Micron’s latest quarter was strong enough that the headline numbers almost explain themselves. Revenue surged, gross margin reached levels most memory investors would not have expected a few years ago, and management guided for even stronger profitability in the next quarter.

But a strong quarter is not the interesting part of the Micron story anymore.

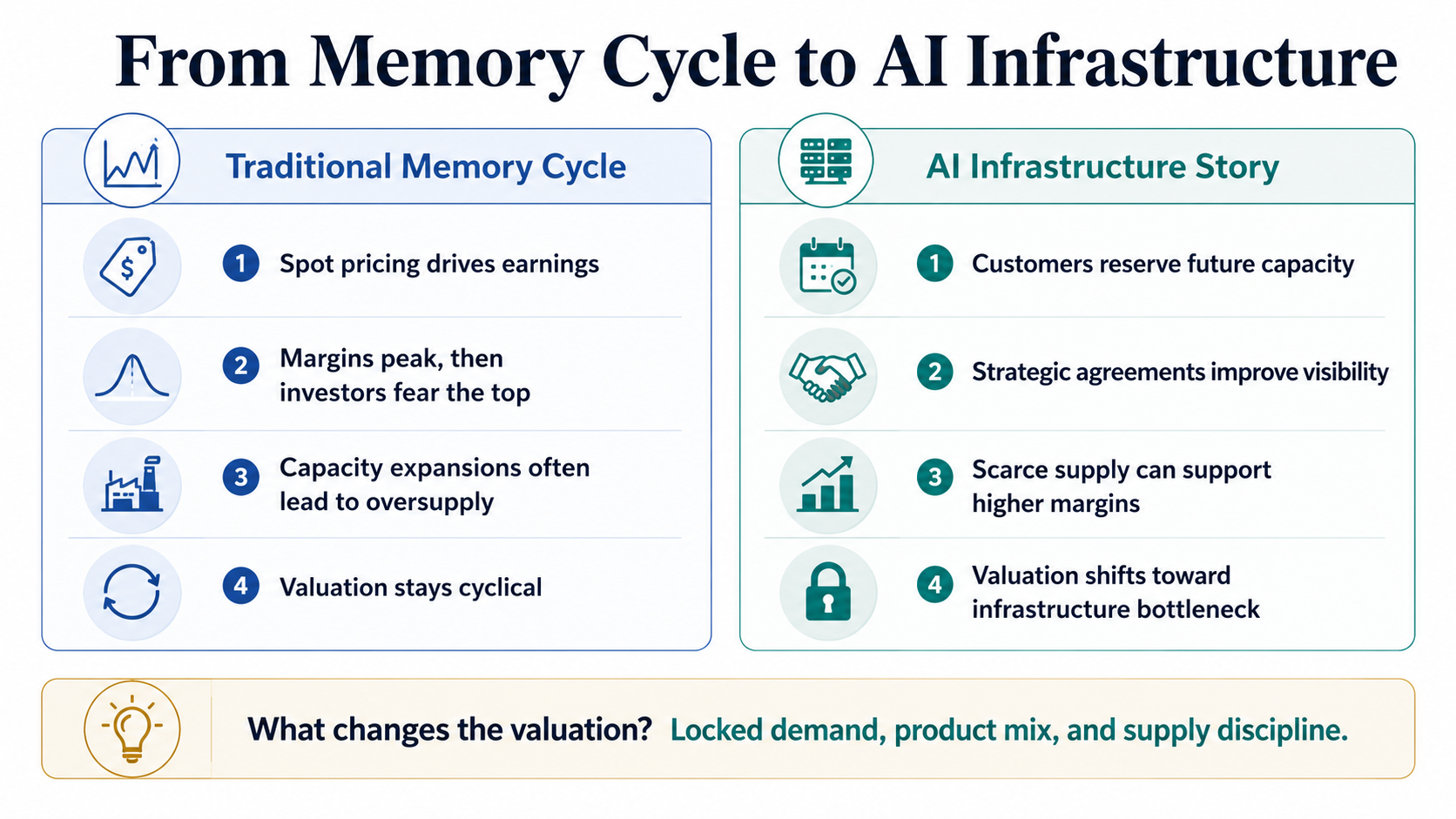

The real question is whether Micron is still being priced as a classic memory-cycle stock, or whether AI is starting to pull the company into a different category: a supplier of scarce infrastructure capacity that large customers are willing to reserve years in advance.

