Search for “Agility Robotics stock,” and one ticker now appears repeatedly: $CCXI.

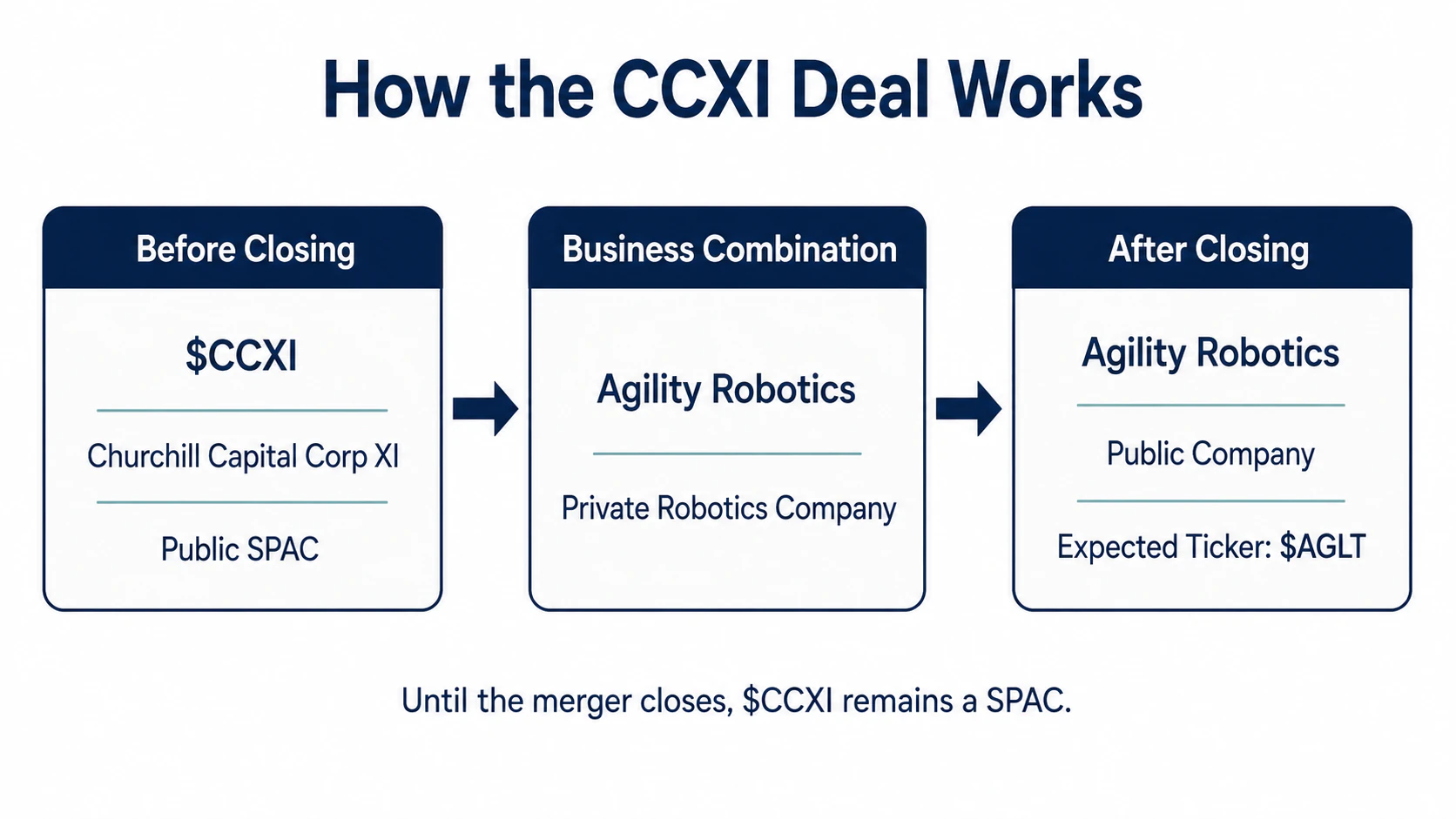

That can create the impression that Agility Robotics is already a publicly traded company. It is not. $CCXI currently represents Churchill Capital Corp XI, a special purpose acquisition company, or SPAC. Churchill XI has signed a definitive agreement to combine with Agility Robotics, but the transaction still has to complete before public shareholders directly own shares in the combined operating company.

