The market did not suddenly discover that indium phosphide exists. It discovered that a material once buried deep inside the optical supply chain could become a constraint on AI infrastructure.

That distinction explains much of the recent interest in AXT Inc.

AI investment initially concentrated on accelerators. It then moved upstream and outward into high-bandwidth memory, advanced packaging, networking switches, power generation and cooling. As constraints appeared across each layer, investors continued searching for the next component capable of delaying data-center expansion or redistributing profits within the AI infrastructure supply chain.

That search has now reached the substrates beneath optical chips.

Indium phosphide, commonly abbreviated as InP, is used in the production of high-speed lasers and other photonic devices that transmit data through optical fiber. As AI clusters grow larger, communication among accelerators becomes more demanding. Copper remains useful over short distances, but bandwidth, signal integrity and power consumption increasingly favor optical links as systems scale.

AXT manufactures the semiconductor substrates on which customers build many of these compound-semiconductor devices. Its portfolio includes InP, gallium arsenide and germanium wafers for applications where silicon cannot satisfy the required optical or electrical performance. AXT does not sell GPUs, transceivers or finished optical chips. It occupies an earlier and less visible layer of the production chain.

That upstream position has become strategically important because qualified InP supply is concentrated, difficult to expand and increasingly affected by Chinese export controls. Customers are reserving capacity. Wafer prices have risen sharply. Optical manufacturers cannot switch substrate suppliers quickly without qualification work and production risk.

The industrial bottleneck is real.

The investment case remains unfinished.

AXT still has to prove that scarcity can become sustainable pricing power, that pricing power can reach gross margin, and that margin improvement can ultimately create value per share. At the same time, the stock market does not wait for every step to appear in reported earnings. Public research, social-media attention and institutional follow-up can bring future expectations into the current price years before the financial statements fully confirm them.

AXTI must therefore be understood through two separate but connected questions:

How far has the business progressed from scarcity to cash flow?

How far has the stock progressed from discovery to valuation?

The gap between those two paths will determine both the opportunity and the risk.

Key Takeaways

- AI optical infrastructure is increasing demand for indium phosphide (InP), a critical substrate material used in many photonic devices.

- AXT operates upstream in the optical supply chain, but strategic importance does not automatically create shareholder value.

- Coherent’s prepayment agreement provides evidence that qualified InP capacity has become strategically important.

- The central investment question is whether AXT can convert scarcity into pricing power, margin expansion, and durable cash flow.

- Market expectations can move ahead of operating results, creating both upside potential and valuation risk.