That distinction matters because memory stocks have always carried a strange curse. When earnings are weak, investors worry about the downturn. When earnings are too strong, they start worrying about the top. High margins can look bullish on the surface, but in a cyclical industry they also invite a familiar fear: if pricing is this good now, new supply may eventually catch up and destroy the margin structure.

Micron is trying to break out of that old pattern. The company is arguing, implicitly and explicitly, that AI has changed the value of memory. In a world where training clusters, inference workloads, long-context models, and custom AI accelerators all need more memory bandwidth and capacity, memory is no longer just another component in the server bill of materials. It is becoming one of the limiting factors in AI infrastructure.

That is a powerful story. It is also not fully proven yet.

Micron has earned the right to make the argument. The real test is whether the company can still make it after 2027, when new capacity, customer commitments, HBM4E ramps, and AI capital spending all start colliding with one another.

Micron is asking investors to move from a cycle framework to an infrastructure-capacity framework.

How AI Spending Actually Reaches Micron

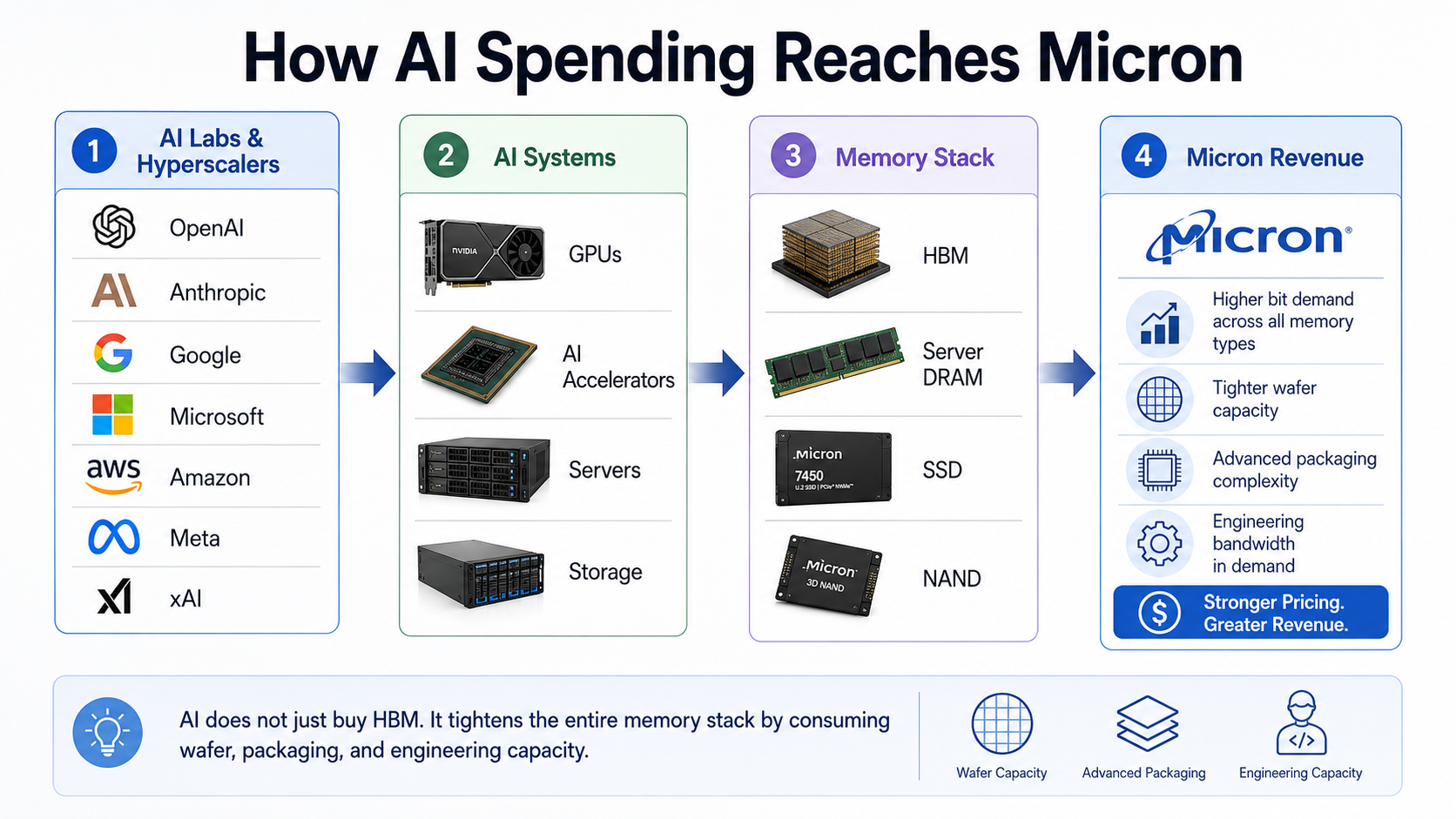

AI capital spending does not move in a straight line from OpenAI, Anthropic, Google, Microsoft, Amazon, Meta, or xAI into Micron’s revenue. The path is indirect. AI labs and cloud companies build larger clusters. Those clusters require GPUs, custom accelerators, servers, storage, networking, and data center systems. Those systems, in turn, need HBM, server DRAM, enterprise SSDs, and NAND.

That is where Micron enters the story.

Micron’s Q3 revenue reached $41.46 billion, up from $23.86 billion in the prior quarter and $9.30 billion a year ago. The segment breakdown is just as important as the total. Cloud Memory generated $13.77 billion. Core Data Center generated $11.52 billion. Mobile and Client generated $11.52 billion. Automotive and Embedded generated $4.63 billion.

The obvious conclusion is that data center demand is the main driver. The less obvious conclusion is that AI is no longer only an HBM story. HBM absorbs wafer supply, advanced packaging capacity, engineering resources, and customer qualification bandwidth. Once those resources are pulled into AI platforms, the rest of the memory market tightens as well. Server DRAM becomes more valuable. Enterprise SSD demand improves. NAND pricing gets support. Even customers outside AI have to deal with a more constrained supply environment.

That is why Micron’s AI exposure should not be reduced to one product line. AI is not merely buying HBM. It is tightening the entire memory stack.

For investors, that is the first real shift in the thesis. Micron is benefiting not only from a product cycle, but from the repricing of memory capacity itself.