If the deal closes as planned, Churchill XI will be renamed Agility Robotics, and the combined company is expected to trade under the ticker $AGLT. Until then, investors buying $CCXI are buying the public acquisition vehicle attached to the proposed transaction.

That distinction matters because a SPAC stock carries two separate risks. The first is whether the merger closes. The second is whether the operating company will eventually justify the valuation embedded in the share price.

Understanding $CCXI therefore begins with understanding the structure of the deal.

What is Churchill Capital Corp XI?

Churchill Capital Corp XI was formed as a blank-check company. A blank-check company raises money from public investors before it has an operating business. The cash is placed in a trust account while the SPAC’s sponsor searches for a private company to acquire.

Churchill XI completed that search when it announced its agreement with Agility Robotics on June 24, 2026.

Agility is the company behind Digit, a bipedal humanoid robot designed for manufacturing, logistics and distribution environments. The company says Digit is already operating with customers including Schaeffler, GXO, Toyota Motor Manufacturing Canada and Mercado Libre. Agility also operates Arc, a cloud platform designed to integrate robots into customer workflows and manage deployed fleets.

Churchill XI itself does not design robots, sell automation software or generate operating revenue from Digit. Its role is to provide Agility with a route into the public market and a pool of capital that can be used to finance commercialization.

Is this an Agility Robotics IPO?

Investors often describe the transaction as the “Agility Robotics IPO,” but it is more accurately described as a de-SPAC transaction.

In a traditional IPO, a private company sells newly issued shares to public investors through an underwritten offering. In a de-SPAC transaction, the private company combines with a SPAC that is already publicly listed.

The result can look similar. Agility becomes public, gains access to new capital and receives a tradable stock ticker. The path is different because Churchill XI already has public shareholders, cash in trust, founder shares and outstanding warrants before the operating company arrives.

Under the merger agreement, Churchill XI will first domesticate from the Cayman Islands into Delaware. Its merger subsidiary will then merge into Agility, with Agility surviving as a wholly owned subsidiary of the public company. Churchill XI will be renamed Agility Robotics, and existing Churchill Class A shares are expected to convert one-for-one into common shares of the combined company.

In practical terms:

$CCXI before closing → Agility Robotics after closing → expected ticker $AGLT

The ticker change only occurs after the required filings, approvals and closing conditions have been completed.

What does the $2.5 billion valuation mean?