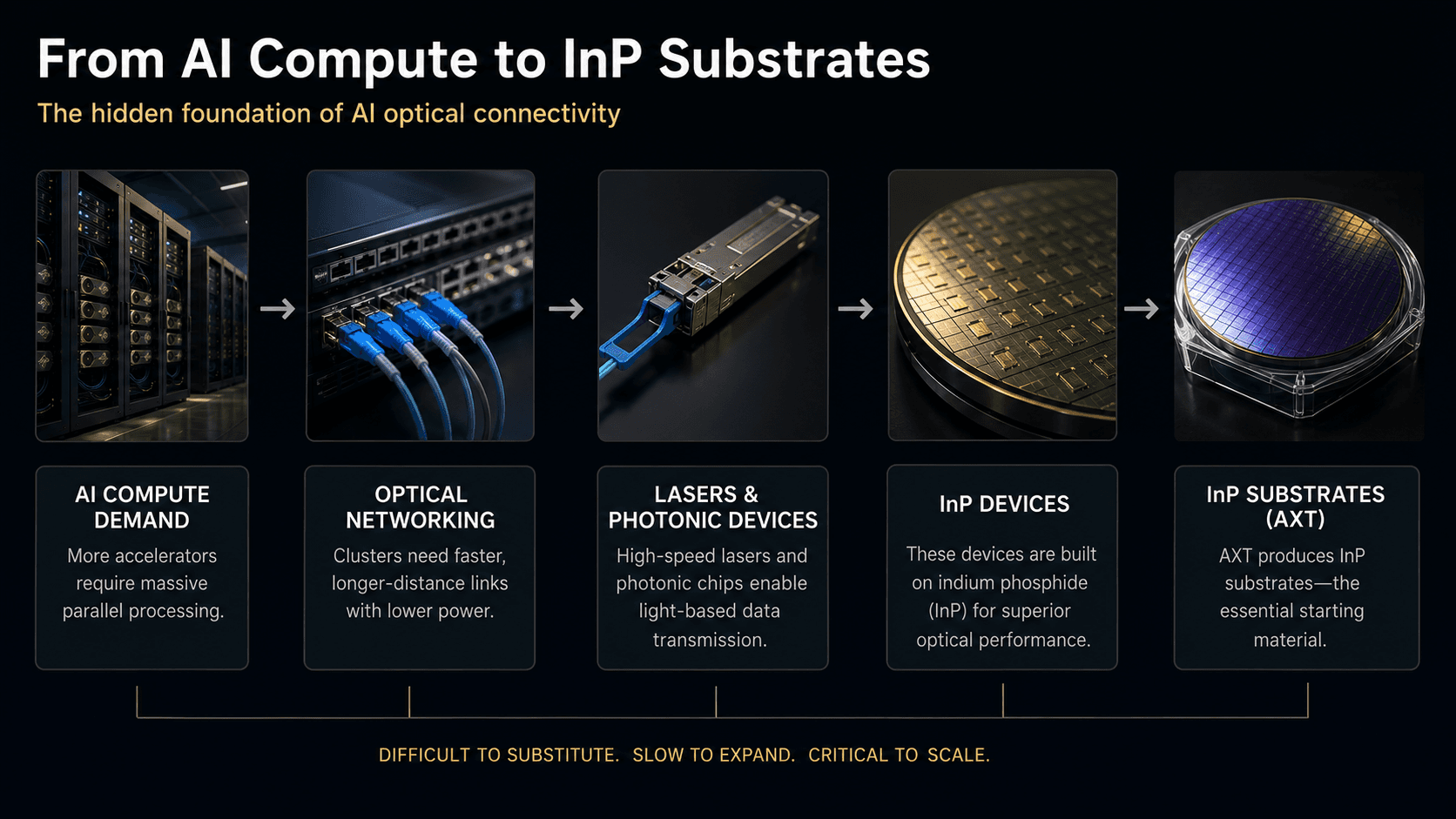

Why AI infrastructure needs indium phosphide

AI data centers do more than perform computation. They must move enormous quantities of data among accelerators, memory, switches and storage. As clusters expand from thousands toward tens of thousands of accelerators, communication becomes a larger part of system cost, power use and performance.

This creates demand for faster optical links.

InP is valuable because it supports devices capable of generating, detecting and manipulating light at wavelengths used in fiber-optic communication. Manufacturers use InP substrates as the crystalline foundation for lasers, photodetectors and other optoelectronic components. The substrate is only one part of the finished device, but its quality affects device performance, production yield and reliability.

The commercial transmission chain is roughly:

AI compute demand → more network traffic → faster optical links → more lasers and photonic devices → greater demand for qualified InP substrates

AXT sits near the beginning of this chain.

That position creates leverage when qualified supply is scarce, because no downstream optical device can be manufactured without suitable starting material. It also creates distance from the final demand signal. AXT does not directly control hyperscaler capital expenditure, network architecture, transceiver pricing or the timing of new data-center deployments.

AI spending must pass through multiple layers before becoming AXT revenue.

That makes AXTI a more complex investment than a simple “AI demand” proxy.

The shortage has moved from forecast to observable behavior

The evidence for InP scarcity has strengthened considerably.

China added InP substrates to its export-control list in February 2025. Because AXT manufactures its wafer substrates in China, its subsidiary must obtain permits before exporting them. The company later received permits for certain customers, but timing remained uncertain, particularly for shipments to the United States. North American revenue consequently fell from approximately 8% of worldwide sales in 2024 to about 2% in 2025. (AXT 2025 Form 10-K)

This is not a conventional shortage caused only by factories running at full capacity. Supply can physically exist while remaining unavailable to specific customers because export approval is uncertain.