AI capex reaches Micron through the server, accelerator, memory, and storage stack, not through a single direct customer line.

Why the 86% Gross Margin Guide Cuts Both Ways

Micron reported Q3 GAAP gross margin of 84.6% and non-GAAP gross margin of 84.9%. For Q4, management guided both GAAP and non-GAAP gross margin to roughly 86%.

Those are extraordinary numbers. They also create the central tension in the stock.

In software, an 86% gross margin usually supports the idea of durable profitability. In memory, it raises a different question: is this what a new AI-driven business model looks like, or is this simply what peak pricing looks like before the next supply response?

That may sound cautious, but it is exactly how memory investors have been trained to think. The industry has a long history of moving from shortage to overinvestment. Demand improves, pricing rises, margins expand, suppliers add capacity, and eventually the additional supply pressures pricing again. The market rarely waits for the downturn to appear in reported earnings. It starts discounting it early.

Micron’s answer is that this cycle is structurally different. The company is pushing into higher-value products such as HBM4, HBM4E, 256GB DDR5 RDIMMs, PCIe Gen6 SSDs, and 245TB QLC SSDs. Management has said HBM4 is moving toward high-volume shipments for a lead customer platform, while HBM4E is expected to enter volume production in 2027.

That supports the idea that product mix is improving. It also supports the argument that AI memory is harder to commoditize than older DRAM cycles.

Still, supply and demand have not disappeared. If Samsung, SK hynix, and Micron all add meaningful capacity into 2027 and 2028, and if AI demand growth slows at the same time, pricing will come under pressure. AI may raise the strategic value of memory, but it does not repeal the basic economics of the industry.

So the 86% margin guide is not the final answer. It is the question investors now have to solve.

Micron has to prove that today’s margins are supported by more than temporary pricing strength. It has to show that the margins are backed by customer commitments, product differentiation, supply discipline, and the ability to convert demand into real shipments.

Strategic Customer Agreements Are the Strongest Evidence

The most important evidence in Micron’s favor is not the margin guide by itself. It is the company’s Strategic Customer Agreements.

According to earnings call commentary and market reporting, Micron has signed 16 SCAs, including four very large customers and three medium-sized customers, with the rest largely from automotive customers. These agreements reportedly cover about 20% of DRAM volume and about one-third of NAND volume. Even more important, 14 of the agreements represent roughly $100 billion of minimum cumulative revenue over the remaining contract terms, based on minimum contractual pricing.

This matters because the biggest weakness of the traditional memory business has never been the absence of good years. The weakness is that investors do not trust the good years to last.

SCAs are Micron’s attempt to change that perception. They move part of the business away from purely spot-driven pricing and toward longer-term customer commitments. For customers, the motivation is supply assurance. For Micron, the benefit is better visibility and less earnings volatility.

That does not turn DRAM into software. It does not make Micron a subscription business. It does not eliminate the cycle.

But it may change the shape of the cycle. If a meaningful portion of future volume has pricing floors, minimum purchase commitments, deposits, or take-or-pay economics, Micron’s downside may be less severe than in prior cycles. The company would still be cyclical, but not necessarily cyclical in the same way.

That is why the SCA disclosure is so important. It is the closest thing in this quarter to evidence that Micron is becoming an infrastructure bottleneck rather than just another beneficiary of a memory upturn.

The Agreements Help, But They Do Not Settle the Debate

The case for Micron is stronger than it was before this quarter. It is not complete.

Even if the reported SCA coverage is accurate, those agreements still do not cover the whole company. A large portion of Micron’s DRAM and NAND business remains exposed to market pricing, customer inventories, supply additions, and end-market demand. The company has also not disclosed the customer names, exact contract lengths, volume commitments, pricing formulas, renegotiation terms, cancellation protections, or product mix behind the agreements.

That is a major limitation. A $100 billion minimum cumulative revenue figure sounds large, but it is spread across multiple years. It is not annual revenue, and it is not a profit guarantee.

This is where investors need to be careful. SCAs can improve visibility without proving that Micron has fully escaped the memory cycle. They may justify a higher multiple than the market has historically assigned to deep-cycle memory stocks, but they do not remove the need to watch supply, pricing, capex discipline, and customer demand after 2027.

The right way to frame SCAs is as a partial answer. They are a serious step toward a more durable business model. They are not proof that the transformation is finished.

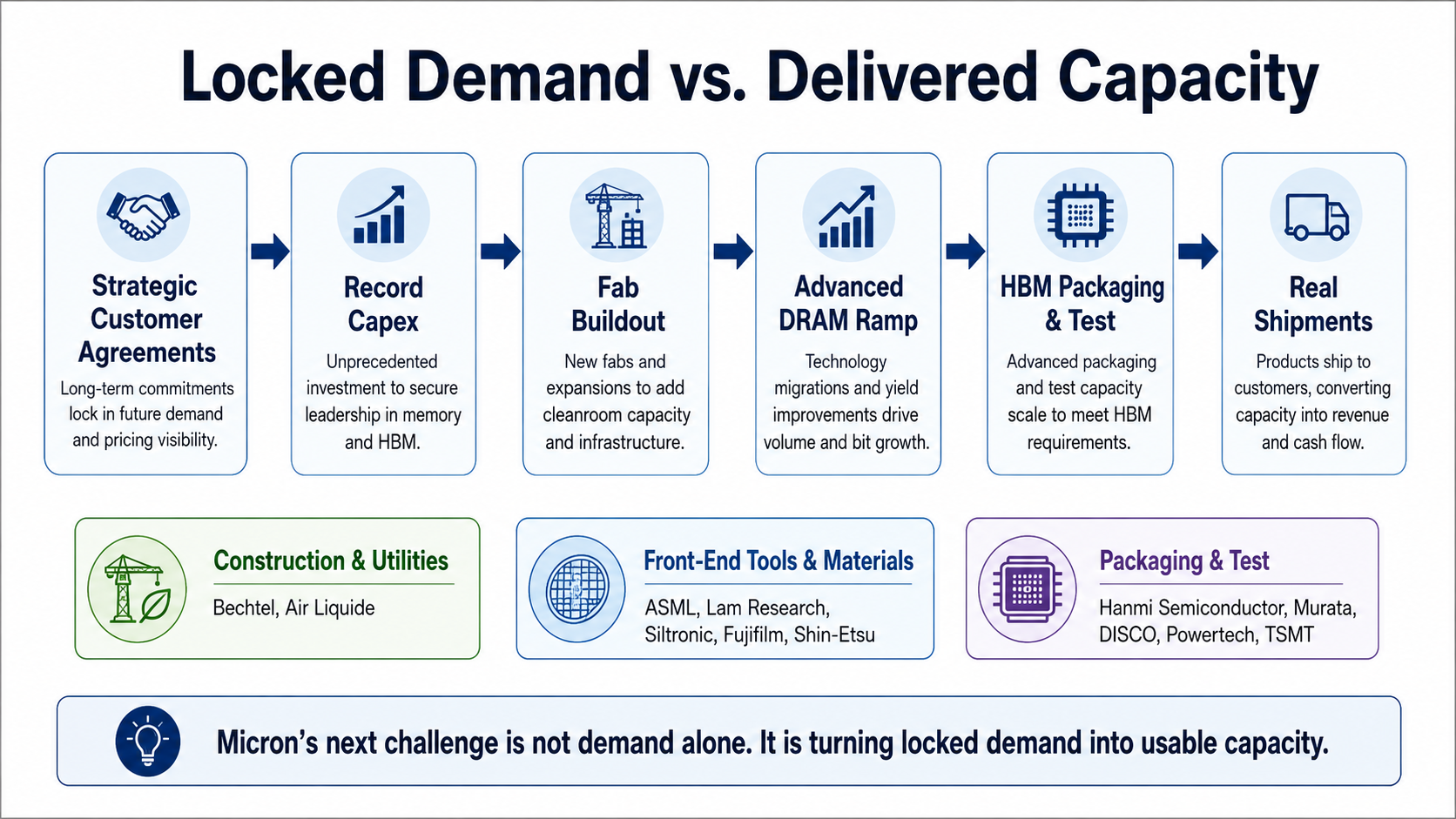

Once Demand Is Reserved, Capacity Becomes the Next Test

If customers are willing to reserve future memory supply, Micron’s next challenge is no longer just finding demand. It is turning that demand into usable capacity.

The capex numbers make that clear. Micron expects around $10 billion of capex in Q4, roughly $27 billion for fiscal 2026, and quarterly capex in fiscal 2027 that will be even higher than Q4. That is not routine maintenance spending. It is a race to convert AI-driven demand into actual output.

This is where the supply chain becomes part of the investment thesis. A semiconductor shortage does not end just because a company announces a larger budget. New capacity has to be built, equipped, qualified, and ramped. That requires fabs, cleanrooms, gases, chemicals, power systems, lithography tools, deposition tools, etch tools, metrology, wafers, packaging, testing, and yield improvement.

Micron’s own execution now depends partly on the companies helping it turn capex into production.

At the fab level, Micron selected Bechtel as the construction partner for its New York megafab project. Air Liquide is investing more than $250 million to build ultra-high-purity industrial gas infrastructure for Micron’s Idaho fab. These companies do not make HBM, but they help create the physical foundation that future memory supply depends on.

At the equipment and materials level, Micron has a multi-year EUV agreement with ASML for future DRAM nodes. Lam Research has been recognized by Micron as a front-end capital equipment supplier. Micron’s supplier awards have also highlighted names such as Siltronic, Fujifilm Electronic Materials, and Shin-Etsu in materials-related areas. This part of the chain matters because advanced DRAM is not only about adding wafer capacity. It is about producing more usable chips from more complex process nodes.

Packaging and testing are another bottleneck. HBM is not ordinary DRAM. It requires multiple DRAM dies to be stacked, bonded, tested, and qualified before shipment into AI platforms. A packaging or test constraint can limit final shipments even if wafer supply improves. Micron’s supplier ecosystem includes Hanmi Semiconductor in assembly and test equipment, along with companies such as Murata, Tripod, DISCO, Neosem, Powertech, and TSMT across assembly, test, external manufacturing, and related categories.

This is why the better supply-chain question is not simply, “Which semiconductor equipment stocks benefit from AI?” That is too broad. The sharper question is: who helps Micron turn reserved demand into deliverable supply?

That should be treated as a research map, not a confirmed investment conclusion. Micron has not disclosed order sizes for each supplier or specified which companies are tied to HBM4, HBM4E, 1-beta, 1-gamma, or individual fab ramps. But the direction of research is clear. If Micron’s AI memory thesis is right, the next layer of opportunity may sit with the companies that help build the capacity behind it.

Locked demand only matters if Micron can turn capex into qualified, deliverable capacity.

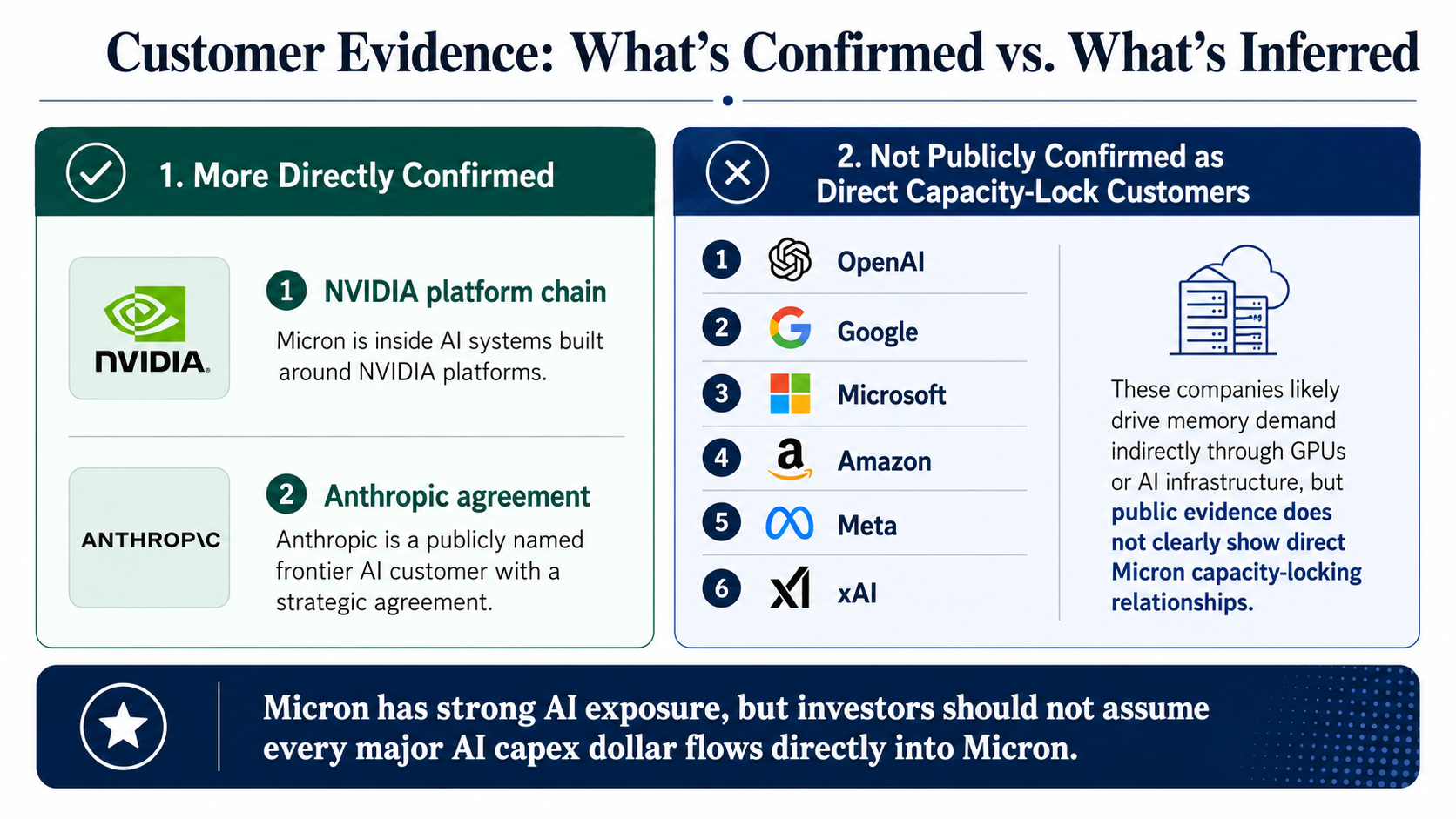

The Customer Evidence Is Strong, But Not as Simple as Investors Want

Many investors want the big customer names. That is understandable. If Micron is locking up future AI memory demand, the natural question is whether the customers are NVIDIA, AMD, hyperscalers, AI labs, AI ASIC programs, or automotive companies.

Micron has not named the SCA customers. The company has said HBM4 is moving toward high-volume shipments for a lead customer platform and that it is sampling to multiple end customers, but it has not disclosed the names behind the agreements.

That creates a temptation to fill in the blanks. Investors should resist it.

The strongest public evidence for Micron’s AI exposure is its position inside NVIDIA’s AI platform chain and its strategic agreement with Anthropic. The Anthropic agreement is especially notable because it shows Micron working directly with a frontier AI company on memory and storage architecture, supply, enterprise AI adoption, and strategic investment. That is different from simply being a component supplier buried several layers inside a server system.

But the broader customer picture is mixed. OpenAI’s Stargate-related memory reports have pointed more clearly to Samsung and SK hynix. Google TPU supply chain signals have leaned more toward Samsung. Microsoft Maia 200 HBM3E reports have pointed toward SK hynix. Amazon Trainium, Meta, and xAI almost certainly drive large memory demand through NVIDIA systems or custom AI infrastructure, but public evidence is not enough to show direct Micron capacity-locking relationships.

That does not weaken the Micron thesis as much as it defines its boundaries.

Micron has strong AI exposure. What investors should not assume is that every major AI capex dollar flows directly into Micron. The more precise conclusion is that Micron is already benefiting from AI infrastructure through platform-driven demand, and it now has at least one publicly named frontier AI relationship through Anthropic. The next step is proving that customer lock-in extends more broadly across the largest AI spenders.

Customer evidence matters most when confirmed relationships are separated from inferred AI demand.

Why 2027 Is the Real Test

Micron’s management story is coherent. AI is increasing the strategic value of memory. Customers are reserving future capacity. The company is investing heavily in technology, products, and supply. SCAs should make financial performance more durable and predictable.

That story can work, but it depends on several conditions holding at the same time.

AI capex cannot be a one-year rush. It has to continue pulling demand for HBM, server DRAM, SSDs, and NAND. Samsung, SK hynix, and Micron have to avoid repeating the old memory mistake of adding too much supply into the same window. The SCAs must create real volume and pricing protection rather than being renegotiated when conditions change. Micron must hold its competitive position in HBM4, HBM4E, and high-end data center products. And the company must convert record capex into real output, not just future supply promises.

That is why the period after 2027 matters so much. By then, AI demand, SCA durability, HBM4E production, industry capacity additions, and supplier execution will all be tested together.

My view is that Micron should no longer be treated as a simple replay of the last memory upcycle. The customer commitments, AI demand profile, and product mix are stronger than in a normal cycle. At the same time, Micron has not fully earned an AI infrastructure valuation yet. The company sits in the middle: its financial performance increasingly resembles a scarce infrastructure bottleneck, while its industry structure still carries cyclical risk.

If SCAs truly lock demand beyond 2027 and include effective pricing protection, Micron’s earnings volatility should be lower than in prior cycles. The stock may deserve a higher multiple than a traditional memory stock.

If capacity catches up, pricing protection proves weak, or AI capex slows, the 86% gross margin guide will look less like the start of a new business model and more like the peak of another memory cycle.

That is the real test for Micron now. Not whether the company can deliver another strong quarter, but whether it can turn a powerful AI memory cycle into a more predictable AI infrastructure business.

Related Reading

- Micron Earnings Eve: The Market Has Already Bought the Growth

- AI Semiconductor Bottlenecks: The System, Not the Chip

- Nvidia’s Next Bottleneck Is Data Movement

Sources & Notes

Sources for this article are listed below. Strategic Customer Agreement details beyond Micron's official press release are treated as market-reported earnings-call commentary, not as SEC-filed contract terms.

Primary source for Q3 revenue, gross margin, Q4 guidance, business-unit revenue, product highlights, and management commentary.

Primary filing wrapper for the Q3 FY2026 earnings release.

Earnings-call reporting on 16 SCAs, customer mix, DRAM/NAND volume coverage, and minimum cumulative revenue commentary.

Management commentary on SCAs improving durability and predictability.

Earnings-call reporting on Q4 capex, FY2026 capex, FY2027 quarterly capex, and cleanroom construction.

Earnings-material reporting on tight memory conditions beyond 2027 and greenfield fab complexity.

Publicly named Anthropic relationship and scope of memory and storage collaboration.

Ultra-high-purity gas infrastructure investment tied to Micron's Idaho fab.

Reference source for prepared remarks, earnings-call materials, HBM roadmap, capex, EUV, and supplier-execution commentary.

- Micron New York megafab construction partnership

Supports discussion of the New York megafab construction layer in the capacity-conversion thesis.

- Micron Supplier Day / Supplier Awards

Supports supplier ecosystem references including equipment, materials, assembly, test, and external manufacturing categories.

Disclosure

This article is for research and education only. It is not investment advice.