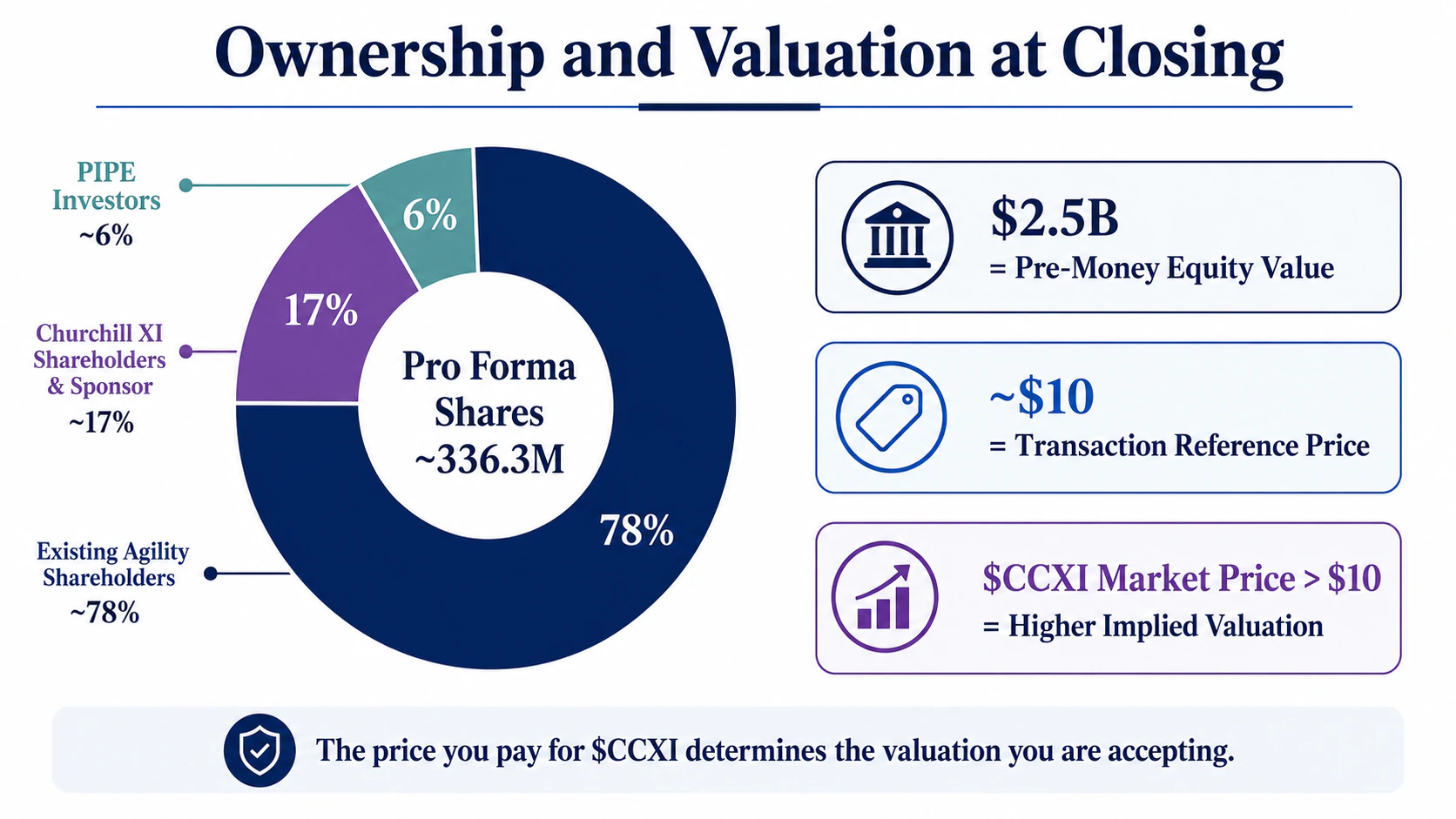

The headline transaction assigns Agility a $2.5 billion pre-money equity value.

“Pre-money” means the value assigned to Agility before the new transaction cash is added. It does not mean the combined public company will have a market capitalization of exactly $2.5 billion.

The investor presentation uses an illustrative transaction price of approximately $10 per share and assumes no Churchill shareholders redeem their stock. Under those assumptions, the proposed ownership structure is:

| Shareholder group | Illustrative shares | Approximate ownership | |---|---:|---:| | Existing Agility shareholders | 260.6 million | 78% | | Churchill XI shareholders and sponsor | 55.7 million | 17% | | PIPE investors | 20.0 million | 6% | | Total | 336.3 million | 100% |

Percentages do not add perfectly because of rounding. The Churchill figure includes the public Class A shares and approximately 13.8 million Class B founder shares. The presentation’s share count excludes approximately 4.14 million public warrants and 0.05 million private-placement warrants.

The $2.5 billion figure therefore describes the negotiated value assigned to Agility’s existing equity. It is only one component of the combined company’s capital structure.

Why the CCXI share price changes the effective valuation

The transaction was negotiated around the trust value per share, illustrated at approximately $10. PIPE investors are also committing capital at $10 per share.

Public investors are free to trade $CCXI at a higher or lower price.

When $CCXI trades above $10, a new buyer is paying a premium to the negotiated transaction reference price. The market is effectively assigning Agility and the combined company a higher value than the valuation highlighted in the announcement.

A rough shortcut is:

Illustrative post-closing market capitalization ≈ CCXI share price × 336.3 million pro forma shares

Under that simplified calculation:

| CCXI share price | Approximate pro forma market capitalization | |---:|---:| | $10 | $3.36 billion | | $15 | $5.04 billion | | $20 | $6.73 billion |

This is a directional estimate rather than a final fully diluted valuation. The ultimate share count can change because of redemptions, transaction adjustments, equity awards, option exercises, warrants and future financing. Enterprise value will also differ from market capitalization because the combined company is expected to receive cash.

The important lesson is straightforward: a $2.5 billion deal announcement does not mean someone buying $CCXI at any price is still investing in Agility at $2.5 billion.

