Editor's note: This article was originally published on Substack on June 6, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

June 5 looked like a cross-asset selloff.

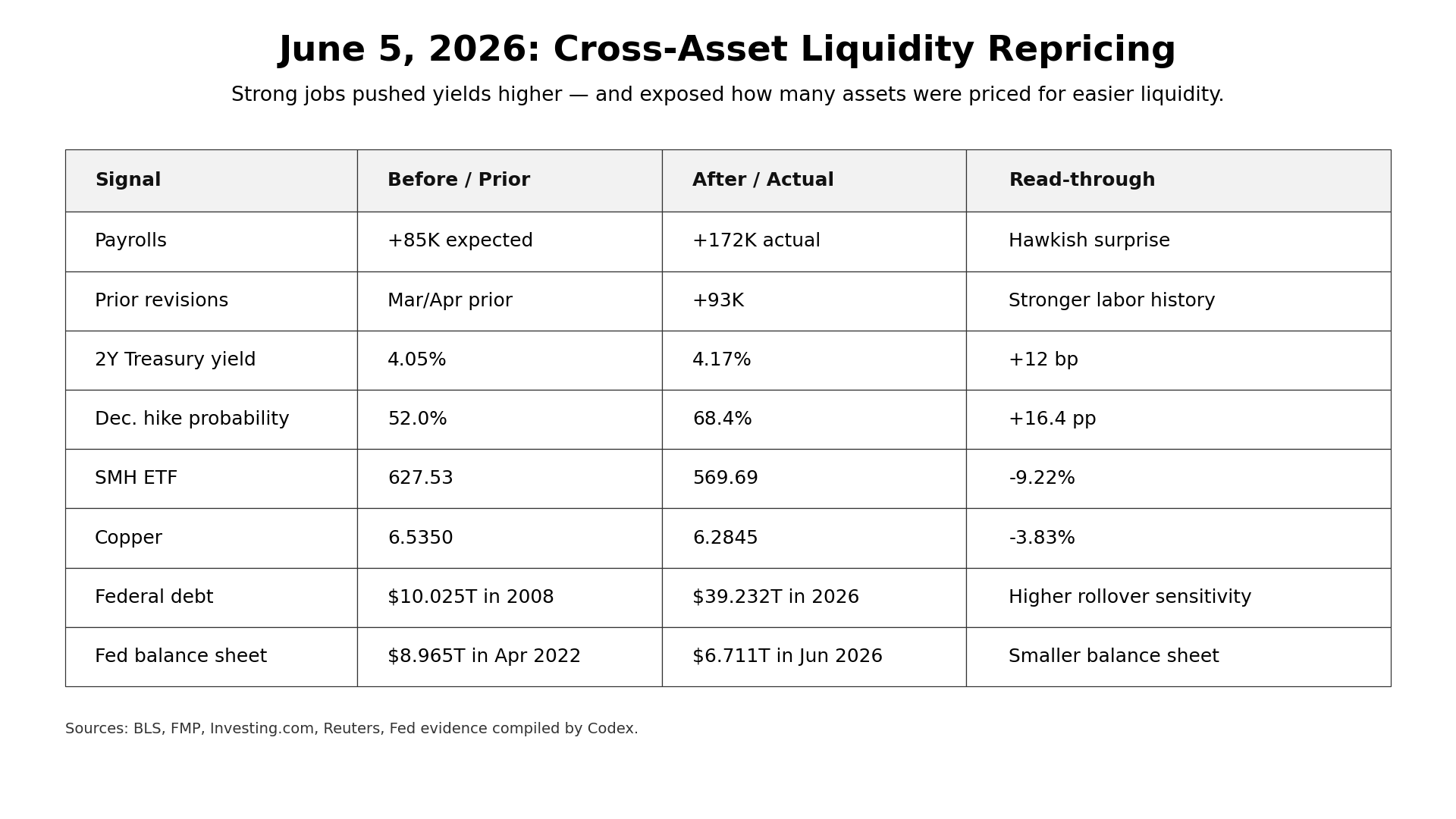

The visible trigger was the May U.S. Nonfarm Payrolls report. The U.S. economy added 172,000 jobs, far above the market expectation of roughly 85,000. March and April payrolls were revised upward by a combined 93,000. The unemployment rate held at 4.3%.

This was not recessionary data. It was strong labor-market data.

