successful pilot, and Mercado Libre has announced plans to deploy Digit in Texas fulfillment centers.

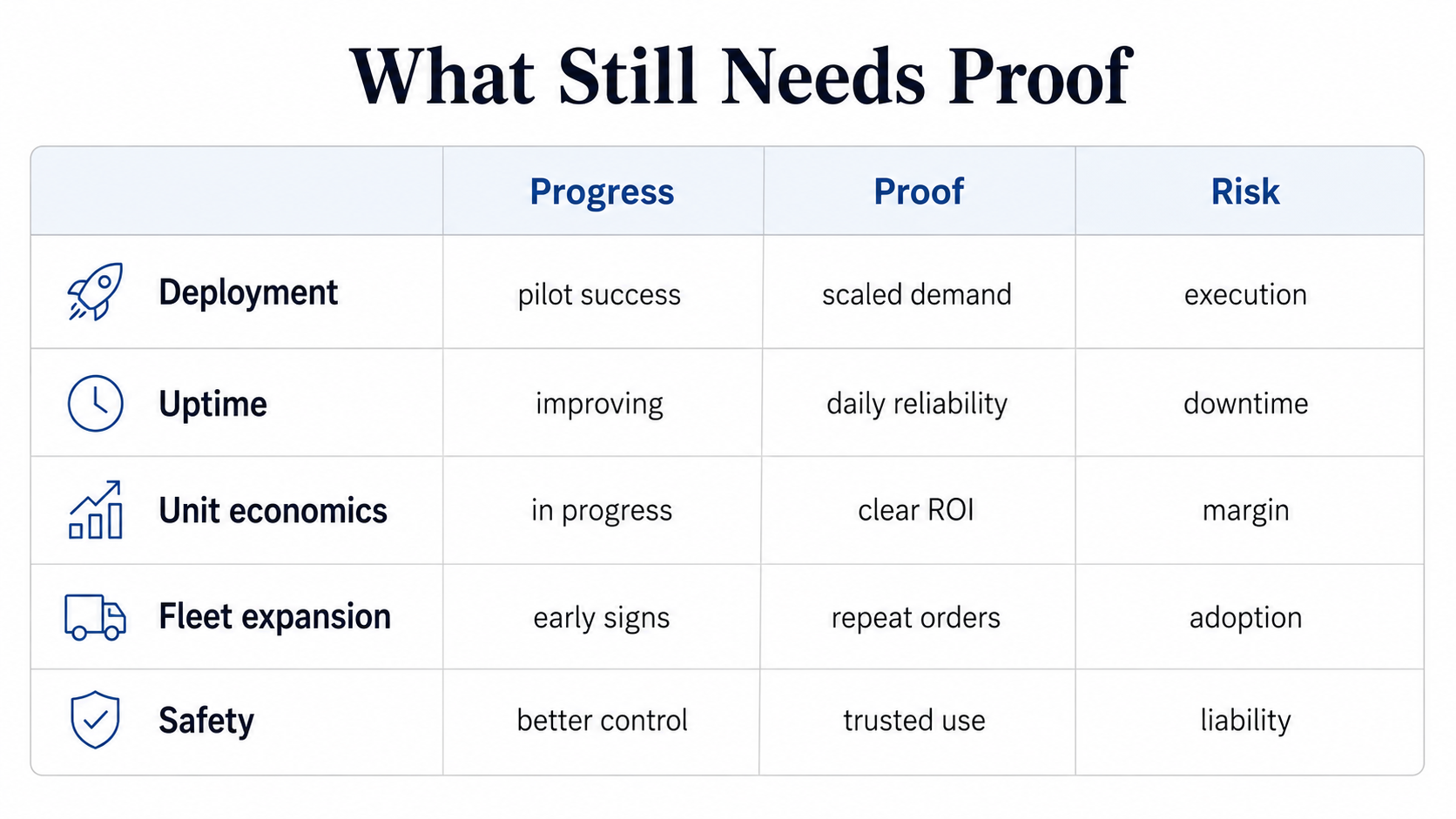

But this is still the beginning, not the proof.

Orders and deployments do not automatically translate into high-quality revenue. The most important financial question for a robotics company is not whether customers are willing to test the robot. It is whether customers expand deployment. It is not whether the robot can complete a task once. It is whether it can work reliably every day. It is not whether the order number sounds large. It is whether that order becomes revenue, gross margin, and eventually cash flow.

This is the missing piece in Serenity's logic. Her view is valuable because she spotted Agility's scarcity value. Among humanoid robotics assets available to public-market investors, Agility may be one of the few relatively pure names with real commercial deployments. Compared with Figure's high private-market valuation, Agility's implied valuation through CCXI looks less extreme. That "relative value" argument is worth discussing.

But relative cheapness is only a comparison. It is not a margin of safety.

If the benchmark itself is expensive, another asset can look cheaper simply because it is less expensive, not because it is genuinely cheap. What will determine whether Agility is investable is not how much cheaper it looks than Figure. It is whether the unit economics of Digit can be proven: production cost, maintenance cost, labor savings per hour, failure rate, insurance and safety liability, and customer payback period. Is the payback two years, three years, or still impossible to calculate?

This is the part of humanoid robotics investing that is easiest to overlook. The market loves to talk about "mass production," but mass production is not the same as making a robot that works.

If mass production means dozens or hundreds of units, the industry is already moving in that direction. Agility, Tesla, Figure, Unitree, and 1X can all show real hardware, and all can make robots complete certain tasks in controlled environments. But if mass production means tens of thousands or hundreds of thousands of units per year, with falling costs, reliable operation, customer expansion, and a manageable service system, the industry has not proved that yet.

This is also why Tesla Optimus recently drew so much attention again. Elon Musk's photo with the Optimus production team at the Fremont factory was interpreted by the market as a sign that Tesla is pushing Optimus from a research project into production engineering. Musk has also said that early production of Cybercab and Optimus will be "agonizingly slow," because these products include many new parts and new processes, with Optimus production targeted for later in 2026.

That statement is more realistic than many promotional claims in robotics. Tesla may be one of the companies best positioned to engineer humanoid robot production at scale because it has manufacturing experience, supply-chain capability, vertical integration, and its own factories for internal testing. For most robotics startups, the hardest gap to close is not making an impressive video. It is building the manufacturing system, quality control process, supply chain, and service network.

Yet even Tesla admits the ramp will not be fast. The reason is simple: a robot is not just a car in a different shape. A car mainly operates on roads. A humanoid robot must move through three-dimensional spaces, walk, turn, grasp, carry, avoid obstacles, understand objects, and collaborate around people. The failure modes are broader, the safety risks are higher, and the task boundaries are less defined.

That is why the question "why does it need to be humanoid?" matters.

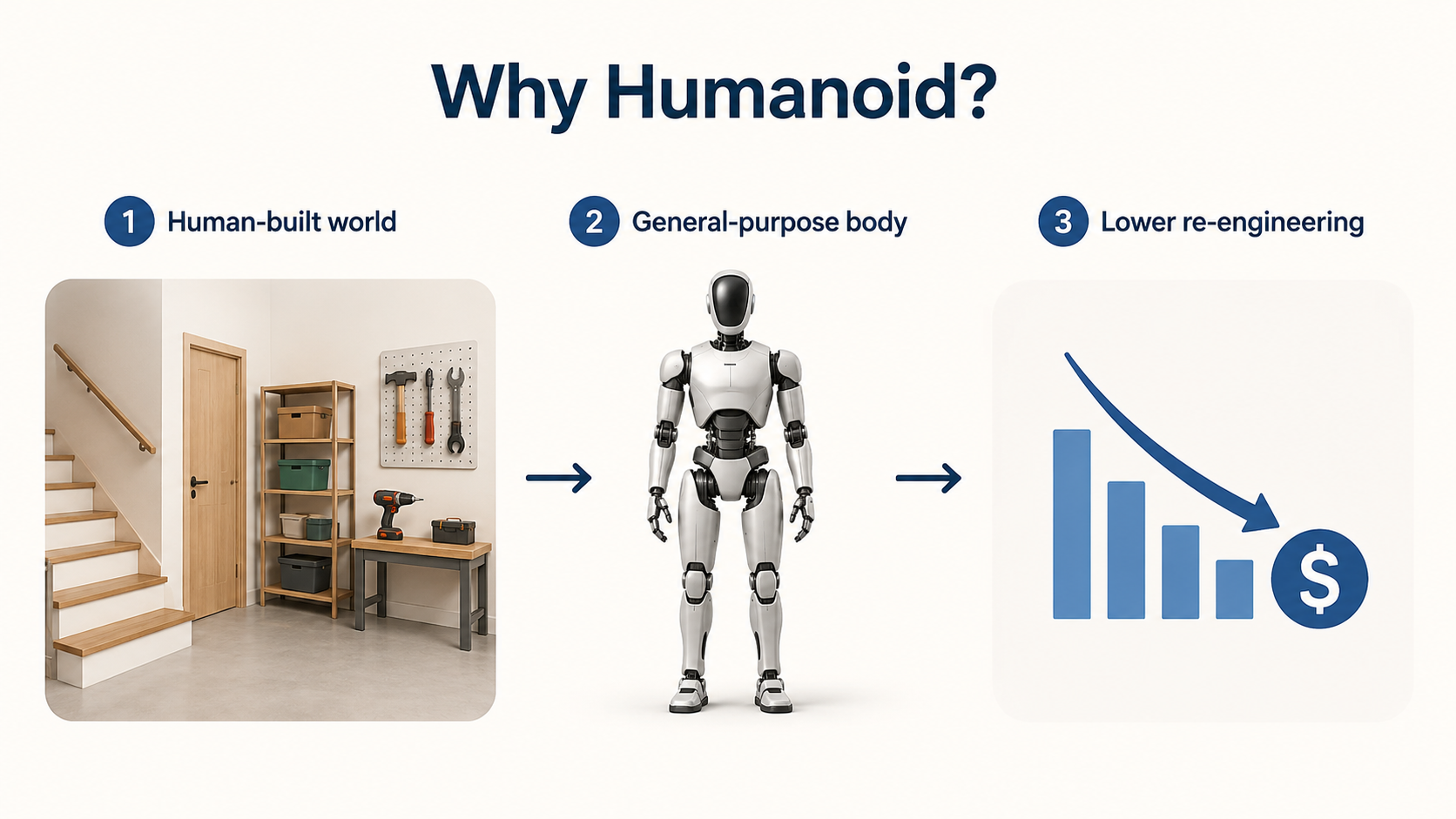

Companies do not buy a robot simply because it looks like a person. If a task can be solved by a conveyor belt, a fixed robotic arm, an AMR cart, or an automated sorting system, dedicated equipment is usually cheaper, more reliable, and easier to maintain. The value of a humanoid robot is not its appearance. The value is that the human world was built around the human body.

Doors, stairs, shelves, carts, tools, switches, workbenches, warehouse aisles, and factory workflows all assume an operator with two legs, two arms, and a torso. If a customer does not want to rebuild the entire environment, but wants a robot to enter an existing human-designed workflow, a humanoid form starts to make commercial sense.

So the first-principles case for humanoid robots is not that they are "human-like." It is this: a general-purpose body can enter environments already designed for people and perform repetitive, low-frequency, dangerous, or hard-to-staff tasks.

This also explains why the first real use cases are unlikely to be household butlers. They are more likely to be warehouses, logistics facilities, and factories. Homes are too open-ended, too cluttered, too variable, and too unforgiving. Moving boxes in a warehouse, feeding materials into a production line, sorting goods in a logistics center, or carrying items within a fixed operating zone is far less glamorous, but much easier to control and much easier to justify with a return-on-investment calculation.

This is also where Physical AI differs from internet AI. Internet AI makes mistakes on a screen. Physical AI makes mistakes in the real world. A language model can answer incorrectly and try again. A robot that grabs the wrong object, collides with equipment, falls over, or damages goods can injure people, destroy inventory, or stop a production line. The hard part is not getting the robot to do something once. The hard part is getting it to do useful work every day, avoid serious mistakes, and recover quickly when something goes wrong.