The premium above the transaction reference price belongs in the valuation analysis.

Where does the transaction cash come from?

The companies expect more than $620 million of gross transaction proceeds under the no-redemption assumption. The funding is expected to come from two main sources:

- Approximately $420 million held in Churchill XI’s trust account

- Approximately $200 million from a common-stock PIPE priced at $10 per share

The PIPE is led by Foxconn, with additional participation from existing and new institutional investors. After illustrative transaction expenses, the investor presentation estimates approximately $574 million of cash could reach the combined company’s balance sheet if there are no public-shareholder redemptions.

Agility says it plans to use the proceeds to fulfill existing orders, expand customer deployments, scale Digit v5 production and continue investing in robotics hardware, physical AI, safety systems, software and manufacturing infrastructure.

The capital raise is important because Agility remains in an expensive commercialization phase. Its investor presentation shows preliminary cash uses of approximately $75 million in 2024 and $102 million in 2025. The company has not achieved positive operating cash flow and says it expects continuing losses and significant expenses for the foreseeable future.

The transaction is therefore doing more than creating a ticker. It is financing the attempt to move from limited commercial deployments into larger-scale production.

What is a PIPE?

PIPE stands for private investment in public equity.

In a SPAC transaction, selected investors agree to buy shares directly from the combined company, usually at a fixed price and subject to the closing of the merger. In the Agility transaction, PIPE investors have committed approximately $200 million at $10 per share, equivalent to roughly 20 million shares.

A PIPE can serve several purposes. It adds capital, reduces the company’s dependence on the SPAC trust and can signal that institutional investors were willing to evaluate the transaction before committing money.

It does not guarantee that the public-market price is attractive. A buyer purchasing $CCXI above $10 is paying more than the PIPE investors’ subscription price. PIPE shares may also become part of the future tradable supply once their registration and contractual restrictions permit sales.

The PIPE price is best understood as part of the transaction structure, rather than a promise that the stock will remain above $10.

What are SPAC redemptions?

Before the merger vote, eligible public shareholders can generally choose to redeem their SPAC shares for their proportional share of the money in the trust account instead of remaining invested in the combined company.

A shareholder can vote for the deal and still choose redemption, depending on the applicable terms and deadlines. Redemption is therefore different from voting against the merger.

Redemptions matter because they remove cash from the trust. The announced estimate of approximately $420 million from Churchill assumes no public shareholders redeem. Heavy redemptions could leave Agility with less capital than the headline proceeds suggest.

The merger agreement requires at least $200 million of available closing cash, measured after redemptions and including qualifying incremental financing, before certain transaction expenses and repayments. If that minimum cash condition is not satisfied or waived, Agility is not obligated to complete the transaction.

Investors should therefore watch both the shareholder vote and the redemption rate. A transaction can receive enough votes to pass while still losing a meaningful portion of the expected trust cash.

How much of Agility will current CCXI shareholders own?

Under the presentation’s no-redemption illustration, Churchill XI shareholders and sponsor shares would represent roughly 17% of the combined company. PIPE investors would own approximately 6%, while existing Agility holders would retain about 78%.

This structure tells investors two things.

First, buying one share of $CCXI does not mean acquiring the same percentage of Agility that a private shareholder received at the negotiated pre-money valuation. Existing Agility shareholders receive most of the post-closing equity.

Second, existing Agility investors are rolling 100% of their holdings into the transaction rather than receiving cash at closing. The company says existing Agility shares will be subject to a 180-day lock-up. Sponsor shares are also subject to a lock-up, although the transaction documents provide for a potential early release if specified post-closing trading conditions are met.

Rollover and lock-ups improve alignment at closing, but they do not permanently remove selling pressure. Investors should track registration rights, lock-up expiration dates and any early-release conditions after the merger.

Where can dilution come from?

The headline ownership table is a starting point rather than the final fully diluted share count.

Potential dilution includes:

- Churchill founder shares

- Public and private-placement warrants

- Existing Agility options and equity incentive awards

- New employee equity compensation

- Future capital raises

- Shares or warrants issued through commercial agreements

The investor presentation includes the dilutive impact of certain existing Agility equity awards and options in its ownership illustration, but it excludes approximately 4.19 million Churchill public and private warrants. Exercising those warrants could create additional shares after closing.