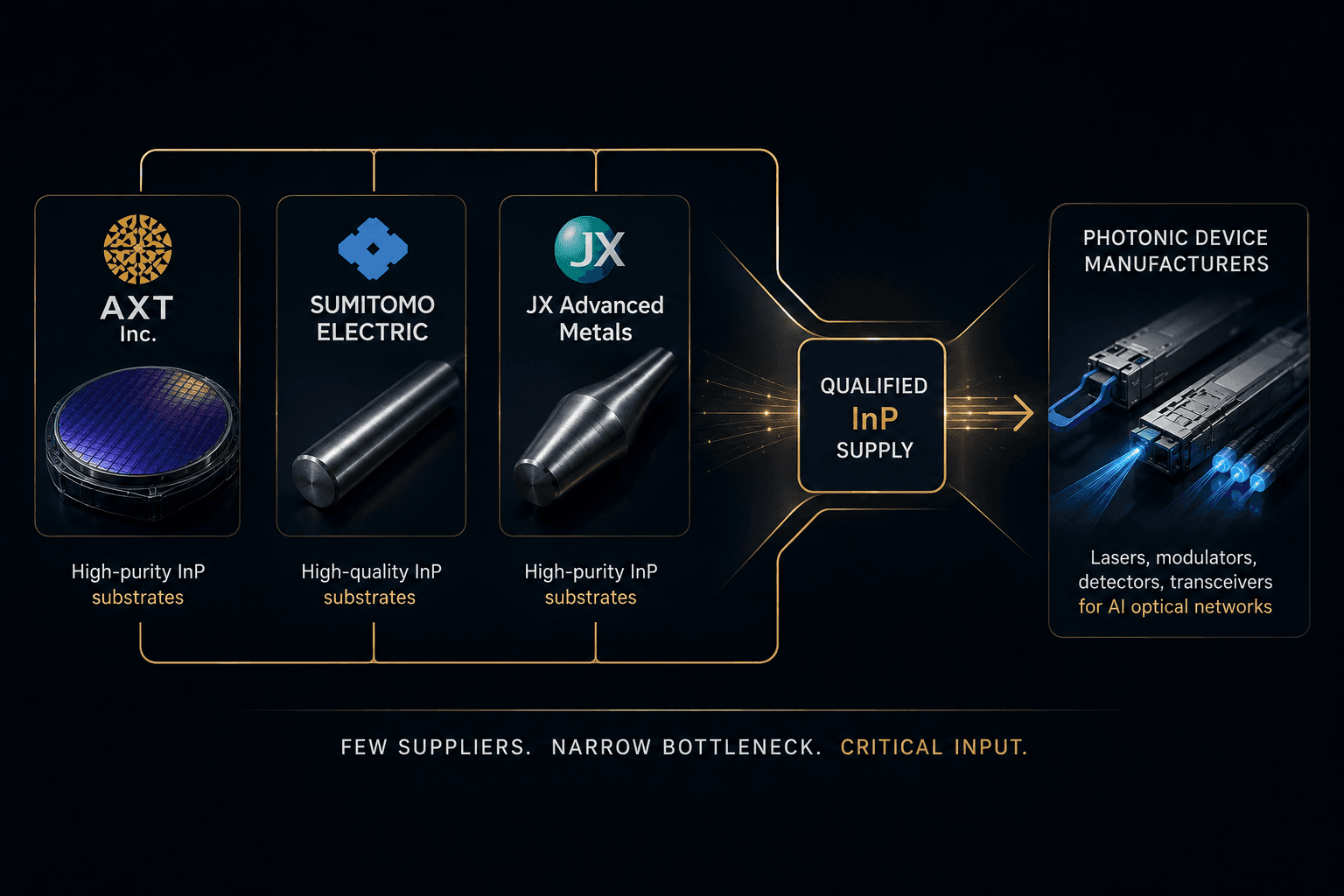

Reuters reported in June 2026 that AXT and Sumitomo Electric together represented close to 80% of global InP substrate manufacturing, with JX Advanced Metals accounting for roughly another 10%. The same investigation reported that the average price of a six-inch InP wafer had risen about 250% to approximately $5,000 after China imposed export restrictions.

Those figures point to a highly concentrated market. They do not establish that AXT has monopoly control.

Sumitomo remains a large and technically capable competitor. JX is an established supplier. Chinese producers are adding capacity, and major optical manufacturers have incentives to expand internal wafer production. New supply, however, cannot appear immediately. Reuters reported that additional plants can take years to build, while new suppliers must pass lengthy customer-qualification processes.

Four conditions are therefore reinforcing one another:

- supplier concentration;

- export friction;

- slow capacity expansion;

- qualification barriers.

That combination supports the claim that InP has become an authentic AI infrastructure bottleneck.

It still does not tell us which participant will retain the resulting profits.

Coherent’s prepayment upgrades the quality of the evidence

The most important recent signal is customer behavior.

Forecasts can be wrong. Industry commentary can become crowded. A customer committing capital to reserve future supply is stronger evidence.

Under a multi-year agreement, Coherent committed approximately $22.3 million in prepayments to support future six-inch InP capacity from AXT. AXT, in turn, committed to expanding production capability over the agreement period. (AXT Form 8-K)

The structure matters more than the headline.

Coherent is effectively helping finance capacity it expects to need later.

That suggests supply security has become important enough to justify tying up capital before the wafers are delivered. The agreement also concerns six-inch substrates, which are difficult to manufacture consistently but can support higher-volume device production when yields are adequate.

The agreement therefore supports three conclusions:

- future InP capacity has strategic value;

- at least one major customer is unwilling to rely solely on ordinary spot procurement;

- the optical industry is preparing for greater production scale.

It proves demand visibility and capacity reservation.

It does not prove exceptional contract economics.

Prepayments will eventually be applied against product deliveries. AXT still bears manufacturing, yield, timing and capacity-execution risks. Contract protections can require funds to be returned if obligations are not met. Agreed pricing may also reduce some exposure to future spot-market increases.

The same contract can therefore validate the bottleneck while limiting part of the supplier’s upside.

Its real quality will be visible in utilization, gross margin and cash flow.

AXT owns qualified capacity, not the entire bottleneck

The most direct answer to the article’s central question is this:

AXT owns meaningful qualified capacity inside a constrained supply chain. It does not own the entire bottleneck.

Its competitive position rests on manufacturing knowledge, crystal quality, customer qualification, production scale and access to upstream materials. These are legitimate industrial advantages.

Compound-semiconductor substrates are difficult to manufacture consistently. Defects in the wafer can reduce customer yield and device reliability. A lower-priced but less consistent substrate may therefore raise the customer’s total cost. Once a customer has qualified a supplier and designed manufacturing processes around its material characteristics, switching introduces risk and delay.

This supports customer stickiness.

Yet AXT’s position remains exposed to several forms of competition.

Sumitomo has scale, technical expertise and vertical integration. JX remains present. Coherent and other large optical companies can expand internal production to reduce dependency. Chinese competitors are adding capacity. High wafer prices and geopolitical uncertainty provide strong incentives for governments and customers to finance alternative supply.

The bottleneck itself can therefore attract the capital that eventually weakens it.

AXT’s opportunity depends on how much economic value it can capture before new supply, vertical integration and customer diversification materially loosen the market.

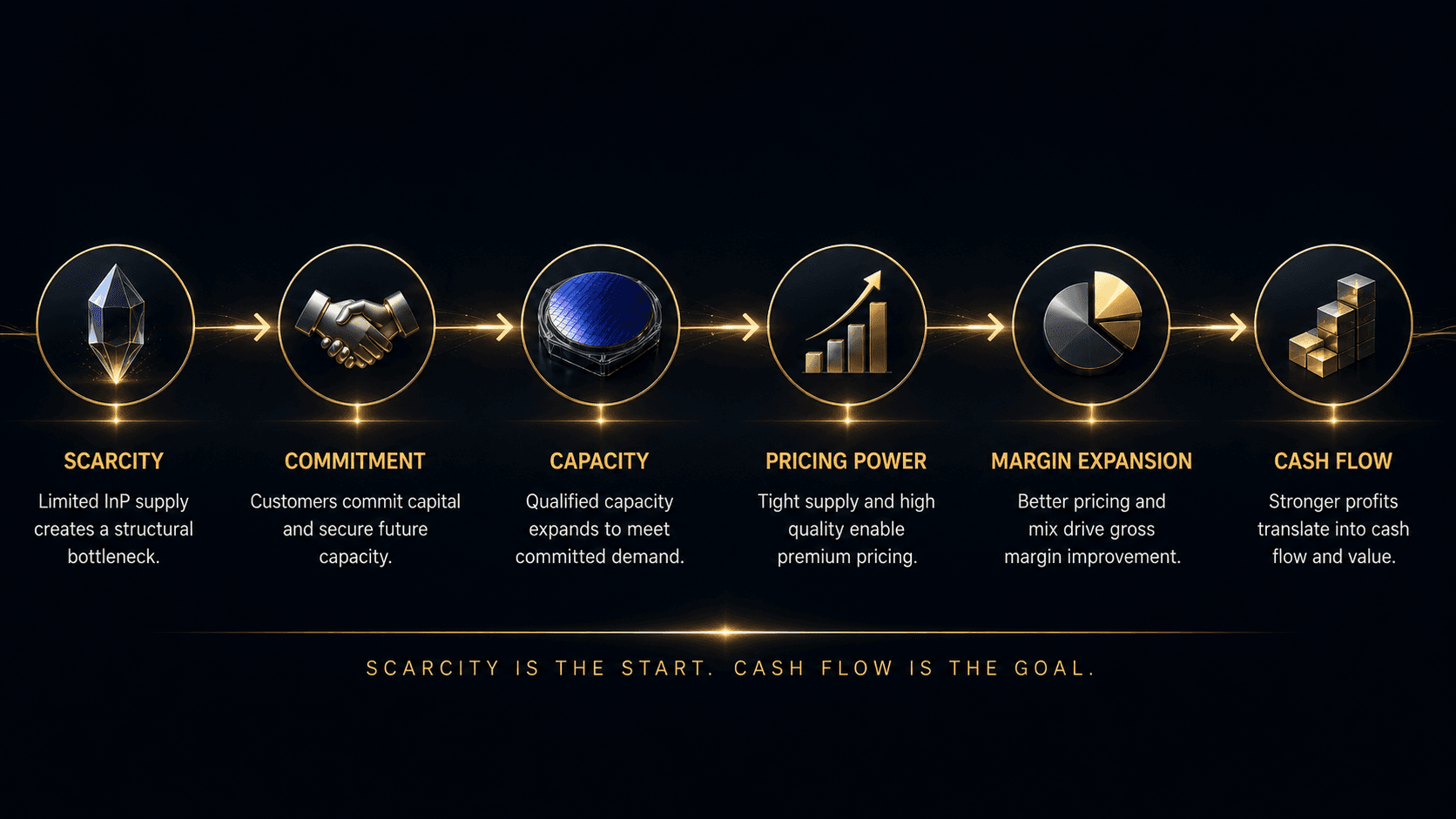

Scarcity is only the first stage of value creation

A shortage can support a compelling narrative without producing equally compelling shareholder economics.

The operating chain is:

Scarcity → customer commitment → qualified capacity → pricing power → gross margin → cash flow → per-share value

Each transition requires separate evidence.

Scarcity can increase customer urgency. Urgency can produce prepayments and long-term agreements. Those agreements can improve demand visibility. They do not automatically raise AXT’s normalized margin.

Higher selling prices may be offset by:

- underutilized factories;

- poor manufacturing yields;

- unfavorable product mix;

- expansion and qualification costs;

- higher raw-material costs;

- contract pricing negotiated before the shortage intensified.

Even revenue and margin growth may fail to create attractive per-share returns if expansion requires substantial equity issuance.

AXT’s financial history demonstrates why this distinction matters.

The company generated approximately $88.5 million of revenue in 2025, down from about $99.4 million in 2024. Its annual gross margin fell to 12.7% from 24.0%, reflecting lower production volume, capacity underutilization and manufacturing variances. (AXT 2025 Form 10-K)

The quarterly path was highly volatile. GAAP gross margin was negative 6.4% in the first quarter of 2025. By the first quarter of 2026, revenue had improved to $26.9 million and gross margin had recovered to 29.6%, although the company still reported a GAAP net loss. (AXT Q1 2026 results)

That rebound shows the operating leverage available when shipment volume and factory utilization improve.

It does not establish a normalized margin.

AXT has demonstrated that the business can produce much stronger profitability under favorable conditions. It has not yet demonstrated that those conditions can be sustained across a full investment cycle.

The market can price the bottleneck before AXT monetizes it

Operating results are only one side of the investment.

The other is market expectation.

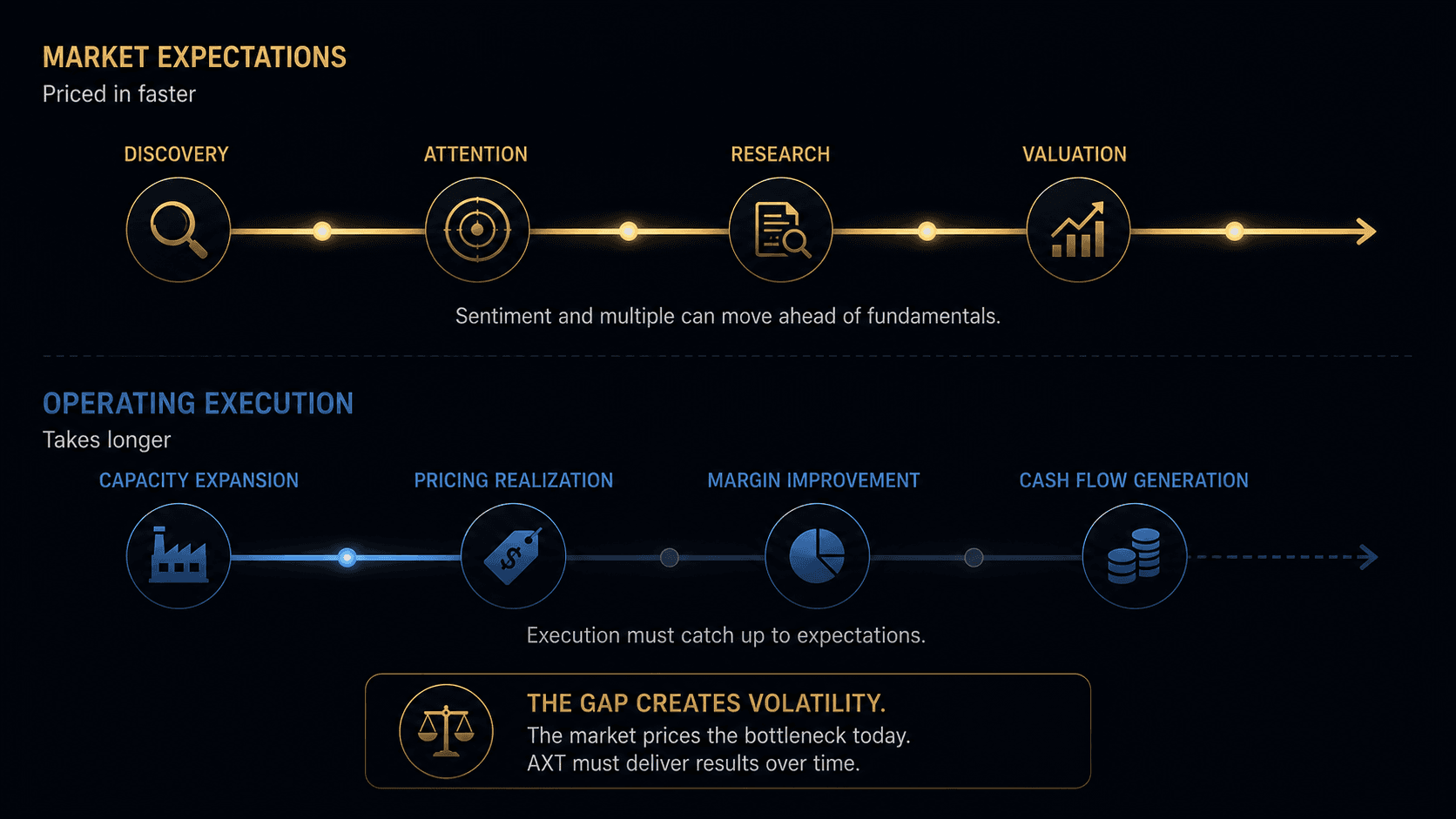

Small-cap stocks do not require large amounts of capital to reprice sharply. When a credible researcher identifies an overlooked supply-chain position, public discussion can rapidly move through several stages:

Discovery → attention → wider research → institutional validation → valuation expansion → operating verification

This process has accelerated in markets where detailed investment research is published openly on X and other platforms.

A researcher may identify a genuine operating variable before sell-side analysts or larger funds have incorporated it into their models. Once the thesis becomes visible, other investors begin validating the evidence. Institutions may study the same supply chain, contact industry participants or wait for public filings that confirm the original thesis.

In a liquid mega-cap stock, this attention may have limited immediate impact.

In a small-cap stock with a narrow trading float, the same discovery process can produce a dramatic price response before reported revenue, earnings or cash flow change meaningfully.

That does not mean the research “creates” the business value.

It accelerates price discovery.

Faster price discovery has two effects. It rewards early recognition of a genuine operating change, but it also brings more future success into the current valuation. The stock can therefore become more fragile even while the underlying industry thesis grows stronger.

AXTI’s current debate is partly explained by this gap.

The market has substantial evidence for:

- InP scarcity;

- supplier concentration;

- export disruption;

- customer efforts to secure supply;

- rapid growth in AI optical connectivity.

It has much less evidence for:

- sustained AXT-specific ASP growth;

- durable normalized margins;

- reliable export access;

- returns on newly financed capacity;

- consistent free cash flow.

The stock market can price the first group while waiting for the second.

Once that happens, a new positive headline may no longer be enough. Each subsequent result must justify expectations already embedded in the price.

Attention can move the stock, but it cannot finish the thesis

It is tempting to divide AXTI’s price action into two opposing explanations.

One view treats the stock as a momentum or meme phenomenon driven primarily by social-media attention. The other treats every price increase as a rational reflection of a strategic supply shortage.

Both are incomplete.

Public research can identify a genuine industrial change and still contribute to extreme short-term volatility. A stock can have legitimate long-term business potential and become temporarily priced for near-perfect execution. A subsequent decline does not automatically invalidate the bottleneck. It may reflect the removal of excess expectations, financing risk, profit-taking or a mismatch between the speed of the stock and the speed of the income statement.

The relevant distinction is between price discovery and value realization.

Price discovery determines when investors begin paying for a possible future.

Value realization determines whether that future arrives.

Over the long term, AXTI’s return will depend on whether the operating economics embedded in today’s valuation become real. In the interim, attention, liquidity and positioning can dominate price action for extended periods.

This is why “the company has value” is not a complete investment conclusion.

Investors also need to know how much of that value has already been anticipated.

Export controls create scarcity while restricting AXT’s ability to benefit

A central tension runs through the thesis.

China’s export controls make InP more difficult for overseas customers to obtain. That can increase the strategic value of AXT’s manufacturing capacity. The same controls can prevent AXT from delivering into the markets where scarcity is most severe.

The company has stated that uncertainty around InP export permits creates anxiety for both AXT and its customers. It expects permits may eventually be granted for U.S. shipments, but timing remains outside management’s control. (AXT Q1 2026 results)

This creates several possible paths.

A favorable outcome would combine broader permit approvals with elevated demand and stronger pricing. AXT could convert backlog into shipments while customers remain focused on supply security.

A less favorable outcome would leave customer demand intact but shipments delayed. In that case, reported demand would overstate realizable revenue.

A prolonged restriction could also accelerate the qualification of Japanese suppliers, internal production and alternative Chinese sources. AXT would have helped demonstrate the strategic importance of InP while encouraging customers to reduce their dependence on it.

Export-control headlines therefore cannot be interpreted mechanically.

The operating impact depends on four variables:

- which customers receive permits;

- how quickly approval arrives;

- what volume can be shipped;

- what pricing and margin AXT earns on those shipments.

Capacity expansion is the economic test

Scarcity gives AXT a reason to expand.

It does not guarantee that the expansion will earn an attractive return.

The company raised substantial equity capital to support InP capacity, research and development, working capital and other corporate needs. Customer prepayments provide another source of financing. The availability of capital reduces the immediate funding constraint but increases the importance of capital discipline.

A successful expansion requires several things to occur together:

- equipment must be installed on schedule;

- six-inch wafers must reach acceptable quality;

- customer qualification must proceed without major delays;

- yields must protect gross margin;

- export permits must allow delivery;

- demand must remain strong when capacity becomes available;

- pricing must compensate for execution and geopolitical risk.

The result will be shaped by timing.

AXT does not need scarcity to remain permanent. It needs scarcity to last long enough for the company to build qualified capacity, fill that capacity and earn adequate returns before alternative supply materially changes the market.

If demand remains strong and utilization rises, fixed manufacturing costs can be spread over more wafers. The sharp recovery in gross margin between early 2025 and early 2026 illustrates that leverage.

If qualification, permits or yields lag, new capacity can become expensive idle infrastructure.

The factory buildout is therefore not a secondary detail.

It is where the strategic thesis becomes a financial one.

Long-term contracts improve visibility but may redistribute bargaining power

Coherent’s prepayment improves AXT’s demand visibility, but the relationship also highlights customer concentration and bargaining power.

A large optical manufacturer can offer several benefits:

- minimum purchase commitments;

- financing support;

- more predictable utilization;

- technical collaboration;

- validation that attracts other customers.

It can also negotiate:

- agreed pricing;

- capacity protections;

- refund rights;

- delivery obligations;

- terms that shift part of the economic upside toward the customer.

This creates a trade-off between volume security and pricing optionality.

A supplier can lock in future demand and sacrifice some exposure to rising spot prices. It can preserve pricing flexibility and accept greater uncertainty. Without the confidential economics of the agreement, the public cannot know exactly where AXT sits on that spectrum.

The contract should therefore be interpreted carefully.

It confirms customer urgency.

It does not disclose who captures the majority of the value.

Gross margin will provide the answer more reliably than the contract headline.

The absolute market remains smaller than the narrative surrounding it

AXT can hold a strategically important market share while still serving a specialized addressable market.

InP substrates sit far upstream from finished optical modules. The wafer is essential, but it represents only a fraction of the value of the completed component and an even smaller fraction of the total data-center system. AXT’s 2025 revenue remained below $100 million.

That small base creates room for rapid percentage growth. It also makes the stock sensitive to assumptions about market size, share and future pricing.

The transition from valuable niche supplier to durable compounder depends on several unresolved questions:

- How quickly does InP content grow in future optical architectures?

- Do six-inch wafers become a high-volume production standard?

- How much supply remains external rather than vertically integrated?

- How much of the shortage-induced price increase reaches AXT?

- How much share can AXT retain as new suppliers scale?

- Can the company generate attractive returns after financing expansion?

A narrow market can produce excellent economics when suppliers remain disciplined and customers have few alternatives.

It can also become cyclical when high prices trigger simultaneous capacity expansion.

Current evidence supports the scarcity thesis more strongly than it supports long-term supply discipline.

Operating progress and expectation progress are no longer aligned

AXTI now needs to be assessed on two separate tracks.

Operating Framework

| Stage | Current assessment |

|---|---|

| InP scarcity | Strong evidence |

| Customer commitment | Strong evidence |

| Qualified capacity expansion | Underway |

| AXT-specific pricing power | Emerging, not proven |

| Sustained margin expansion | Early evidence |

| Free-cash-flow conversion | Not proven |

| Durable per-share value | Not proven |

Expectation Framework

| Stage | Current assessment |

|---|---|

| Strategic-position discovery | Complete |

| Public attention | High |

| Broader investor research | Accelerating |

| Institutional interest | Likely increasing |

| Valuation expansion | Already occurred materially |

| Operating verification | Still in progress |

The mismatch is the central source of volatility.

The market may be several stages ahead of the financial statements. That creates large upside when operating evidence catches up quickly and equally large downside when execution takes longer than expected.

A strong industry thesis therefore does not remove price risk.

It raises the standard of proof.

What matters next

The next decisive evidence will come from operating variables rather than additional declarations that AI optical demand is strong.

InP revenue and shipment volume will show whether demand and backlog are converting into recognized sales.

Export permits by customer and geography will determine whether AXT can serve the markets where supply is tightest.

Average selling prices will reveal whether reported industry scarcity is reaching AXT’s own revenue mix.

Gross margin will show whether pricing, utilization and yield are improving together.

Six-inch wafer qualification and production yield will determine whether the Coherent-supported expansion becomes commercially productive.

Additional prepayments or long-term contracts would indicate whether capacity reservation is becoming a broader industry behavior.

Operating cash flow and capital expenditure will show whether growth can finance itself.

Share count and future financing will determine whether total company growth also becomes per-share growth.

These indicators complete the two frameworks.

The operating chain is:

Scarcity → commitment → qualified capacity → pricing → margin → cash flow

The expectation chain is:

Discovery → attention → valuation → verification

AXT has made clear progress through the early stages of both.

The financial outcome still depends on the later ones.

Conclusion

Indium phosphide has moved from an obscure semiconductor material to a visible constraint in the AI optical supply chain.

Export controls have disrupted availability. Global supply is concentrated. Prices have reportedly risen sharply. Qualification cycles slow substitution. A major photonics customer has committed capital to reserve future AXT capacity. These facts establish that the bottleneck is more than a social-media narrative.

Public research helped the market recognize that position earlier and faster. In a small-cap stock, that discovery process can produce a dramatic valuation change long before reported earnings fully reflect the thesis.

The resulting volatility does not by itself prove that AXTI is a meme stock, nor does the strategic importance of InP prove that every valuation is justified.

AXT now faces a more demanding test.

It must expand qualified capacity, secure export approvals, preserve pricing, stabilize yields and convert shipments into margin and cash flow. It must do so while competitors add supply, customers pursue internal production and investors have already begun paying for future success.

The bottleneck is real.

The market has discovered it.

The remaining question is whether AXT’s economics can catch up with the expectations that discovery created.

Frequently Asked Questions

What does AXT Inc. do?

AXT manufactures compound semiconductor substrates, including indium phosphide (InP), gallium arsenide (GaAs), and germanium wafers used in photonics and semiconductor applications.

Why is indium phosphide important for AI infrastructure?

Indium phosphide is used as a substrate material for high-speed optical devices, including lasers and photonic components that support increasing AI data-center networking requirements.

Is AXT an AI chip company?

No. AXT does not design AI processors or optical transceivers. It supplies semiconductor substrate materials used by companies manufacturing photonic devices.

Why are investors watching AXT?

Investors are evaluating whether InP supply constraints can translate into sustainable pricing power, higher margins, and long-term shareholder value.

Is AXT the only supplier of indium phosphide substrates?

No. The market includes other suppliers such as Sumitomo Electric and JX Advanced Metals. However, qualified InP substrate supply is concentrated among a limited number of producers.

What should investors monitor for AXT?

Key operating variables include InP shipment growth, customer agreements, capacity expansion, gross margin improvement, export approvals, and free cash flow generation.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | AXT Inc. Annual Report Form 10-K | SEC | 2026 | SEC | Revenue, gross margin, manufacturing structure and export-control impact. |

| 2 | AXT First Quarter 2026 Financial Results | AXT Inc. | 2026 | Company IR | Revenue recovery and gross-margin improvement. |

| 3 | AXT-Tongmei and Coherent Supply Agreement | SEC | 2026 | SEC | Customer prepayment and future InP capacity reservation. |

| 4 | China’s control over indium phosphide exports threatens AI data centre rollout | Reuters | 2026 | Other | Supply concentration, export restrictions, wafer pricing and industry impact. |

| 5 | Compound semiconductor industry analysis | Industry sources | Various | Other | InP substrate market structure and competition. |

| 6 | Coherent optical communications commentary | Coherent Inc. | 2026 | Company commentary | Optical-demand environment and the strategic importance of qualified InP supply. |

Primary filings and company results support AXT-specific operating and financial claims. Reuters supports the reported market-concentration, pricing and export-control context. Broader industry references are included without invented URLs.

Related Reading

Sivers Semiconductors (SIVE): When Does an AI Photonics Story Become a Business?

The market is already pricing a future in co-packaged optics, external laser sources and InP manufacturing. The harder question is whether qualification, capacity, yield and customer orders can turn that future into per-share cash flow.

NVIDIA’s Next Bottleneck Isn’t GPUs. It’s Data Movement.

Why AI factories are moving from copper to optical connectivity — and which suppliers deserve deeper research

CPO Isn’t Dead. The Timeline Is.

After the CPO Selloff: The Real Story Is Not the Death of Optical Stocks, but a Repricing of AI Infrastructure’s Transition Layer

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for informational and research purposes only and does not constitute investment advice. Small-cap semiconductor companies can involve substantial execution, geopolitical, liquidity and dilution risks.

Comments