Nvidia's push into robotics infrastructure comes from this bottleneck. Nvidia's GR00T N1 paper describes a generalist humanoid robot as a system that needs both a versatile body and an intelligent brain. Training requires a mix of real robot trajectories, human videos, and synthetic data, while vision-language-action models connect environmental understanding to real-time action generation.

This suggests robotics is entering a platform-building phase similar to the early development of large language models. Data pipelines, simulation systems, foundation models, edge computing, and developer toolchains are becoming central. Research around Nvidia Isaac Sim also highlights simulation as a core piece of robotics infrastructure because GPU-accelerated simulation and synthetic data generation can help address the shortage of real robot training data.

But stronger infrastructure does not mean commercial robotics will mature overnight. The physical world cannot be bypassed entirely with better models. Robots are still constrained by data, generalization, dexterous manipulation, actuators, batteries, heat, weight, reliability, safety certification, maintenance systems, and cost curves.

That is why the view that "robots may still need another decade to mature" is not outdated. It does not mean there will be no investment opportunities in the next ten years. It means the path from small-scale deployment to general labor substitution is still long. Semi-structured industrial settings will come first. Homes and more complex open environments will take longer.

For investors, the most important conclusion is not that robotics is uninvestable. It is that buying the most visible robot maker may not be the best risk-adjusted way to invest in Physical AI.