The risk is larger than a single warrant calculation. Agility says its business is capital intensive and may require additional financing sooner than expected. Future equity issuance could fund growth while reducing the ownership percentage represented by each existing share.

That is why a SPAC valuation should be assessed using a fully diluted share framework whenever possible.

Does Agility already have $300 million in revenue?

No.

Agility reports more than $300 million of multi-year orders for Digit v5. That figure is commercially meaningful, but the investor presentation explicitly says it is not a measure of current-period revenue.

The disclosed order amount relates to 1,000 Digit v5 robots under a three-year Robots-as-a-Service agreement. The value is expected to be realized over time and depends on Agility achieving contractual development, manufacturing and deployment milestones. The agreement also includes warrants issued to the purchaser that vest in proportion to robots deployed.

This creates an important distinction:

- Order value represents potential future contract value.

- Revenue is recognized as Agility delivers products or services under the applicable accounting rules.

- Cash flow depends on payment timing, manufacturing cost, deployment expense and ongoing support requirements.

An order can be delayed, reduced or fail to become revenue if product milestones are missed. Revenue can also grow without producing positive cash flow if robots remain expensive to manufacture and maintain.

The $300 million figure should therefore be treated as evidence of customer interest and potential demand, rather than as $300 million already earned.

How does Agility Robotics plan to make money?

Agility currently presents two primary commercial models for Digit v5.

Under Robots-as-a-Service, Agility retains ownership of the robot and receives a deployment fee plus recurring subscription payments. The subscription includes access to the Arc software platform and maintenance services.

Under the ownership model, the customer purchases Digit upfront and continues paying for software, maintenance and related services.

Management’s illustrative model estimates approximately $500,000 of cumulative five-year revenue per robot under RaaS and approximately $400,000 under the ownership model. These figures are internal assumptions, not historical results at commercial scale. They depend on robot life, uptime, deployment cost, maintenance expense, pricing and customer retention.

The financial case will ultimately depend on more than the number of robots shipped. Investors need to know:

- How frequently each robot can perform useful work

- How much maintenance and human supervision it requires

- Whether customers expand from pilots into larger fleets

- How quickly production costs decline

- Whether recurring software and service revenue carries attractive margins

- Whether Digit remains competitive with fixed automation and less complex mobile robots

These variables determine whether Agility develops into a scalable automation platform or remains a capital-intensive hardware supplier.

For the broader business model, competitive position, and investment risks, read our full analysis of the CCXI and Agility Robotics investment case.

What must happen before CCXI becomes AGLT?

Signing a definitive agreement does not complete the merger.

Churchill must file the required registration statement and proxy materials with the SEC. The registration statement will contain more complete financial statements, transaction details, ownership information, risk disclosures and voting materials.

The transaction then requires Churchill shareholder approval, Agility shareholder approval, an effective SEC registration statement, the required regulatory clearances and approval to list the combined company’s shares. It must also satisfy the minimum cash condition and the remaining contractual closing requirements.

The investor presentation targets a fourth-quarter 2026 closing. The merger agreement allows either side to terminate under certain circumstances if the transaction has not closed by December 31, 2026.

Until the transaction closes, several outcomes remain possible:

- The deal closes substantially as announced

- The terms are amended

- Shareholder redemptions reduce available cash

- Additional financing changes the capital structure

- The closing is delayed

- The agreement is terminated

The market can price the probability of a successful deal, but the ticker change is not guaranteed in advance.

What should investors watch next?

The next major source document will be the registration statement and proxy prospectus. It should provide the financial and ownership information needed to move beyond the investor presentation.

The most useful questions will be:

How much historical revenue has Agility generated?

The announcement emphasizes deployments, runtime and contracted orders. Investors still need audited revenue, gross-margin and cash-flow information.

How concentrated are the orders?

The disclosed $300 million order value relates to 1,000 robots under one three-year RaaS contract. The customer concentration and contract milestones matter.

How much cash survives redemptions and fees?

The difference between gross proceeds and cash delivered to the balance sheet will affect Agility’s funding runway.

Can Digit v5 launch and scale on schedule?

Digit v5 remains under development. Manufacturing, software, safety and supply-chain delays could postpone revenue recognition.

How large is the fully diluted share count?

Investors need to include options, founder shares, warrants and any additional financing when estimating valuation.

When do restricted shares become tradable?

Lock-up expirations and registration rights can materially change the public float after closing.

These questions are more useful than treating the original $2.5 billion announcement as a complete valuation.

The bottom line

$CCXI offers public investors a potential path into Agility Robotics before the proposed merger closes. It does not yet represent a completed investment in the operating company.

The transaction assigns Agility a $2.5 billion pre-money equity value, adds capital from the Churchill trust and a $200 million PIPE, and is expected to leave existing Agility shareholders with most of the combined company. If the deal closes, Churchill XI is expected to become Agility Robotics and trade as $AGLT.

The price investors pay for $CCXI still determines the valuation they are accepting.

A buyer at $10 is entering near the transaction’s illustrative reference price. A buyer at a substantial premium is making a larger bet that humanoid robotics scarcity, Agility’s deployments and future commercialization will justify a higher public-market valuation.

The ticker is the easy part. The durable investment case depends on whether contracted orders become deployed robots, recognized revenue, sustainable margins and eventually positive cash flow.

FAQ

Is CCXI already Agility Robotics?

No. CCXI currently represents Churchill Capital Corp XI, the SPAC that has agreed to combine with Agility Robotics. The operating-company merger has not yet closed.

Will CCXI shares become AGLT shares?

If the transaction closes under the announced structure, Churchill XI will be renamed Agility Robotics and the combined company is expected to trade under the ticker AGLT. Existing Churchill Class A shares are expected to convert into common shares of the domesticated public company.

Is Agility Robotics going public through an IPO?

Agility is going public through a SPAC business combination rather than a traditional underwritten IPO. Searches may still refer to it informally as the Agility Robotics IPO.

Why is $10 important in a SPAC deal?

The transaction presentation uses an illustrative trust value of approximately $10 per share, and the PIPE is priced at $10. It is a transaction reference point, not a guarantee that the public stock will trade at or above $10.

Does the $2.5 billion valuation include the new cash?

No. The $2.5 billion figure is the proposed pre-money equity value assigned to Agility before the transaction proceeds are added.

Are Agility's $300 million of orders the same as revenue?

No. The figure represents potential multi-year contract value subject to milestones. The company explicitly states that it is not a measure of current-period revenue.

Can the CCXI merger fail?

Yes. The transaction still depends on shareholder approvals, SEC effectiveness, listing approval, minimum cash, and other closing conditions. The agreement can also be terminated under specified circumstances.

Does buying CCXI provide downside protection near $10?

Eligible public shareholders may have redemption rights tied to the trust value at the shareholder vote, subject to the transaction documents and deadlines. That mechanism is not the same as a permanent market-price floor, particularly for shares purchased well above trust value.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Churchill Capital Corp XI Form 8-K and transaction exhibits | U.S. Securities and Exchange Commission | 2026-06-24 | SEC | Merger structure, exchange mechanics, closing conditions, minimum cash, PIPE terms, lock-ups, and termination provisions. |

| 2 | Agility Robotics Investor Presentation | U.S. Securities and Exchange Commission | 2026-06 | SEC | Pro forma ownership, sources and uses, warrants, orders, unit economics, and risk disclosures. |

| 3 | Agility Robotics transaction announcement | Agility Robotics | 2026-06-24 | Company IR | Proposed valuation, expected proceeds, PIPE, customers, orders, and expected AGLT ticker. |

| 4 | Agreement and Plan of Merger and Reorganization | U.S. Securities and Exchange Commission | 2026-06-24 | SEC | Legal structure of the proposed business combination and treatment of securities. |

The transaction remains proposed as of July 12, 2026. Sources below are official SEC filings and Agility Robotics materials.

Related Reading

Serenity Is Watching CCXI: Humanoid Robots Finally Have a Public-Market Entry Point. But Is It a Good Investment?

CCXI could become a rare public-market window into humanoid robotics, but investors still need to separate theme exposure from proven economics.

NVIDIA’s Next Bottleneck Isn’t GPUs. It’s Data Movement.

Why AI factories are moving from copper to optical connectivity — and which suppliers deserve deeper research

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. SPAC transactions, pre-commercial technology companies, and humanoid robotics investments may involve substantial volatility, dilution, execution risk, and loss of capital.

Comments