The most dangerous moment in a semiconductor cycle is not always when earnings disappoint.

Sometimes it is when everyone already knows the numbers will look spectacular.

That is where Micron stands before its fiscal Q3 report.

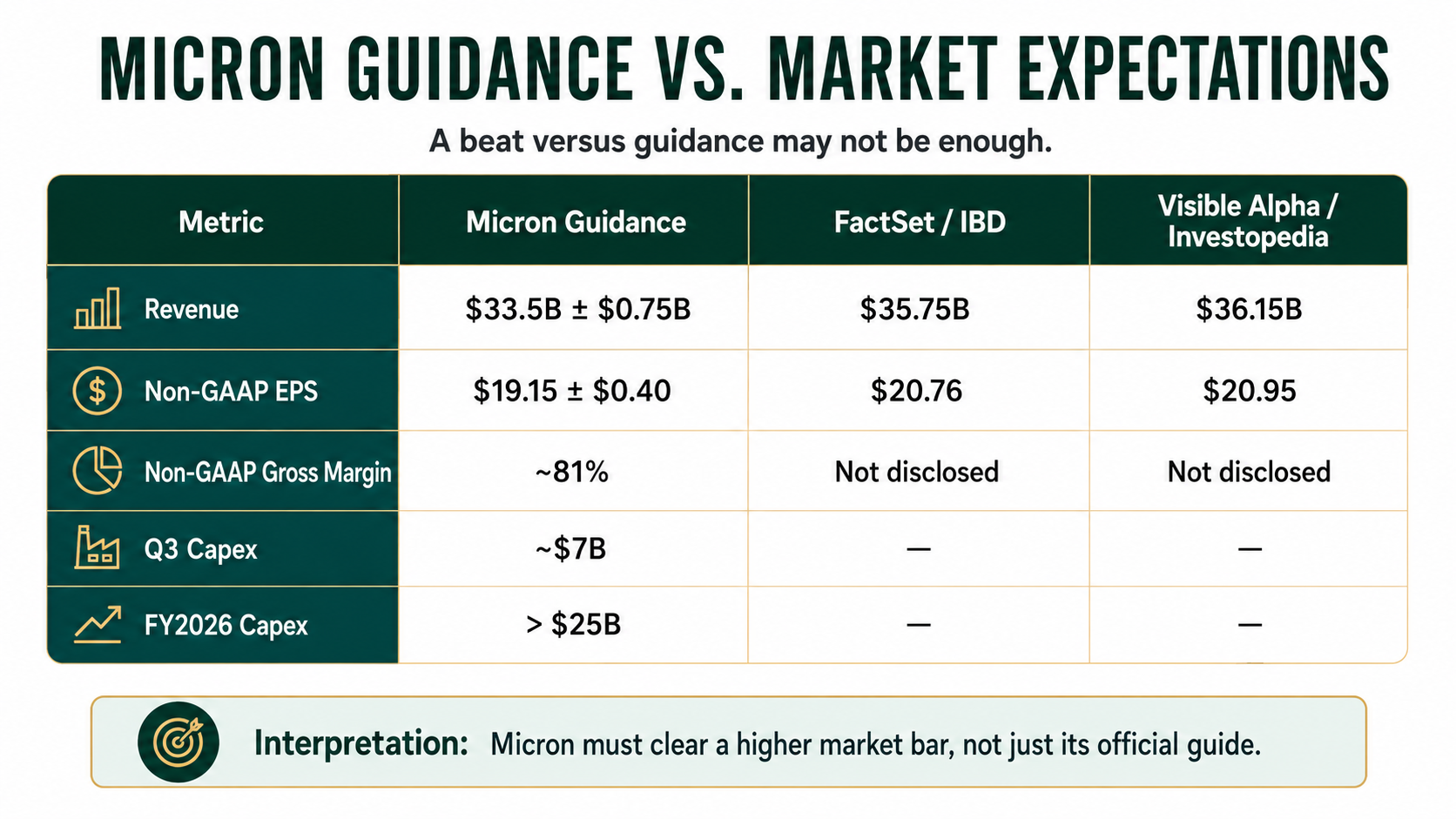

The market is no longer debating whether HBM demand is strong. That conversation is over. AI servers need more memory. Nvidia’s next platforms need more bandwidth. Cloud operators are still building AI clusters. Micron’s own guidance is already extremely high, and third-party expectations have moved above that guidance.