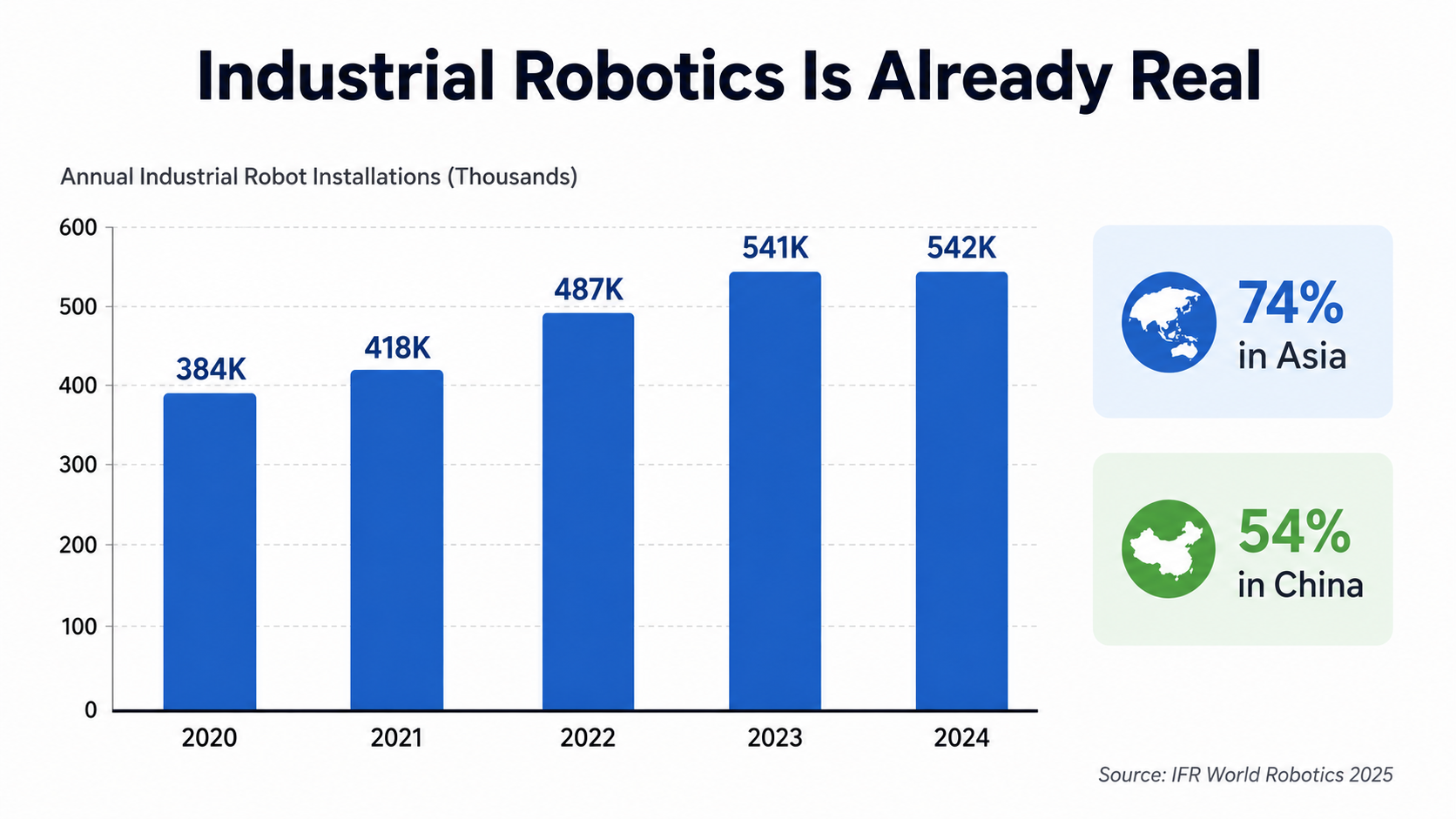

Industrial robotics is already a real industry. The International Federation of Robotics reported that global factories installed about 542,000 industrial robots in 2024, marking the fourth consecutive year above 500,000 units. Asia accounted for 74% of new installations, and China alone represented 54% of global installations. That shows real-world automation is already happening. Humanoid robots have simply pushed the broader idea of general-purpose robotic labor into the foreground.

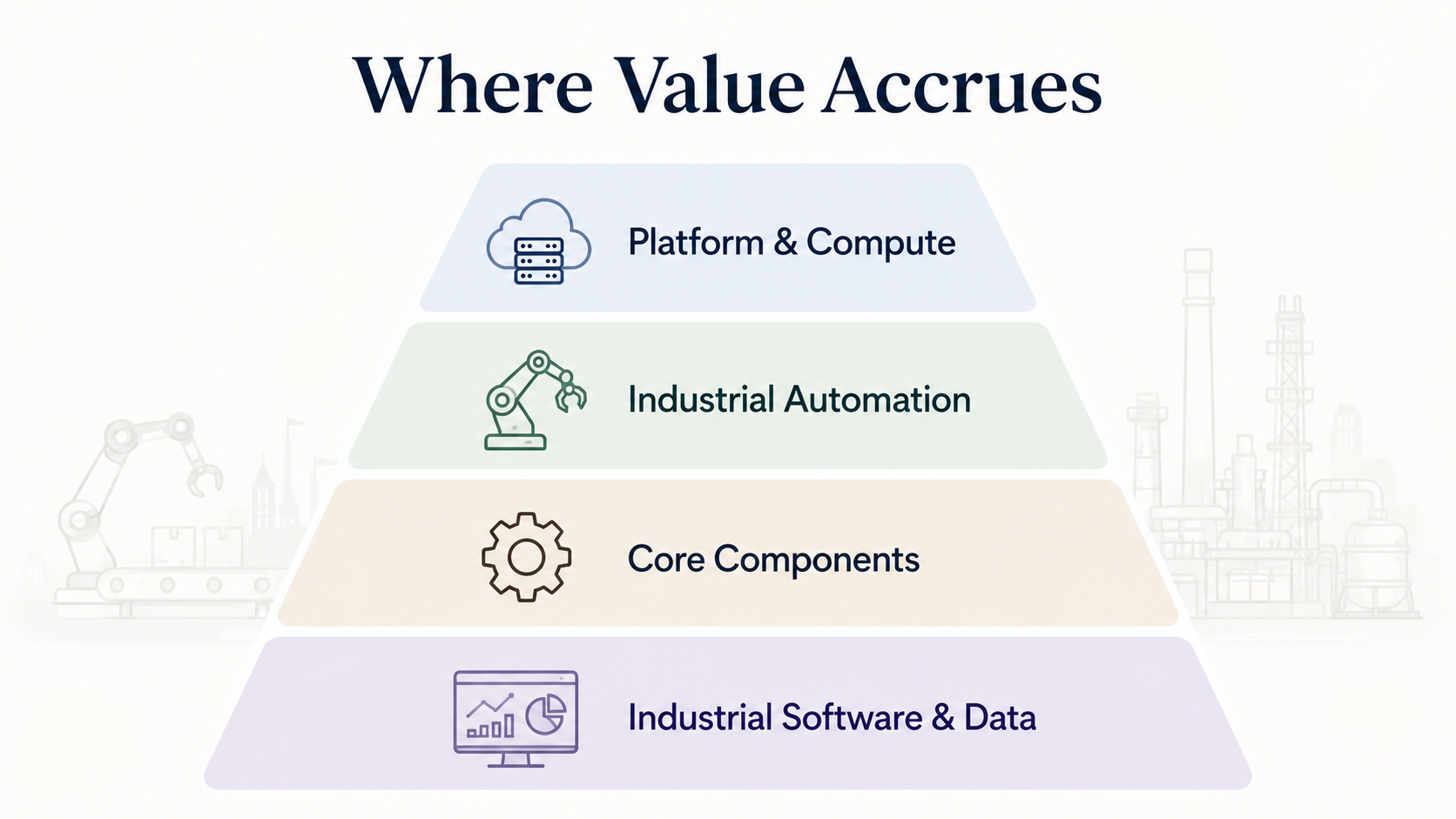

If Physical AI becomes the next major AI theme, the value will not necessarily stay with the robot makers. The more durable investment opportunities may sit in several layers.

The first layer is platforms and compute. Nvidia does not need to know whether Agility, Figure, Tesla, or Unitree wins. As long as robotics, autonomous driving, factory edge AI, and simulation training keep expanding, platforms such as GPUs, Jetson, Isaac, Omniverse, and GR00T can become infrastructure. This is the same control-point logic behind AI infrastructure and AI CapEx: the platform can matter more than the most visible application. The issue with Nvidia is not the direction of travel. The issue is valuation, because humanoid robotics alone is not enough to justify a near-term investment case.

The second layer is mature industrial automation. Industrial robots, PLCs, servo systems, machine vision, and warehouse automation companies may not carry the same narrative excitement as humanoid robots, but they have real customers, installed bases, service revenue, and cash flow. Physical AI is unlikely to replace these systems from scratch. It is more likely to integrate with the automation stack already inside factories and warehouses, much like AI systems depend on less glamorous bottlenecks such as data movement.

The third layer is core components. If humanoid robots scale, value will not sit only in the final robot. Joint modules, actuators, motors, reducers, torque sensors, encoders, bearings, batteries, wiring harnesses, controllers, and edge-computing modules will all become important cost items. This layer looks more like a "picks and shovels" opportunity, but it is also where concept inflation can be dangerous. Not every supplier with a robotics label will benefit. The key question is whether the company is actually entering major customer supply chains or already has a real position in traditional robotics and precision manufacturing.

The fourth layer is industrial software and data infrastructure. This is where a company like PTC fits into the broader Physical AI framework. PTC is not a humanoid robotics company. It sells CAD, PLM, ALM, and SLM software, helping manufacturers manage product data, engineering workflows, and lifecycle processes. When robots enter manufacturing, they are not just walking hardware. They need to understand products, processes, quality records, service histories, and engineering changes. If the underlying industrial data is not structured, robots and AI agents will struggle to operate inside complex manufacturing workflows.

That makes companies like PTC less exciting but potentially more durable. They do not offer the same upside beta as CCXI, but they look more like data infrastructure for industrial digitization and Physical AI. PTC is a slow-compounding asset. CCXI is a high-beta thematic trade.

That distinction matters.

CCXI's strength is scarcity. There are very few pure humanoid robotics names available in the public market, and Agility appears closer to commercial deployment than many robotics companies. Digit is already in real customer environments, which makes CCXI an important window into how the market prices humanoid robotics commercialization.

Its weakness is equally clear. The transaction has not closed. The SPAC structure creates uncertainty. If the stock trades meaningfully above $10, the cash-shell safety anchor becomes much weaker. Orders must become revenue. Revenue must become gross margin. Gross margin must survive maintenance costs, failure rates, safety issues, and service expenses. Most importantly, the biggest debate in robotics is not whether there is demand. It is when the unit economics will actually work.

So CCXI is not a stock that can be easily labeled as a buy or a pass. It is better understood as a public-market signal: the market is beginning to put a price on humanoid robotics commercialization.

For investors who want steadier exposure to Physical AI, the core position should probably not be a humanoid robotics SPAC. It should be built around platform companies, industrial automation, industrial software, and critical components. CCXI can be used as a small, volatile, event-driven position to capture the possibility that humanoid robotics moves from private-market excitement into public-market repricing.

That is the real value in Serenity's focus on CCXI. She is pointing to a shift: humanoid robotics is no longer only a Tesla presentation or a Figure funding headline. It is becoming something the public market can price, trade, and potentially misprice.

The bigger question is not whether CCXI rallies in the short term. It is whether capital markets begin to reprice the entire Physical AI supply chain.

Robot makers will get the most attention. Platform companies may collect the most economic rent. Component suppliers may benefit most directly from volume. Industrial automation companies have the cash flows. Industrial software companies provide the data backbone. CCXI is an important entry point, but it is not the whole answer.

If humanoid robots truly move toward mass production, the winners will not be limited to one robot brand. Value will be redistributed across compute, simulation, actuators, sensors, industrial automation, data systems, and safety standards. CCXI may simply be the first signal light flashing in the public market.

Related Reading

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

NVIDIA’s Next Bottleneck Isn’t GPUs. It’s Data Movement.

Why AI factories are moving from copper to optical connectivity — and which suppliers deserve deeper research

How to Read the AI Cycle: CapEx, Supply Bottlenecks, and the Semiconductor Trade

AI infrastructure spending is still expanding, but the semiconductor equity trade is becoming more fragile. The next phase depends on CapEx, supply bottlenecks, usage, pricing, and earnings revisions.

If You Missed Nvidia’s 10x Run, Where Is AI’s Next Stop?

The Lesson From GTC Taipei: When Computing Starts Serving Agents, the Next Decade of Wealth Redistribution Begins

Sources & Notes

Sources for this article are listed below. Transaction, customer, runtime, and robotics-market details should be treated as company-reported or source-reported unless separately disclosed in audited filings.

| Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|

| Agility Robotics — Agility to go public through merger with Churchill Capital Corp XI | Agility Robotics | 2026 | Company announcement | Transaction value, expected proceeds, Digit deployments, customer sites, runtime, and commercial positioning. |

| Agility Robotics — Toyota Motor Manufacturing Canada agreement | Agility Robotics | 2026 | Company announcement | Toyota deployment and Robots-as-a-Service agreement. |

| Agility Robotics — Mercado Libre commercial agreement | Agility Robotics | 2026 | Company announcement | Mercado Libre fulfillment center deployment. |

| Elon Musk says production for Cybercab robotaxi and Optimus robot will initially be 'agonizingly slow' | Business Insider | 2026 | Market reporting | Tesla Optimus production timing and the initial production-ramp comment. |

| GR00T N1: An Open Foundation Model for Generalist Humanoid Robots | arXiv / NVIDIA authors | 2025 | Research paper | Robotics foundation model, real robot trajectories, human videos, synthetic data, and VLA framework. |

| NVIDIA Isaac Sim: Enabling Scalable, GPU-Accelerated Simulation for Robotics | arXiv | 2026 | Research paper | Robotics simulation, GPU acceleration, and synthetic data generation. |

| World Robotics 2025 | International Federation of Robotics | 2025 | Industry report | 2024 industrial robot installation data, Asia share, and China share. |

FAQ

Is CCXI a pure humanoid robotics company today?

No. CCXI is the SPAC vehicle tied to the proposed Agility Robotics transaction. If the deal closes, public investors may gain exposure to Agility through the combined company.

Why is Agility Robotics important for public-market investors?

Agility may become one of the rare U.S.-listed ways to invest directly in commercial-stage humanoid robotics instead of accessing the theme indirectly through larger companies such as Tesla or Nvidia.

What still needs to be proven?

The key proof points are repeat customer expansion, daily reliability, service cost, safety performance, gross margin, and whether Robots-as-a-Service economics produce attractive cash flow.

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. The author may discuss securities, companies, or themes that are volatile, speculative, or event-driven.

Comments