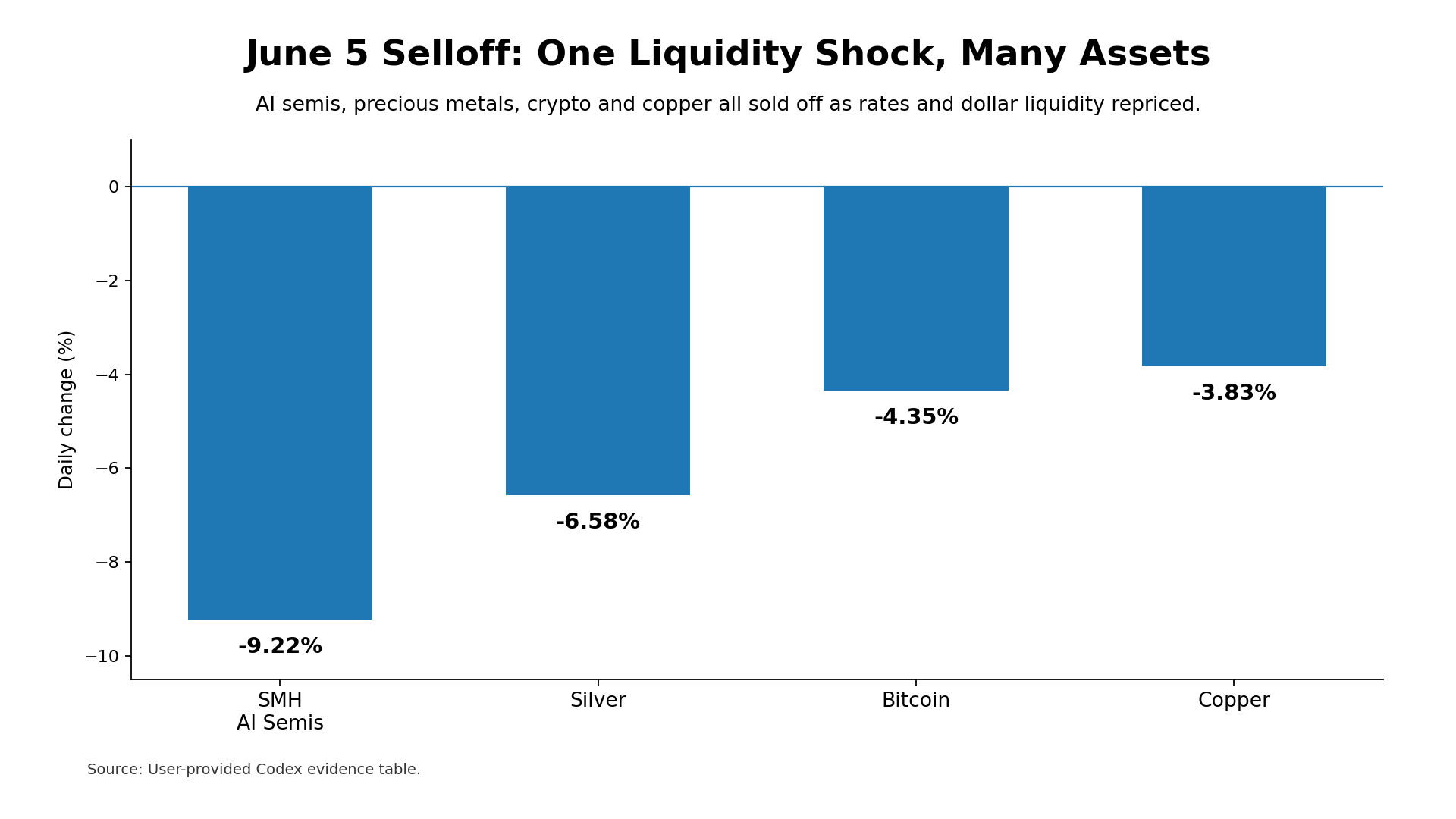

Yet the market did not respond as if stronger employment meant stronger risk assets. Instead, the two-year Treasury yield rose from 4.05% to 4.17%. The market-implied probability of a December rate hike increased from 52.0% to 68.4%. The VanEck Semiconductor ETF, SMH, fell 9.22%. Silver dropped 6.58%. Copper fell 3.83%. Bitcoin declined 4.35%.

This was not an isolated equity selloff. It was not just an AI correction. It was not simply a gold pullback. It was a repricing of rates, the dollar, liquidity, and the market’s embedded assumption that the Federal Reserve will eventually return to balance-sheet expansion whenever financial conditions tighten.

The real problem was not that the jobs report was too strong.