So this is not a low-expectation earnings setup.

It is a high-expectation verification event.

The bar is no longer Micron’s official guide. Market expectations have already moved above company guidance.

The real question is not whether Micron can report growth. The market has already paid for growth.

The real question is where the profits are coming from.

Are Micron’s current profits the late-stage surge of a traditional memory upcycle?

Or is AI beginning to reshape the supply structure of the entire memory market?

Those are two very different stories.

If this is just another memory cycle, then high gross margins, explosive EPS growth, and record guidance may eventually become warning signs. Investors will start looking ahead to capacity additions, pricing normalization, and margin compression.

But if AI is changing how memory capacity is allocated, then Micron is not only an HBM beneficiary.

It may be one of the clearest examples of how AI is tightening the broader memory stack.

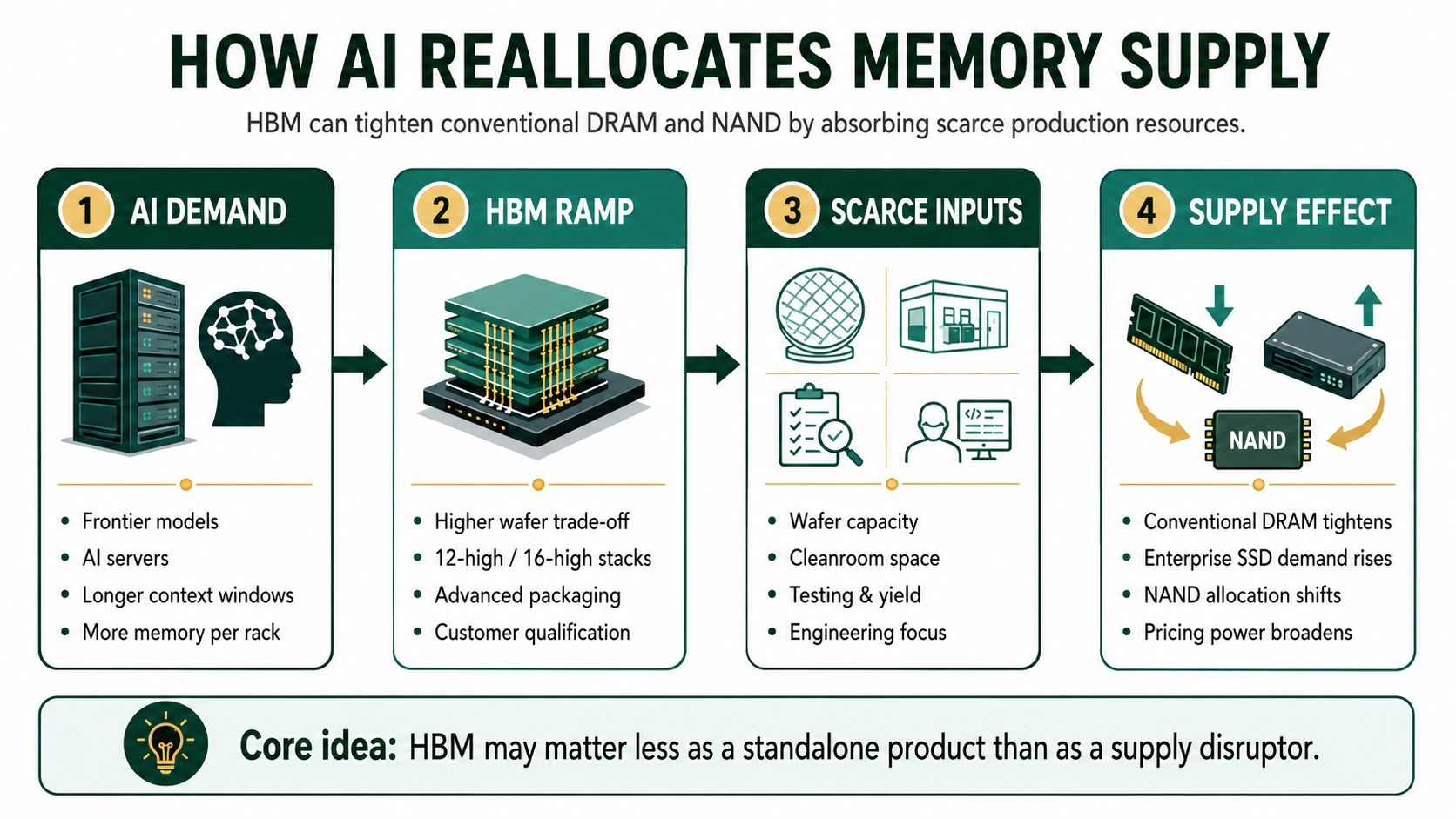

HBM is not just another DRAM product

HBM is often described as if it were simply a premium DRAM product.

That misses the point.

HBM consumes more of the industry’s scarce inputs: wafer capacity, cleanroom space, advanced packaging, testing resources, engineering time, and customer qualification cycles.

Micron has already said that DRAM bit supply growth is constrained by cleanroom limitations, long construction lead times, higher HBM trade ratio, faster HBM growth, and lower bit-per-wafer gains from node migration.

That matters.

It means HBM growth can reduce the effective supply available for conventional DRAM.

This is the real supply-side question behind Micron’s earnings.

If more capacity is redirected toward HBM, then standard DRAM becomes tighter. If AI data centers absorb more enterprise SSD and NAND supply, then NAND can also tighten. If customers begin planning memory and storage years ahead of deployment, the old spot-cycle logic becomes less useful.

This is why Micron’s margin expansion should not be read only as an HBM story.

Micron has not disclosed HBM revenue. It has not disclosed HBM gross margin. It has not disclosed HBM versus non-HBM profitability.

What it has disclosed is broader pricing strength.

In fiscal Q2, DRAM revenue was $18.8 billion, or 79% of total revenue, with sequential pricing up in the mid-60% range. NAND revenue was $5.0 billion, or 21% of total revenue, with sequential pricing up in the high-70% range.

This is the important part.

The profit surge may not be coming only from one AI product.

HBM is not just another memory product. It can absorb scarce wafer, cleanroom, packaging, testing, and engineering resources.

It may be coming from a broader supply squeeze created by AI’s demand for memory, bandwidth, and storage.

The Anthropic deal is a signal, not a financial model input

Micron’s strategic agreement with Anthropic is interesting, but it should not be overstated.

So far, the agreement does not disclose deal size, purchase volume, pricing, duration, prepayments, take-or-pay terms, capacity reservations, revenue contribution, or margin impact.

That means it cannot be treated as a near-term earnings catalyst.

At least not yet.

The more important signal is strategic.

Anthropic is not a normal customer. It is a frontier model company. If frontier model labs are now working directly with memory suppliers on memory and storage architecture, then memory is moving upstream in the AI infrastructure conversation.

It is no longer just a component purchased after the compute cluster is designed.

It is becoming part of the architecture itself.

That does not change Micron’s Q3 numbers by itself. But it raises a more important 2027 question:

Are AI model companies starting to secure memory and storage supply earlier, more directly, and with more strategic commitment?

If yes, that could improve visibility for future capacity planning.

If no, then this is simply customer validation without financial weight.

The real questions for the call

The sentence “HBM demand remains strong” will not be enough.

Everyone already knows that.

What matters is whether management can explain the quality and durability of the current profit pool.

The first question is margin source.

Is the expected 81% non-GAAP gross margin being driven mainly by HBM mix? Or is it being supported by conventional DRAM, NAND, and enterprise SSD pricing as well?

If the answer is the broader memory stack, the cycle may be more durable than a single-product HBM story.

The second question is capacity displacement.

How much is HBM expansion constraining conventional DRAM bit supply?

This is not a theoretical issue. Micron has already linked DRAM bit supply constraints to cleanroom space, construction lead times, HBM trade ratio, HBM growth, and node migration limits.

The third question is 2027 capex discipline.

Micron is raising capital spending. The issue is not whether capex is high. The issue is whether that capex is backed by strategic customer agreements, capacity commitments, pricing visibility, or long-term supply planning.

If capex is customer-backed, the market may treat it as disciplined expansion.

If it looks like a supplier chasing peak pricing, the market will start worrying about the next oversupply cycle.

The fourth question is Anthropic.

Does the agreement include hard terms: capacity reservation, pricing protection, prepayment, volume commitment, or product-specific supply?

If not, it remains a useful signal, but not a financial catalyst.

The fifth question is whether the bottleneck is still inside Micron.

Right now, the strongest verified control points remain inside Micron: wafer allocation, cleanroom expansion, HBM roadmap execution, Singapore advanced packaging, and NAND / enterprise SSD allocation.

External upstream areas such as hybrid bonding, advanced packaging equipment, metrology, testing, yield management, and SSD controllers remain watchlist items. They are plausible bottlenecks, but current evidence does not yet identify a clean public-market primary candidate beyond Micron itself.

That matters because it prevents a lazy conclusion.

This is not yet a story about “which upstream stocks benefit.”

It is still a story about whether Micron can prove that AI is changing the memory supply structure.

The verdict

Micron does not need to prove that HBM demand exists.

That has already been priced in.

It needs to prove something harder: that the current profit surge is not simply the top of a memory cycle.

If management can show that HBM’s trade-off ratio, DRAM/NAND supply constraints, enterprise SSD demand, strategic customer agreements, and 2027 capex are all pointing toward a structurally tighter supply regime, then this cycle may deserve a different valuation framework.

If not, even a great quarter could become just another well-anticipated peak-cycle print.

That is the real test.

Not whether Micron beats.

But whether Micron can prove that AI has changed the supply side of memory.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Micron FY2026 Q2 earnings release and Q3 outlook | Micron Investor Relations | 2026-03-18 | Primary / Company IR | Q3 revenue, gross margin, EPS, and operating expense guidance. |

| 2 | Micron FY2026 Q2 prepared remarks | Micron Investor Relations | 2026-03-18 | Primary / Company IR | Capex guide, DRAM/NAND supply constraints, HBM trade ratio, HBM4/HBM4E roadmap, and strategic customer agreements. |

| 3 | FactSet estimates via Investor's Business Daily | IBD / FactSet | 2026-06-22 | Reputable media / consensus estimate | Q3 revenue and EPS expectations above Micron guidance. |

| 4 | Visible Alpha estimates via Investopedia | Investopedia / Visible Alpha | 2026-06-22 | Reputable media / consensus estimate | Q3 revenue and EPS expectations above Micron guidance. |

| 5 | Micron-Anthropic partnership coverage | MarketWatch, Barron's | 2026-06-22 | Reputable financial media | Partnership scope and currently undisclosed financial terms. |

| 6 | TrendForce DRAM/NAND pricing context via Tom's Hardware | TrendForce / Tom's Hardware | 2026-04-01 | Industry data via media | DRAM/NAND contract price increases and broader supply tightness. |

| 7 | HBM upstream bottleneck scan | VIUS research note | 2026-06-23 | Internal research | Used to classify upstream suppliers as watchlist/broad proxy rather than verified primary candidates. |

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments