Open USD is not simply another dollar stablecoin. Its real proposition is to rewrite who gets paid. Instead of allowing the issuer to retain most of the interest generated by reserve assets, OUSD intends to pass nearly all of that economics to the payment companies, exchanges, wallets and merchant platforms that drive adoption. That makes it less a new coin than a direct challenge to the profit architecture behind Circle Internet Group’s USD Coin (USDC).

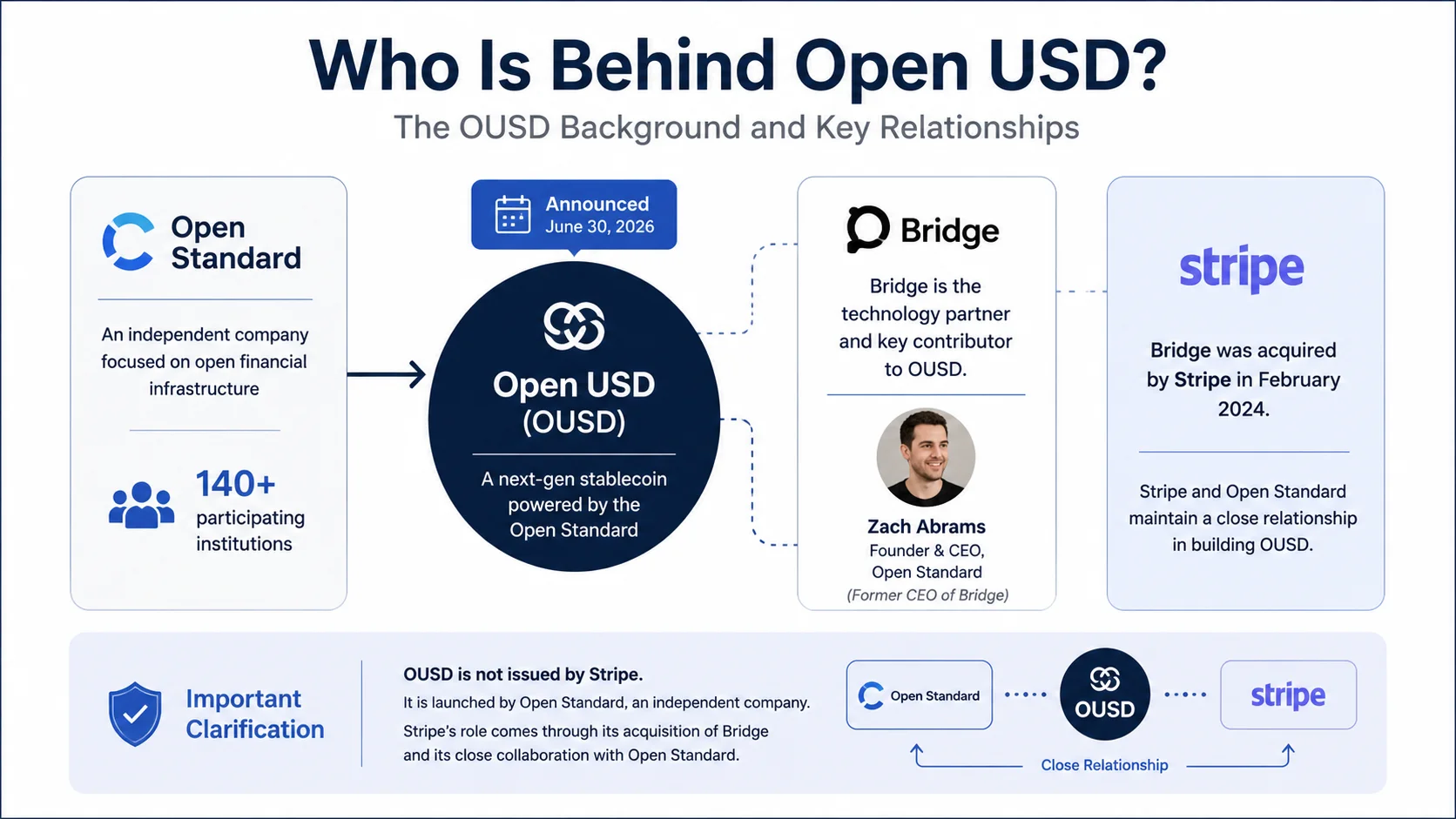

On June 30, 2026, Open Standard announced Open USD, or OUSD, a planned dollar-backed stablecoin designed for global payments and financial activity. The project is expected to launch later in 2026 and has not yet produced the circulating supply, redemption history or stress-tested liquidity that would allow investors to judge it as a functioning financial asset. For now, OUSD is a business model supported by an unusually powerful distribution coalition.

OUSD is being developed by Open Standard, which describes itself as an independent company governed with participation from its partners. Its founding chief executive is Zach Abrams, a co-founder of stablecoin infrastructure company Bridge. Stripe completed its acquisition of Bridge in February 2025, creating a close strategic connection between OUSD’s leadership and one of the world’s largest payment platforms. Open Standard’s launch materials, however, do not establish that Stripe is the issuer of OUSD, and the distinction should remain explicit.

More than 140 companies have been associated with the initiative, including payment networks, banks, exchanges, technology companies and merchant platforms. The most important strategic question is not how many logos appear in the launch coalition, but how many partners ultimately integrate OUSD into live products, make it a default settlement asset and move real customer balances onto the network.

Key Takeaways

- OUSD’s main innovation is a different allocation of reserve income, not a new source of stablecoin yield.

- The first competitive pressure may fall on Circle’s margins before it appears in USDC market share.

- Payment platforms such as Stripe could benefit because they control merchant distribution and may also participate in reserve economics.

The hidden engine of the stablecoin business

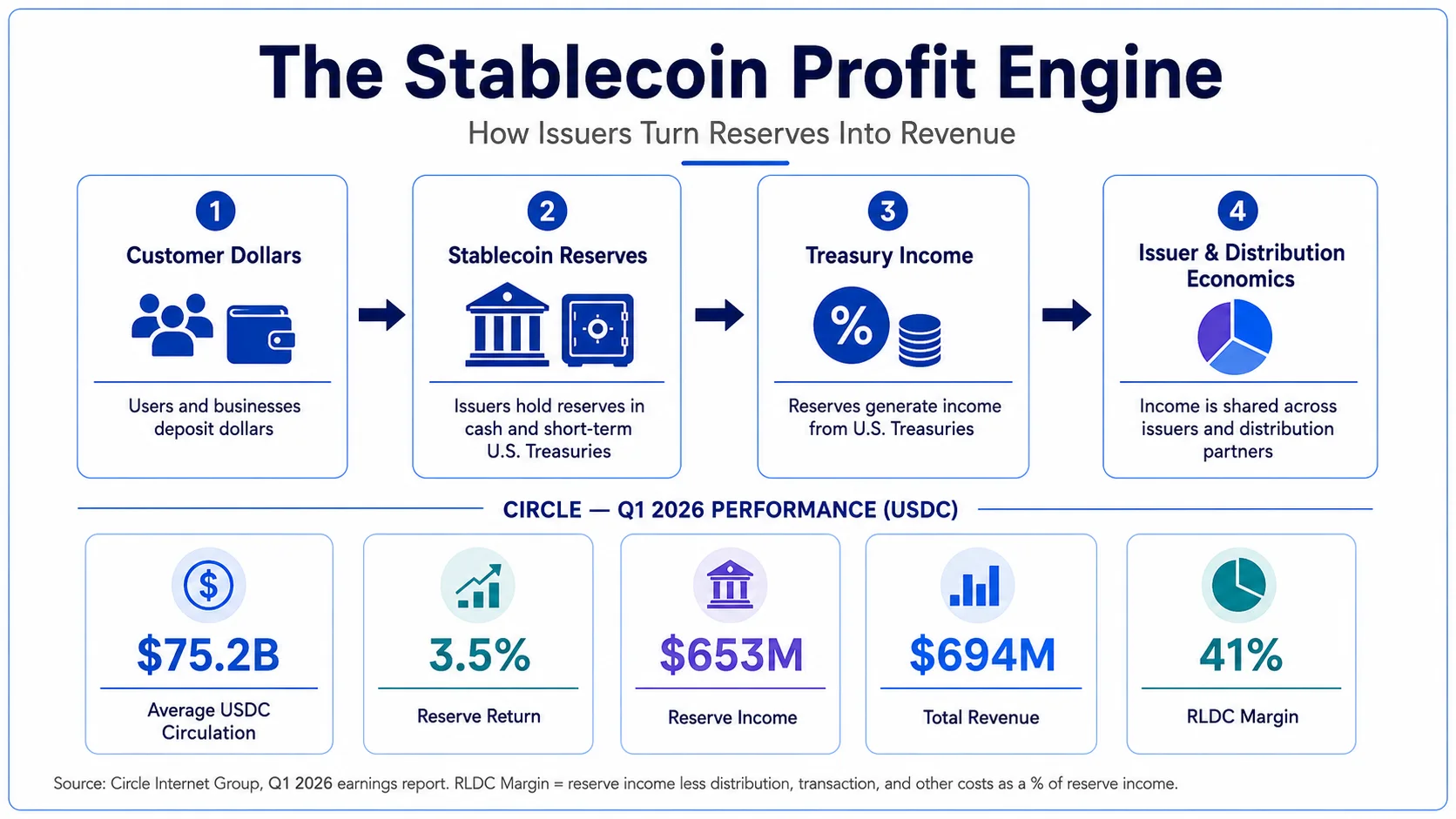

The economics of a fiat-backed stablecoin are straightforward. A customer hands an issuer one dollar, receives one digital dollar, and the issuer invests the reserve in cash, Treasury bills, repurchase agreements or similar liquid assets. The customer normally receives no direct interest, while the reserve continues to earn a return for the issuer.

The basic revenue equation is:

Reserve income = average stablecoin balance × reserve yield

This makes stablecoin issuance primarily a balance-sheet business, not a transaction-volume business. A token may move between wallets many times, but those transfers do not automatically multiply the issuer’s reserve income. What matters is how much money remains inside the system and for how long.

Circle’s first-quarter 2026 results show how powerful this model can be. Average USDC circulation reached $75.2 billion, while the reserve return rate was 3.5%. Circle generated $653 million of reserve income during the quarter and reported $694 million of total revenue and reserve income. Revenue less distribution costs was $287 million, producing an RLDC margin of 41%. Circle also reported $407 million of distribution, transaction and other costs, reflecting the high cost of obtaining and maintaining distribution.

These figures reveal that stablecoin distribution is already a major economic claim on reserve income. Issuers must pay exchanges, platforms and other partners for liquidity, integrations, customer balances and default placement inside financial applications.

OUSD takes that existing arrangement and makes it the centre of the product. Open Standard says businesses will be able to mint and redeem OUSD without issuance or redemption fees, while reserve earnings—after a management fee and operating expenses—are intended to flow primarily to participating distribution partners.

OUSD is therefore not creating a new source of income. It is reallocating an existing one.

Under the conventional structure, the issuer earns the reserve yield and negotiates bilateral payments with selected distributors. Under the OUSD structure, reserve income is presented from the outset as a shared economic pool for the companies that create adoption. Payment platforms, wallets, exchanges and merchant networks are no longer merely customers of the issuer; they become participants in the economics of the reserves.

At a 3.5% reserve yield, every $10 billion of average OUSD balances would produce roughly $350 million in annual gross reserve income. At $50 billion, the figure would be approximately $1.75 billion. The actual amount available to partners would be lower after management, custody, compliance and operating expenses, but the scale explains why distribution companies may find the model attractive.

It also exposes OUSD’s dependence on interest rates. At a 1% reserve yield, the same $10 billion balance would produce only $100 million annually. As our analysis of the tension between monetary policy and the U.S. fiscal system explains, the rate environment can shift the value of short-term dollar assets materially. OUSD must eventually demonstrate that it offers structural payment and distribution advantages, rather than relying only on a subsidy funded by a high-rate Treasury market.

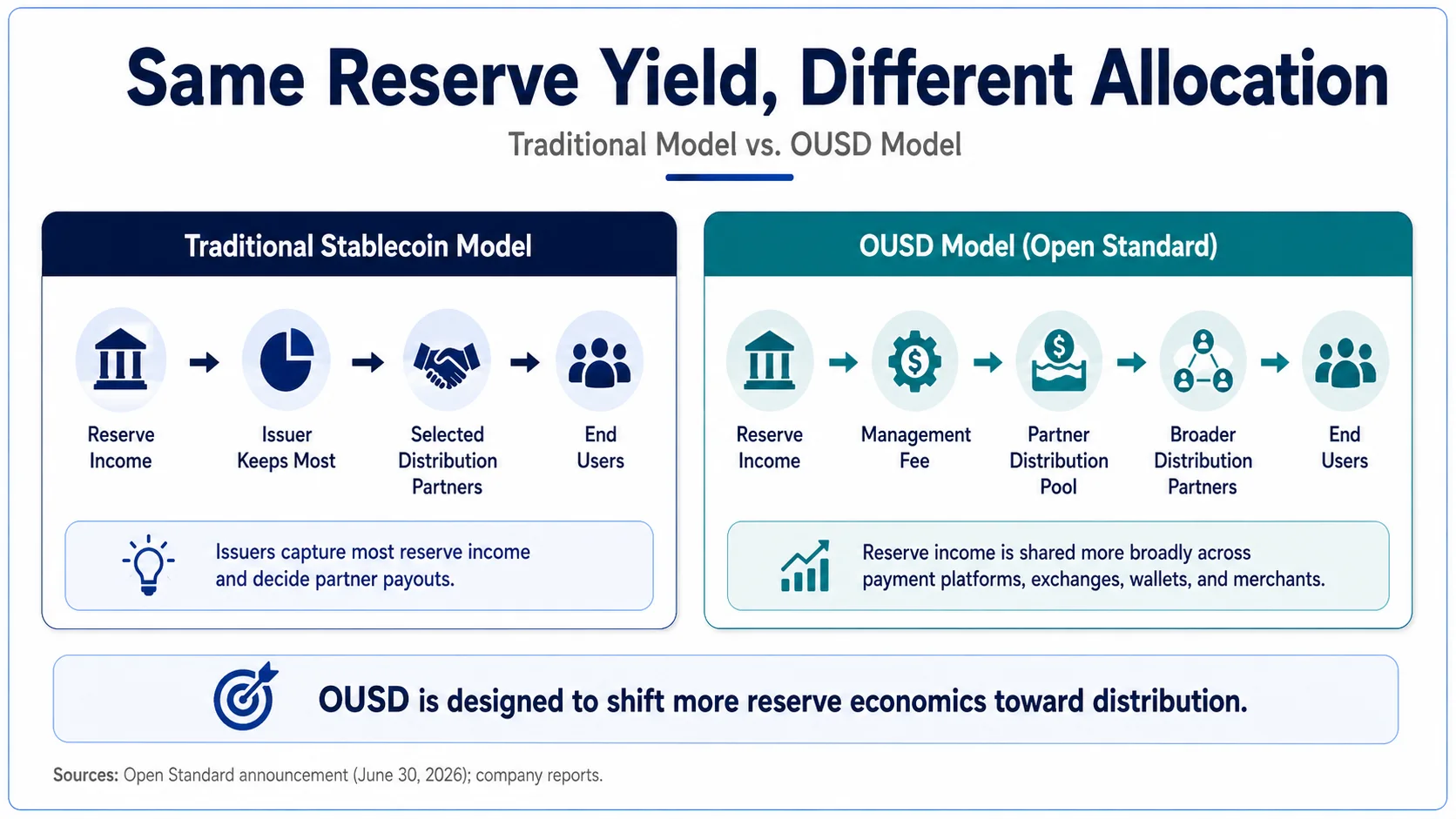

Same reserve yield, different allocation

The central difference between OUSD and a conventional stablecoin is not the source of the yield. Both models rely on reserves invested in cash and short-term government securities. The difference is the order in which the economics are distributed.

In the conventional model, the issuer captures the reserve income and then decides how much to pay selected distribution partners. In the OUSD model, a management fee is deducted first and a larger portion of the remaining economics is intended to flow through a partner distribution pool.

That distinction matters because platforms are rarely loyal to a settlement asset for ideological reasons. They care about liquidity, regulatory treatment, integration costs and economic participation. A payment platform that receives reserve income from OUSD can retain it as profit, use it to reduce merchant pricing, subsidise cross-border transactions or reward customers for holding balances.

Why USDC faces more pressure than USDT

OUSD will compete with both USDC and USDT, but the pressure is unlikely to be evenly distributed.

Tether’s strength lies in global crypto liquidity, exchange depth and demand for offshore digital dollars. OUSD’s initial coalition is strongest in regulated payments, merchant acquiring, enterprise finance and US-facing financial infrastructure. That may limit USDT’s expansion into mainstream corporate payments, but it is unlikely to displace Tether’s established global liquidity network in the near term.

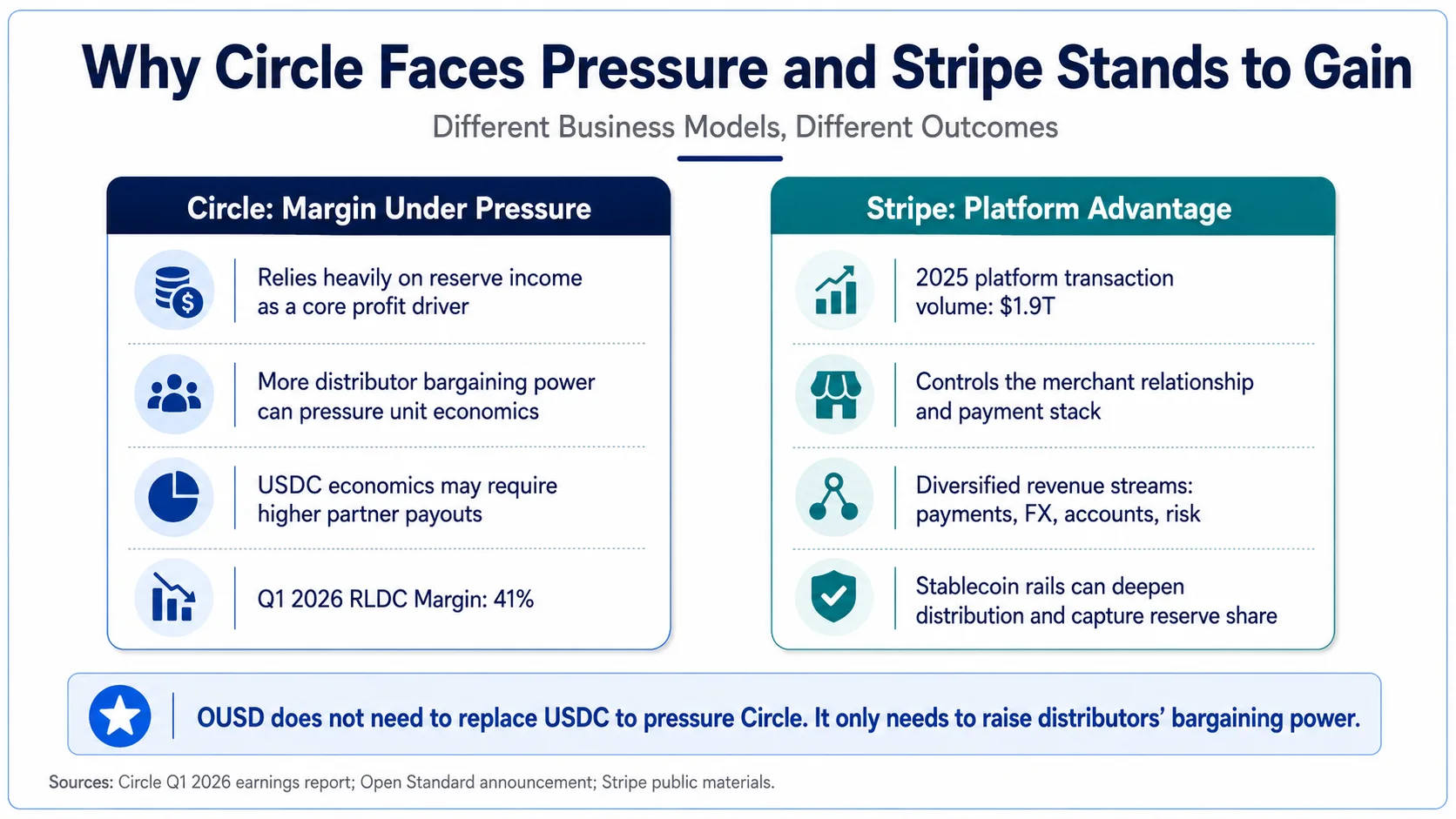

USDC is more directly exposed because it serves many of the same customers OUSD is targeting: financial institutions, payment companies, exchanges, wallets, fintech platforms and corporate treasury departments. More importantly, Circle’s earnings remain heavily tied to reserve income.

OUSD does not need to take a large amount of USDC circulation immediately to hurt Circle’s economics. It only needs to give major distributors a credible alternative.

If a platform can receive a larger share of reserve income by promoting OUSD, it can keep that income, use it to lower merchant fees or subsidise customer adoption. Circle would then face a difficult choice: increase the share of USDC economics paid to distribution partners, or preserve its margin and risk losing incremental balances and activity.

That is why the first phase of competition is likely to be a margin war rather than a market-cap war. Circle may retain most of USDC’s circulation while earning less on every dollar outstanding. Only later, if OUSD establishes reliable redemptions, deep liquidity and durable merchant adoption, would the conflict move from profit allocation to market share.

USDC still has meaningful advantages. It already has established liquidity, institutional integrations, blockchain support and a history of large-scale redemptions. OUSD has none of those operating records yet. Its coalition provides potential distribution, not proven monetary credibility.

Stripe may be the biggest winner

It is tempting to describe stablecoins as a threat to Stripe, PayPal, Visa or Mastercard. That framing confuses a settlement asset with a complete payment service.

A payment transaction involves far more than moving money from one account to another. Merchants require checkout software, authentication, fraud detection, currency conversion, refunds, chargebacks, reconciliation, tax tools and access to local payment methods. Stablecoins can reduce some settlement and cross-border costs, but they do not automatically replace those services.

Stripe is therefore more likely to absorb stablecoins than be displaced by them.

Through Bridge, Stripe has built capabilities around stablecoin issuance infrastructure, wallets, orchestration and fiat conversion. If OUSD becomes widely used inside Stripe’s ecosystem, Stripe could control both the customer-facing layer and part of the underlying reserve economics. It may continue earning payment-processing, software, account, foreign-exchange and risk-management revenue while also receiving a share of stablecoin reserve income.

Stripe reported that businesses running on its platform generated $1.9 trillion in total volume in 2025. That figure does not represent future OUSD volume, but it illustrates the scale of the merchant distribution layer Stripe already controls.

This creates several strategic options. Stripe could retain reserve distributions as additional margin, use them to offer more competitive pricing to large merchants, or subsidise stablecoin-based cross-border payments. In every case, the reserve economics strengthen the platform that owns the merchant relationship.

This is the deeper shift OUSD represents. As stablecoins become more standardised, the scarce asset may no longer be the ability to issue a digital dollar. The scarce assets will be customers, merchant integrations, liquidity and default distribution.

Issuers supply the asset. Platforms control the flow.

The inclusion of major card networks and financial institutions in the OUSD coalition points in the same direction. Traditional payment networks may lose some economics associated with cross-border settlement and funding delays, but they still control merchant acceptance, fraud systems, tokenised credentials, credit authorisation and consumer protection. Rather than being eliminated by stablecoins, they may incorporate stablecoin settlement into their back-end infrastructure while preserving the customer-facing network. That possibility fits the broader role of regulated stablecoins as extensions of dollar infrastructure, not simply as substitutes for existing finance.

The pressure on PayPal falls mainly on PYUSD

PayPal’s most valuable assets are its consumer wallet, Venmo, merchant relationships, checkout brand, credit products and dispute-management infrastructure. OUSD does not replace those capabilities.

The more vulnerable part of PayPal’s strategy is PayPal USD (PYUSD), its proprietary stablecoin. PYUSD is tied to the PayPal and Paxos ecosystem, while OUSD is designed as a common asset supported by payment networks, banks, exchanges, fintech companies and merchant platforms.

That leaves PayPal with a strategic question: why should a merchant or developer hold a PayPal-specific stablecoin when a shared asset may offer wider distribution and a more attractive reserve-sharing model?

PayPal can still answer that question through its existing user network, rewards, checkout integration and consumer experience. It could also support multiple stablecoins rather than insisting on PYUSD exclusivity. The likely impact of OUSD is therefore not the disappearance of PayPal, but greater pressure on the logic of maintaining a closed, company-branded settlement asset.

The real test begins after launch

OUSD currently has an exceptional list of partners, but a partner logo is not the same as production activity. Joining a consortium is not the same as completing an integration, making a stablecoin the default option, transferring customer balances or supporting liquidity during a market shock.

Several critical terms remain unclear in public materials. These include the final reserve composition, the exact management fee, the partner-allocation formula, redemption eligibility and the final governance structure. Nor has OUSD demonstrated how quickly large redemptions will be processed or how reserve income will be divided among platforms that contribute balances, payment volume and liquidity in different ways.

The distribution formula is particularly important. If rewards are based mainly on balances, large exchanges and wallets could dominate the economics. If rewards are based on transaction volume, participants may have an incentive to manufacture activity. If they are based on merchant adoption, the largest payment platforms may capture most of the pool.

“Shared economics” sounds neutral, but the formula will determine where the money actually goes.

There is also no guarantee that reserve income will reach merchants or consumers. Moving the yield from a stablecoin issuer to large payment platforms does not necessarily democratise the industry. It may replace an issuer oligopoly with a distributor oligopoly.

The most useful indicators after launch will be OUSD’s average circulating balance, redemption performance, secondary-market liquidity, number of partners with live integrations, share of payment-platform stablecoin activity and the percentage of reserve income actually distributed or passed through to customers.

OUSD’s real experiment is whether Treasury income can purchase lasting distribution. If the project converts its coalition into tens of billions of dollars of durable balances, Circle may be forced to surrender more of USDC’s reserve economics and payment platforms will gain greater leverage over stablecoin issuers. If rates fall, liquidity remains shallow or partners decline to move meaningful customer funds, OUSD may remain a compelling announcement rather than a functioning monetary network.

The most important stablecoin question is no longer simply which token has the largest supply. It is who controls the customer relationship, who selects the default settlement asset and who ultimately captures the interest generated by the reserves.

OUSD is a major attempt to answer all three questions in favour of distribution.

Frequently Asked Questions

What is Open USD?

Open USD, or OUSD, is a planned dollar-backed stablecoin announced by Open Standard on June 30, 2026. It is designed for payments and financial infrastructure, with a model intended to share much of the reserve economics with participating distribution partners.

Is OUSD issued by Stripe?

Public launch materials describe OUSD as a project of Open Standard, not as a stablecoin issued directly by Stripe. Stripe’s connection comes through its acquisition of Bridge and its broader stablecoin infrastructure strategy.

How does OUSD make money?

Like other fiat-backed stablecoins, OUSD is expected to hold reserves in cash and liquid short-term assets such as US Treasury securities. Those reserves generate interest. The main difference is how that income is intended to be distributed.

Why could OUSD pressure Circle?

Circle depends heavily on reserve income from USDC. If major payment and distribution platforms can earn a larger share of reserve economics through OUSD, Circle may need to increase partner payments to defend USDC distribution.

Does OUSD threaten Stripe or PayPal?

OUSD is more likely to become a back-end settlement asset inside payment platforms than to replace their merchant, fraud, checkout and account services. The more direct pressure on PayPal may fall on PYUSD rather than on PayPal’s entire payment network.

What should investors watch after OUSD launches?

The most important indicators will be average circulating balances, redemption performance, liquidity, live partner integrations, distribution costs and the percentage of reserve income passed to partners or customers.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Introducing Open USD | Open Standard | 2026-06-30 | Company announcement | Supports the OUSD announcement, planned launch, partner model, distribution economics, and coalition structure. |

| 2 | Stripe Completes Bridge Acquisition | Stripe | 2025-02-04 | Company announcement | Supports Stripe’s completed acquisition of Bridge and Zach Abrams’s role as a Bridge co-founder. |

| 3 | Circle Reports First Quarter 2026 Results | Circle Internet Group | 2026-05-11 | Company earnings release | Supports average USDC circulation of $75.2 billion, a 3.5% reserve return rate, $653 million of reserve income, $694 million of total revenue and reserve income, $407 million of distribution and other costs, and a 41% RLDC margin. |

| 4 | Stripe’s 2025 Annual Letter | Stripe | 2026 | Company annual letter | Supports that businesses running on Stripe generated $1.9 trillion in total volume in 2025. |

Confirmed facts are drawn from the primary sources below. Statements about adoption, competitive pressure, partner behavior, and future economics are forward-looking analysis rather than operating results for OUSD.

Related Reading

America Is Rewriting Dollar Credibility

The U.S. is rebuilding dollar credibility through strong-dollar policy, Treasury demand, Fed uncertainty, stablecoins, AI infrastructure, and gold reserves.

The U.S. Economy and U.S. Fiscal System Are Demanding Opposite Monetary Policies

What broke on June 5 was not AI valuation, but the market’s faith in endless Quantitative Easing

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice. OUSD is a planned product, and its final structure, economics, regulatory treatment, and adoption may differ from current announcements.

Comments