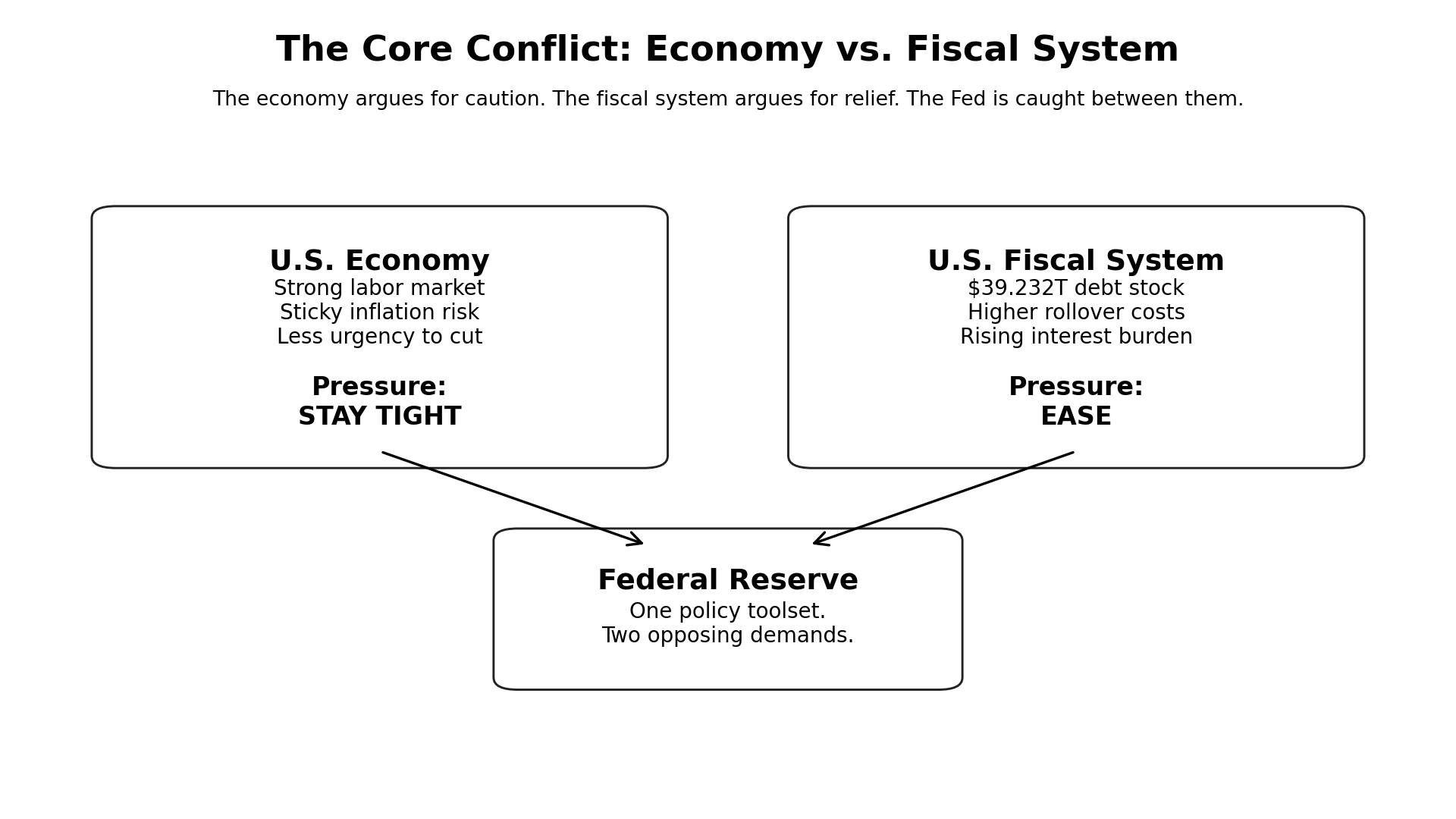

The real problem was that the U.S. economy is still strong enough to make immediate rate cuts difficult, while the U.S. fiscal system has become so debt-heavy that it increasingly needs lower rates.

That is the structural contradiction markets began to reprice on June 5.

1. For the past two decades, the U.S. economy, Treasury, and Federal Reserve were on the same side

To understand why June 5 mattered, we need to go back to the previous crisis playbook.

After the 2008 financial crisis, the U.S. economy needed lower rates. The private sector was deleveraging, the banking system was impaired, and the housing market had collapsed. The U.S. Treasury also needed lower rates because deficits were expanding and the government had to stabilize the financial system. The Federal Reserve’s response was clear: cut rates, launch Quantitative Easing, and expand the balance sheet.

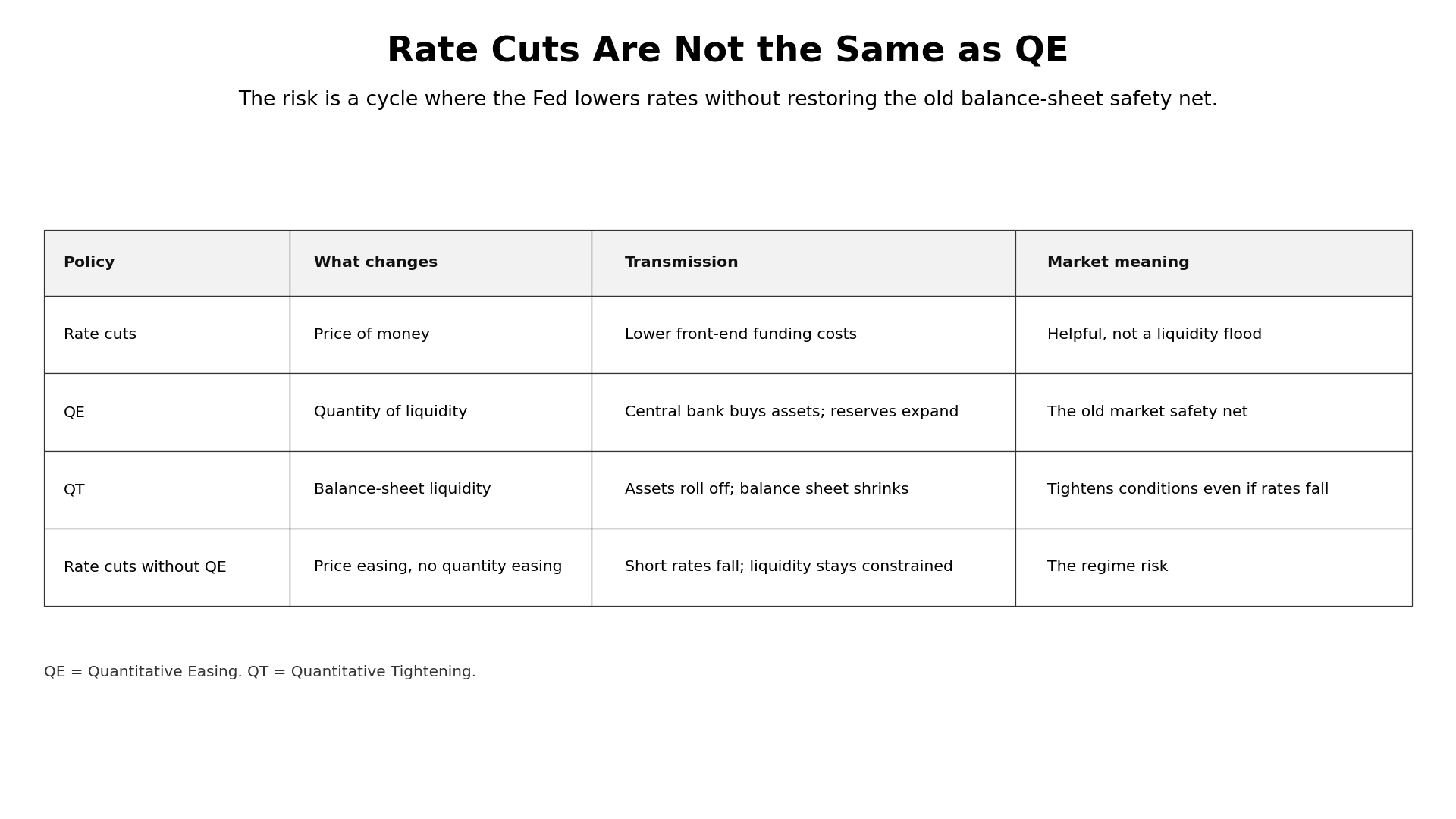

Quantitative Easing, or QE, is a policy in which a central bank creates reserves to buy financial assets such as Treasury bonds or mortgage-backed securities. In plain English, it is not just lowering the price of money through interest rates; it is increasing the quantity of liquidity in the financial system through the central bank’s balance sheet.

After the 2020 pandemic shock, the same playbook returned. The economy stopped, fiscal spending exploded, companies needed liquidity, households needed support, and markets needed a backstop. Once again, the economy, Treasury, and Federal Reserve were aligned: expand the balance sheet, suppress funding costs, and push the crisis into the future.

This created one of the strongest market beliefs of the past fifteen years:

Whenever the U.S. system comes under pressure, the Fed will eventually inject liquidity.

Asset pricing became built not only on earnings, cash flows, and productivity, but also on the Federal Reserve’s reaction function.

Gold, Bitcoin, technology stocks, real estate, private equity, and venture capital all carried different stories, but they benefited from the same underlying regime: expanding dollar liquidity.

Gold’s story was currency debasement. Bitcoin’s story was distrust of fiat money. Growth stocks’ story was lower discount rates applied to distant future cash flows. Real estate’s story was cheaper long-term financing. Private equity’s story was valuation expansion through cheap leverage.

These were different assets on the surface. But underneath, they shared one macro assumption:

The Fed would eventually rescue the system.

What broke on June 5 was not simply AI valuation.

What cracked was the market’s confidence that the QE-era playbook would always return.

2. The U.S. in 2026 is no longer the U.S. of 2008

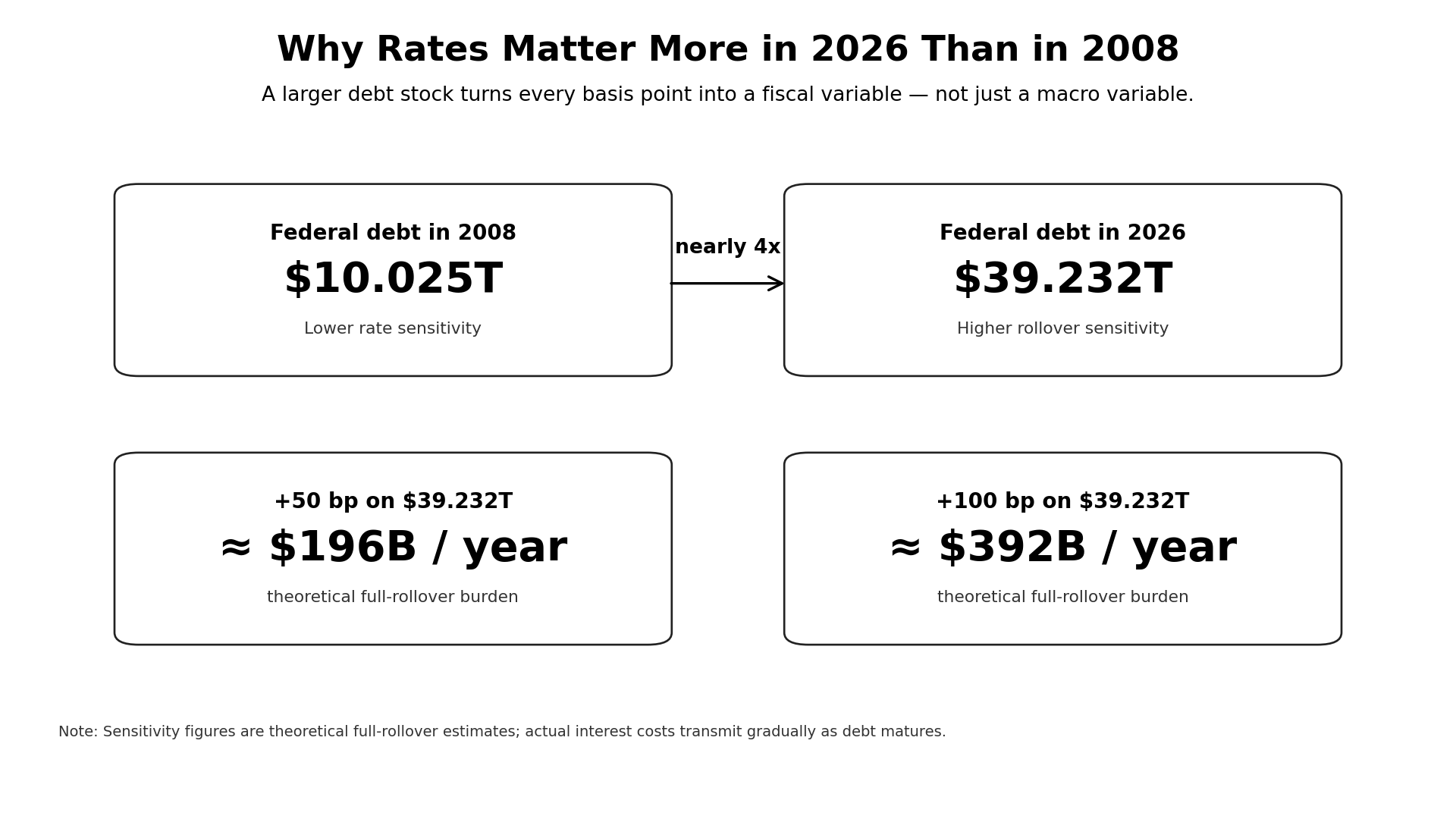

In 2008, U.S. federal debt was roughly $10 trillion. By June 2026, it had reached approximately $39.2 trillion.

The debt stock has nearly quadrupled.

But U.S. GDP has not quadrupled. Federal revenue has not quadrupled. The productive base of the economy has not grown at the same pace as the debt burden.

That changes the meaning of interest rates.

If the average funding cost on $39.2 trillion of debt rises by 50 basis points, the theoretical annualized interest burden increases by roughly $196 billion. If it rises by 100 basis points, the theoretical burden increases by roughly $392 billion.

In reality, the entire debt stock does not reprice overnight. Treasury debt matures over time, so the burden is transmitted gradually. But the direction is clear: the larger the debt stock, the more dangerous every additional basis point becomes.

This is the key difference between 2008 and 2026.

In 2008, lower rates were primarily about saving the economy.

In 2026, lower rates increasingly look like they are needed to save the fiscal system.

Those are not the same thing.

Saving the economy is a cyclical policy problem.

Saving the fiscal system is a credibility problem.

When monetary policy starts shifting from managing the business cycle to protecting debt sustainability, markets must reassess the credibility of the currency itself.

That is why a strong payroll report became bad news. A strong labor market means the Fed has less justification to cut quickly. Fewer rate cuts mean the U.S. government must continue financing an enormous debt load at elevated rates.

The stronger the economy looks, the more pressure it places on the fiscal system.

That is the true mechanism behind “good news is bad news.”

3. Copper mattered more than the semiconductor crash

Many investors focused on semiconductors. SMH fell 9.22%, which was obviously painful. But from a macro perspective, the more important signal was copper.

Copper fell 3.83%.

That move carried more information than the semiconductor selloff.

If the market were only worried about overvaluation in one AI stock, copper should not have fallen sharply. If investors were merely repricing Nvidia, Broadcom, or the semiconductor supply chain, copper should not have been sold this aggressively.

Copper is not an AI concept stock. Copper does not tell stories. Copper reflects expectations for future capital expenditure and real-world physical investment.

Over the past two years, the bullish copper narrative has been driven by three forces: AI data centers, grid modernization, and the energy transition. GPU servers require power. Data centers require transformers. Grid expansion requires transmission equipment. Storage systems and renewable infrastructure require metals.

If the market truly believed the U.S. economy was simply stronger, AI capital expenditure would keep accelerating, and data-center construction would continue without interruption, copper should have benefited.

Instead, copper fell.

That means the market was not trading the disappearance of demand.

It was trading the rise of funding costs.

The deeper message from copper is that capital markets are beginning to understand that the next constraint on AI infrastructure may not be GPUs, electricity, land, or supply chains. It may be the cost of capital.

The AI conversation is still dominated by chips, compute, optical modules, liquid cooling, power, and data centers. But if the ten-year Treasury yield remains above 4.5%, or moves higher, every long-duration capital expenditure plan must be recalculated.

A $100 billion data-center buildout is not the same project at a 3% funding cost as it is at a 5% funding cost. The discount rate is not a minor input in a spreadsheet. It can determine whether an entire investment cycle remains financeable.

So copper’s decline was not a rejection of AI demand.

It was a repricing of the capital cost required to turn AI demand into physical infrastructure.

That was the deeper signal.

4. Gold and Bitcoin did not fall because their narratives died. They fell because the liquidity premium was repriced.

Gold’s decline can be explained mechanically by higher real rates and a stronger dollar. That explanation is correct, but incomplete.

Gold had already been correcting from its previous highs for several months. The June 5 move was not the beginning of a new story. It was the acceleration of an existing adjustment under a stronger-rate shock.

The long-term gold thesis remains tied to dollar credibility, fiscal deficits, and central-bank reserve diversification. But short-term gold pricing still has to pass through real rates and the dollar. If the market starts pricing “higher for longer” again, or even a renewed probability of rate hikes, a non-yielding asset comes under pressure.

But the deeper issue is that gold’s previous rise was not only about inflation. It was also about the belief that the U.S. would ultimately solve its debt problem through monetary expansion.

Gold is not merely an inflation hedge. It is a hedge against the gradual dilution of dollar credibility.

If investors begin to believe that the future Fed may not return easily to QE, and may instead defend a smaller balance sheet even while cutting rates, gold faces a short-term contradiction: the long-term fiscal problem remains, but the near-term pace of dollar debasement may be slower than previously priced.

That is why gold can have a long-term logic and still fall sharply in the short term.

Bitcoin faces a similar issue.

Bitcoin is often described as digital gold. But on June 5, it traded less like a pure monetary alternative and more like a high-beta liquidity asset. Its decline was not caused by the collapse of the decentralization narrative. It was caused by the repricing of dollar liquidity.

When cash yields rise, the dollar strengthens, and leveraged capital retreats, Bitcoin comes under pressure.

Gold and Bitcoin appear to be anti-dollar assets, but in the short run both depend on one shared condition: the market must believe that future dollars will become cheaper and more abundant.

On June 5, what was marked down was not the long-term thesis for gold or Bitcoin.

It was the premium attached to the belief that the Fed will always return to liquidity expansion.

5. The central contradiction: the U.S. economy needs higher rates, while the U.S. fiscal system needs lower rates

This is the core judgment of the article:

The U.S. economy and the U.S. fiscal system are now demanding opposite monetary policies.

From an economic standpoint, the case for aggressive rate cuts is weak. Payrolls rose by 172,000. Unemployment stayed at 4.3%. Prior months were revised higher by 93,000. The labor market is not collapsing. As long as employment remains firm and wage pressure does not fully disappear, inflation risk cannot be declared dead.

If the Fed only looks at the real economy, it has reason to stay cautious.

But from a fiscal standpoint, the U.S. increasingly needs lower rates.

Federal debt has risen from roughly $10 trillion in 2008 to approximately $39.2 trillion in 2026. The larger the debt stock becomes, the less interest rates behave like a normal macro variable. They become a fiscal survival variable.

This is the structural trap:

A stronger economy makes rate cuts harder.

Fewer rate cuts make the fiscal burden heavier.

A heavier fiscal burden makes the market worry that debt will eventually need to be monetized.

But if debt monetization becomes too obvious, dollar credibility weakens.

The United States is no longer facing only the traditional Fed tradeoff between inflation and employment. It is facing a deeper triangle: economic stability, fiscal sustainability, and dollar credibility.

It is very difficult to maximize all three at once.

QE allowed the U.S. to suppress this contradiction for years. When the economy weakened, the Fed injected liquidity. When Treasury borrowing rose, rates stayed low. When asset prices fell, the balance sheet expanded.

But every round of balance-sheet expansion had a cost. It made markets more dependent on the next rescue. It made fiscal policy more reliant on monetary accommodation. It made investors more comfortable pricing risk assets on the assumption that the Fed would eventually reflate the system.

That model can last for a long time.

But it is not costless.

June 5 was the market’s first serious reminder that the marginal cost of the old model is rising.

6. Why Kevin Warsh matters: not as the cause of the selloff, but as a regime variable

It is important to be precise.

The June 5 selloff was not caused by Kevin Warsh.

The market was trading the jobs report, higher rates, a stronger dollar, and liquidity repricing. The data also shows that the market was not pricing “rate cuts without QE” that day. It was pricing fewer cuts and a higher probability of renewed tightening.

So Warsh should not be treated as the direct cause of the selloff.

But Warsh matters because he represents a possible shift in policy philosophy.

The public evidence supports several points: Warsh has favored a smaller Fed balance sheet, questioned the normalization of QE, criticized the Fed’s large asset holdings, and discussed the problem of mortgage-backed securities on the Fed’s balance sheet. However, there is no public evidence that he has formally announced a specific “rate cuts plus Quantitative Tightening” framework.

Quantitative Tightening, or QT, is the reverse of QE. It means the central bank allows assets to mature without reinvesting proceeds, or otherwise reduces the size of its balance sheet, thereby withdrawing liquidity from the financial system.

That distinction matters.

The confirmed evidence is that Warsh has a more restrictive view of the Fed’s balance sheet.

The inference is that a Warsh-led Fed might be more willing to cut rates without returning to aggressive balance-sheet expansion.

Those are not the same claim.

But markets do not wait for policies to be formally announced before repricing possible regimes. What matters is not one specific Warsh quote. What matters is the philosophy he represents: should the Fed continue using its balance sheet as the default backstop for asset markets?

If the Powell-era instinct was to provide enough liquidity when the system came under stress, the Warsh-era question may be different: can the Fed adjust interest rates while keeping the balance sheet constrained?

That difference is enormous.

Rate cuts are a price tool.

QE is a quantity tool.

Rate cuts change the price of money. QE changes the amount of liquidity and reserves in the system.

For years, markets treated them as one package: rate cuts meant liquidity expansion, liquidity expansion meant higher asset prices.

But if the next cycle brings rate cuts without QE, the asset-price response may be very different.

Short-term rates can fall without long-term rates collapsing.

The banking system can remain liquidity-constrained even as the policy rate declines.

The Fed can protect the system without protecting valuation multiples.

That is the real regime risk.

7. The U.S. may not want simple rate cuts. It may want to rebuild the yield curve.

From the perspective of the U.S. fiscal system and the dollar system, “rate cuts without QE” is not necessarily contradictory.

Lower front-end rates can reduce pressure on banks, corporations, and Treasury bill financing. They can also signal policy flexibility to the White House and the market.

But refusing to restart QE, or keeping the balance sheet smaller, can serve another purpose: it prevents the dollar’s credibility from being further diluted through permanent monetary expansion.

It allows long-term Treasury yields to be priced by the market rather than suppressed by the Fed’s balance sheet.

The U.S. Treasury does not simply need low rates across the entire curve. It needs global capital to keep buying U.S. debt.

If the Fed becomes the permanent buyer of last resort, Treasury auctions can be stabilized in the short term, but long-term dollar credibility can erode. If long-dated Treasuries offer a higher term premium, pension funds, insurers, foreign central banks, and global savings pools may have more incentive to absorb supply.

That is the logic of a steeper yield curve.

Lower the front end to give the economy and fiscal system breathing room.

Allow the long end to offer enough yield to attract capital.

Keep the balance sheet constrained to signal that the dollar will not be diluted without limit.

This is not an easy policy mix. It can easily break markets if liquidity becomes too tight. But it fits the strategic problem the U.S. now faces: America needs lower rates to ease the debt burden, but it cannot let the world believe the dollar is being endlessly monetized.

This is no longer just monetary policy.

It is a negotiation between debt financing, dollar credibility, and global capital flows.

8. Who benefits, and who pays?

If the U.S. enters a “rate cuts without QE” regime, the most important market change will not be the level of the policy rate. It will be the hierarchy of assets.

The dollar may benefit in the early phase. A smaller balance sheet, or a constrained balance sheet, implies tighter dollar supply. In the global dollar funding system, a scarcer dollar is a stronger dollar. That is difficult for highly indebted emerging markets.

Long-term Treasuries are more complicated. If QT raises term premium, long bonds may suffer initially. But if the market believes the Fed is restoring inflation credibility and defending dollar quality, long-duration Treasuries may eventually benefit. The key question is not whether the Fed cuts rates. The key question is whether the market believes the fiscal path is credible.

Gold may remain under pressure in the short term but retain long-term value. If dollar credibility is repaired, the currency-debasement trade cools. But if the fiscal problem ultimately proves unsustainable, gold remains a hedge against policy failure.

Bitcoin is more vulnerable in the near term. Its biggest threat may not be regulation. It may be a rate-cutting cycle without QE. Bitcoin’s explosive upside over the past decade was partly powered by liquidity expansion, not just scarcity.

AI stocks will diverge. Companies with real cash flows, pricing power, and capital efficiency can survive. Companies dependent on low discount rates, far-distant earnings, and continuous financing will be repriced. AI as an industry will not disappear because rates rise. But AI valuations will have to move from narrative discounting to cash-flow proof.

Copper and silver will remain volatile. They sit between two forces: real demand from AI infrastructure, grids, and energy transition on one side; and higher funding costs suppressing capital expenditure on the other. Strong demand does not automatically mean strong prices. Demand must be financed before it can become construction.

That is the lesson of June 5.

Assets did not fall according to their stories.

They fell according to their liquidity sensitivity.

9. Final judgment: markets are not afraid of a strong economy. They are afraid of losing the old playbook.

The June 5 payroll report was not historically extraordinary. Strong jobs, higher yields, and risk-asset weakness have happened many times before.

What makes this episode different is that U.S. debt has changed the meaning of higher rates.

In a low-debt world, higher rates often signal economic strength.

In a high-debt world, higher rates also signal fiscal stress.

That is why today’s market can no longer simply celebrate strong growth. If stronger growth keeps rates high, it can pressure fiscal sustainability, valuation multiples, and the global dollar funding system.

That is why gold, silver, copper, Bitcoin, and AI stocks fell together.

They are not the same asset class.

But they shared the same macro assumption:

Future dollars would be cheaper.

The Fed would eventually ease.

The balance sheet would eventually expand again.

June 5 forced the market to mark down that assumption.

Warsh matters not because he caused the selloff, but because he may represent the beginning of a post-QE regime: a Fed that can cut rates without aggressively expanding its balance sheet; a Fed that can protect the system without automatically rescuing asset prices; a Fed that may have to manage the business cycle while also defending dollar credibility.

For the past fifteen years, the market’s deepest belief was simple:

The Fed will eventually inject liquidity.

The next decade may ask a much harder question:

If the Fed no longer returns easily to QE, which assets still deserve premium valuations?

That is what cracked on June 5.

Not AI.

Not gold.

Not Bitcoin.

The market’s faith in the eternal return of QE.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-06 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments