Key Takeaways

- June CPI materially reduced the probability of an immediate Fed rate increase, but it did not create a new low-rate regime.

- Treasury refinancing, fiscal deficits and debt supply may keep long-term yields elevated even if short-term policy rates stabilize.

- AI capital spending remains a major growth driver, but markets are increasingly testing whether hyperscalers can convert investment into revenue and free cash flow.

- The second-half outlook depends on the interaction among inflation, oil prices, Treasury demand, corporate earnings and the November midterm elections.

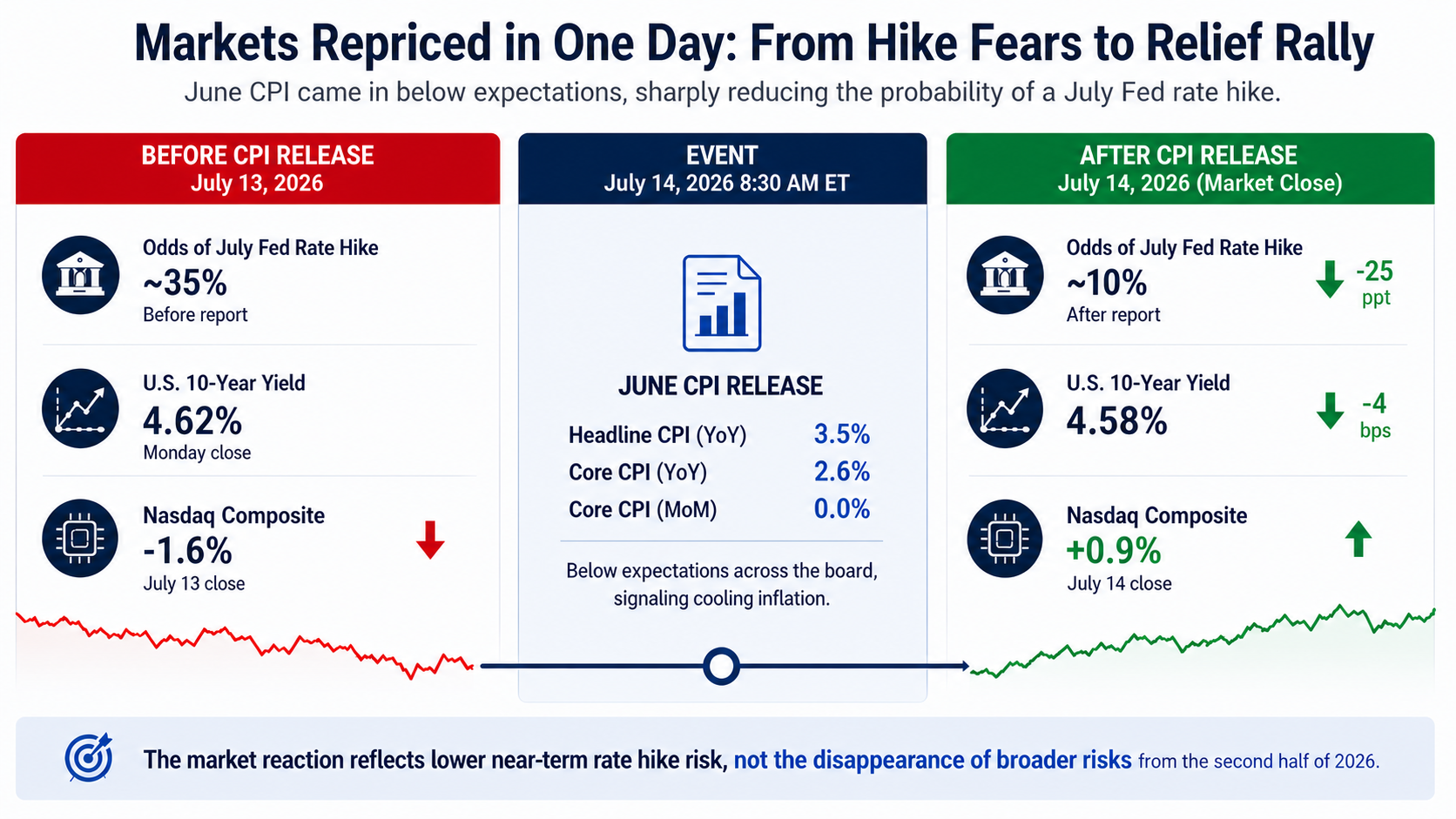

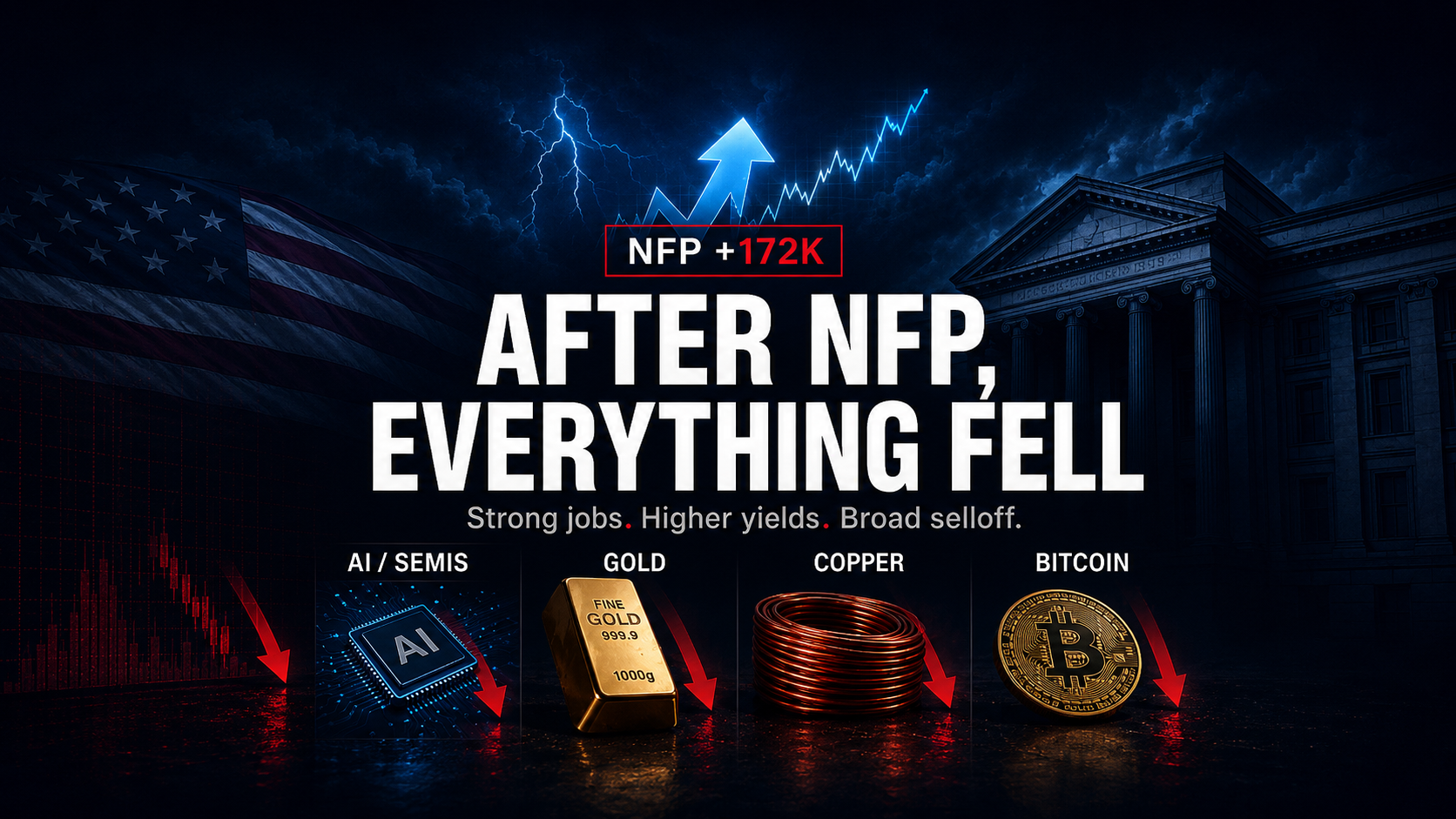

The market’s view of Federal Reserve policy changed abruptly after the release of the June Consumer Price Index. Only a day earlier, investors had been assigning substantial probability to another rate increase as oil prices rose, the conflict with Iran intensified and Federal Reserve officials maintained a restrictive tone. The inflation report weakened that case. Headline CPI fell 0.4% from the previous month, while the energy index declined 5.7%. Core inflation was unchanged on a monthly basis, providing evidence that the improvement extended beyond gasoline alone.

The immediate market reaction was understandable. Lower inflation reduced the need for the Federal Reserve to tighten policy at its next meeting, eased pressure on short-term Treasury yields and improved the valuation case for growth companies whose earnings lie further in the future. Yet the rally should be understood as a repricing of near-term interest-rate risk, not as proof that the broader sources of market instability have disappeared.

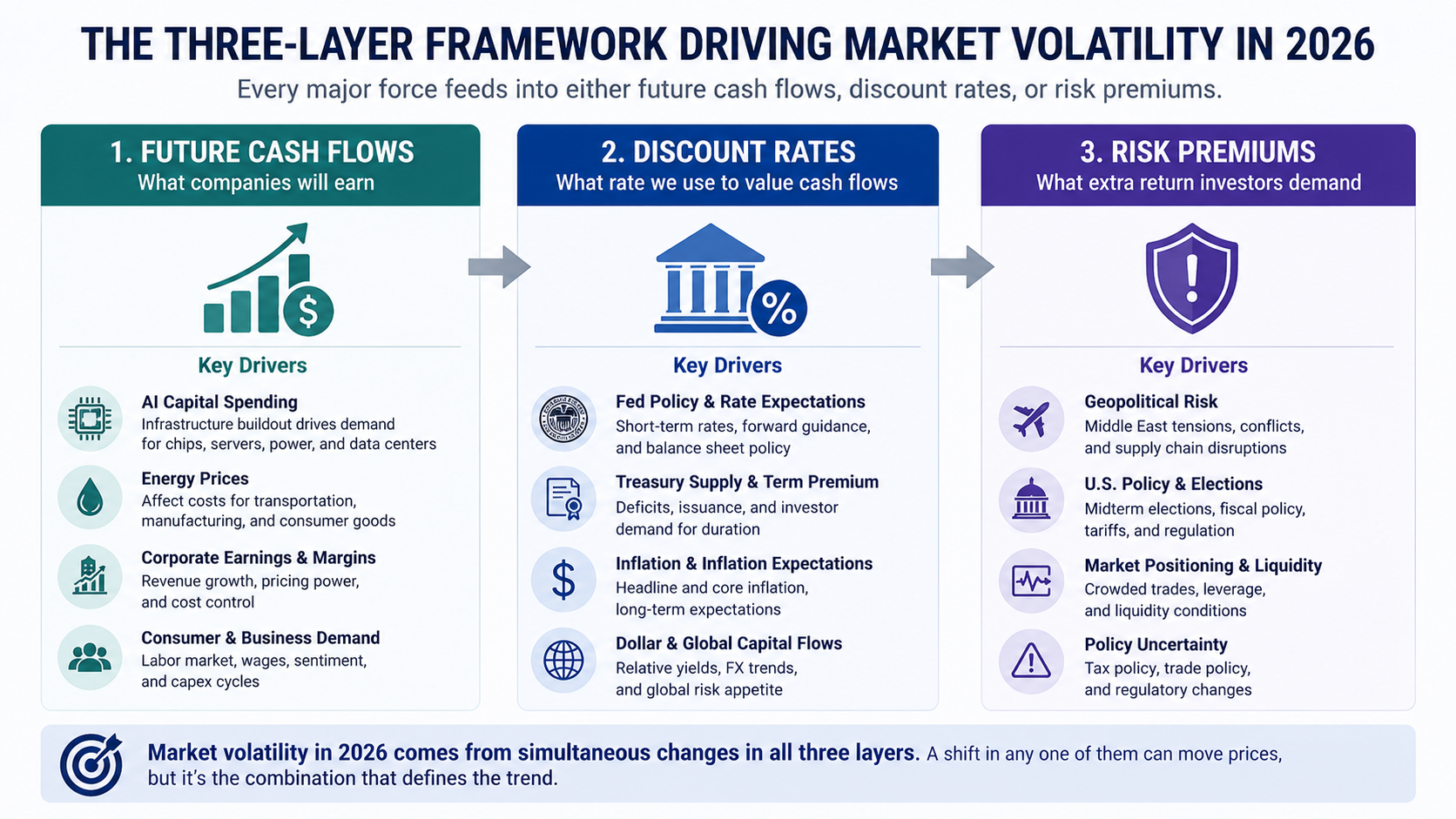

That distinction matters because monetary policy is only one part of the valuation equation. Stock prices reflect expected future cash flows, the rate used to discount those cash flows and the risk premium investors require to hold them. In 2026, all three are moving at the same time. Inflation and the Federal Reserve affect the discount rate; war, elections and policy uncertainty affect the risk premium; AI spending, energy costs and corporate earnings affect future cash flows. A favorable CPI report can relieve pressure in one area while leaving the others largely untouched.

Inflation improved, but the June report described an earlier energy environment

The June CPI report contained genuine signs of progress. Core prices were flat for the month, and several categories that had previously contributed to persistent inflation showed less pressure. That gives the Federal Reserve more room to wait for additional evidence rather than reacting immediately to an energy-driven increase in headline prices. The next CPI report, covering July, is scheduled for August 12.

The limitation is that June inflation was measured during a period in which energy prices had fallen. The report therefore captured the economic effects of an earlier and more favorable oil market. By July, the conflict involving the United States and Iran had again raised concerns about energy supply and transportation through the Persian Gulf.

This creates a timing problem for financial markets. The latest CPI report shows that an earlier energy shock had reversed and that underlying price pressure had softened. It does not yet show how renewed oil-price increases will affect gasoline, air travel, freight, food distribution or manufacturing costs in the months ahead. Energy is excluded from core CPI, but sustained increases can eventually reach core inflation through transportation, wages, insurance and production expenses.

Federal Reserve Chair Kevin Warsh did not present the June report as a decisive policy turning point in his July 14 testimony to the House Financial Services Committee. His testimony continued to emphasize price stability and the need to place the inflation episode firmly in the past. The central bank may have gained time, but it has not declared victory.

The market has therefore moved away from an immediate rate-hike scenario. It has not returned to the low-rate regime that supported much of the previous decade’s equity valuation expansion.

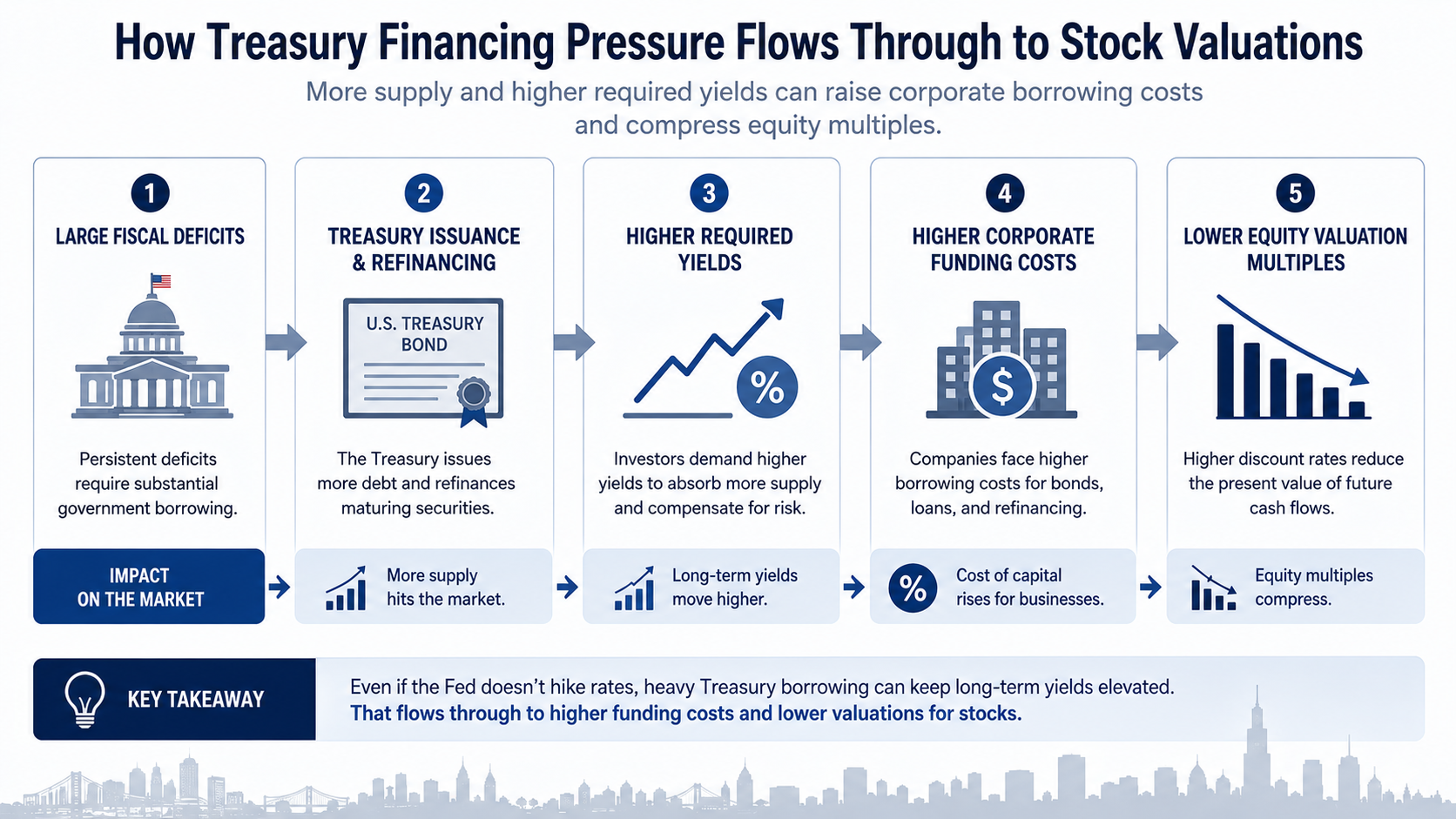

The Treasury market may matter more than a single Federal Reserve meeting

The debate over whether the Federal Reserve raises its policy rate can obscure a larger issue. Short-term interest rates are heavily influenced by the central bank, but long-term yields also reflect fiscal deficits, Treasury supply, inflation uncertainty and the compensation investors demand for lending money over many years.

The Treasury Department expects to borrow $671 billion in privately held net marketable debt during the July-through-September quarter, compared with an estimated $189 billion during the April-through-June quarter. The next financing estimates are scheduled for August 3, followed by the quarterly refunding announcement on August 5.

The relevant issue is not simply that Treasury securities are reaching maturity. Maturing debt is normally refinanced through new issuance. The market question is how much old debt must be rolled over, how much additional borrowing is required to finance the deficit, which maturities the Treasury chooses to issue and what yield investors will demand to absorb the supply.

If private investors, banks, pension funds, foreign institutions and money-market funds require higher yields, the effect extends well beyond the federal budget. Treasury yields serve as a benchmark for corporate borrowing, mortgages and equity valuation. A company can report strong earnings and still face a lower valuation multiple if the risk-free rate used to discount those earnings remains elevated.

This is why a softer CPI report can push two-year yields lower without resolving the pressure on ten- and thirty-year yields. The front end of the yield curve primarily reflects expectations for Federal Reserve policy. The long end must also compensate investors for debt supply, fiscal uncertainty and duration risk. A Reuters 2026 outlook poll forecast the ten-year Treasury yield at 4.25% by year-end, underscoring that softer near-term inflation does not automatically restore the low-yield conditions of the previous decade.

The second half of 2026 may therefore be shaped less by a single rate decision than by the interaction between Treasury financing needs and the market’s willingness to fund them.

VIUS has examined the same fiscal-monetary tension in its analysis of why U.S. fiscal and monetary policy can pull markets in opposite directions and in its discussion of dollar credibility, Treasury demand and global capital flows.

A strong dollar can attract global capital without benefiting every U.S. company

The dollar is often treated as a simple inverse signal for stocks. In practice, its effect depends on why it is rising.

A stronger dollar can reflect higher U.S. real yields, stronger relative economic growth or demand for safe and liquid American assets. Foreign investors purchasing Treasury securities, U.S. money-market instruments or American equities generally need dollars to complete those transactions. In that sense, dollar strength can be both the result of capital flowing into the United States and a force that reinforces the relative appeal of U.S. assets.

That mechanism helps explain why the dollar and U.S. equities can rise together. America still offers the world’s deepest government bond market, its largest and most liquid equity market, and the companies receiving the greatest share of global AI investment. When capital is seeking yield, liquidity or exposure to U.S. productivity growth, a strong dollar does not automatically prevent the stock market from advancing.

The corporate effect is more uneven. A stronger dollar reduces the translated value of overseas sales for multinational companies. It can lower imported input costs for businesses that buy goods abroad, support financial institutions that benefit from global capital flows and tighten financial conditions for emerging-market borrowers with dollar-denominated debt.

The correct question is therefore not whether a strong dollar is bullish or bearish. It is whether the dollar is strengthening because the United States is attracting productive capital, because U.S. interest rates are unusually high or because global investors are retreating from risk. The same move in the currency can produce very different outcomes for corporate earnings and equity valuations.

The conflict with Iran affects more than the price of oil

Geopolitical events become economically significant when they alter supply, costs or the probability distribution of future outcomes. The conflict involving Iran matters to markets because it can affect energy transportation, inflation expectations, corporate margins and monetary policy at the same time.

The first channel is direct. Higher oil prices raise gasoline and aviation costs and increase expenses across freight, chemicals, manufacturing and food distribution. The second channel runs through monetary policy. If the energy increase is brief, the Federal Reserve can look through it. If it persists and begins to influence wages, services and inflation expectations, the central bank has less room to ease policy.

The third channel is the equity risk premium. War increases uncertainty over future cash flows even before reported earnings change. Investors may demand a larger return to hold equities, lowering the valuation multiple they are prepared to pay. Energy and defense companies may benefit from the underlying event, while airlines, transport companies and long-duration growth stocks face a less favorable combination of higher costs and higher discount rates.

This explains why the June CPI report and the renewed conflict can point markets in opposite directions. The CPI report describes an earlier decline in energy prices. The conflict creates the possibility that those gains will partially reverse. The durability of the market response will depend less on the headlines themselves than on whether oil supply remains impaired long enough to alter inflation and earnings.

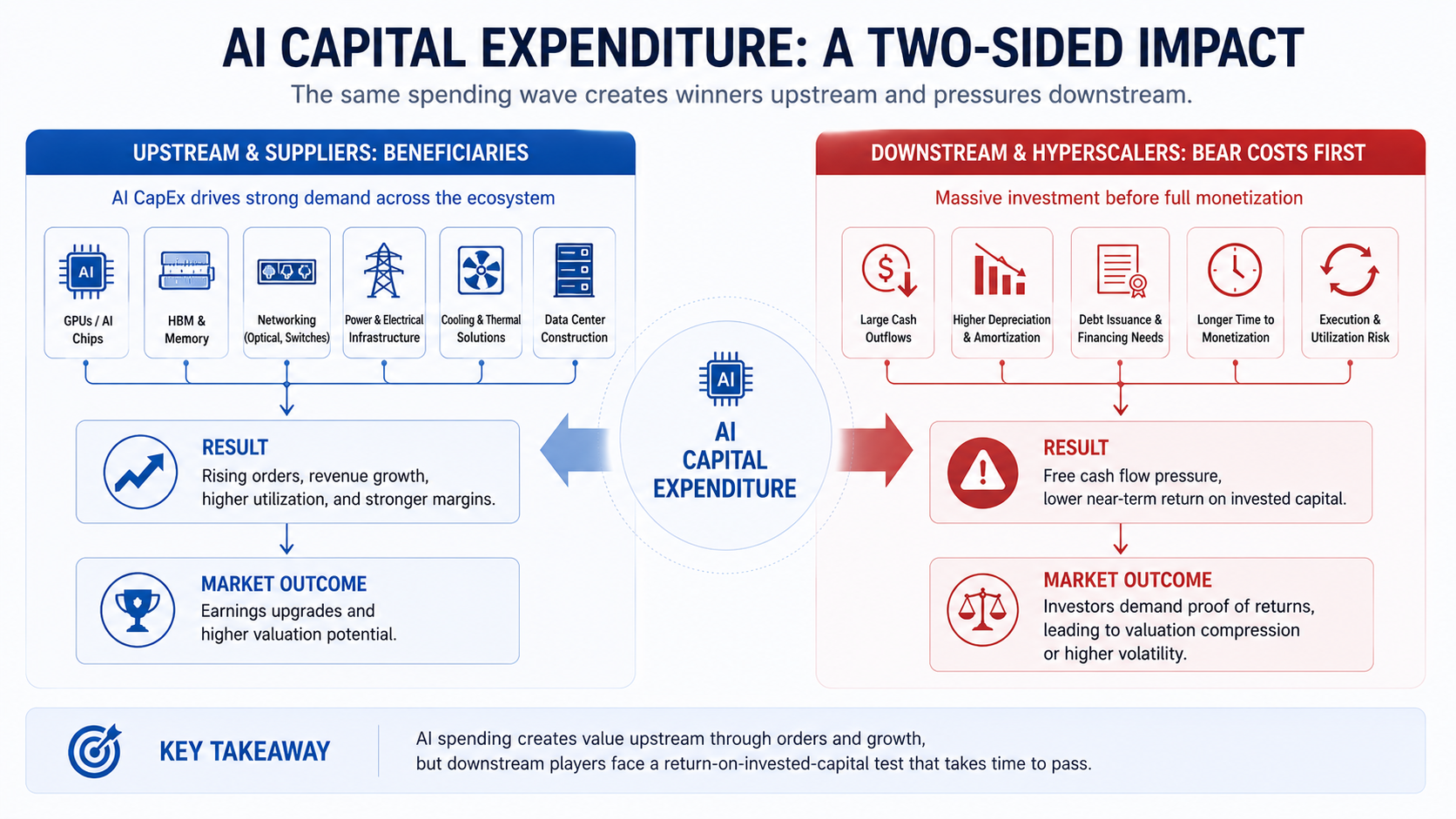

AI capital spending is still supporting growth, but it is no longer exempt from return requirements

Artificial intelligence remains one of the strongest sources of investment demand in the U.S. economy. The spending cycle is supporting semiconductor production, memory, networking, optical components, electrical equipment, cooling systems, construction and data-center development. It has also become a major source of financing activity for Wall Street. Bank of America has participated in nearly $500 billion of AI-related fundraising since 2025, while a Meta data-center project in Texas involved a financing package of roughly $13 billion.

The market’s treatment of that spending is changing. For suppliers of GPUs, memory, networking and power infrastructure, capital expenditure can become revenue relatively quickly. For hyperscalers funding the buildout, the first effects are cash outflows, greater depreciation and, increasingly, debt issuance. Revenue and productivity gains may arrive later.

That delay is now central to technology valuations. Investors are no longer asking only whether AI spending will continue. They are asking whether cloud revenue, advertising efficiency, enterprise software sales and new AI services will grow quickly enough to cover the rising cost of computing infrastructure.

The concern is visible in both equities and credit. Reuters reported that uncertainty over AI profitability is rising even as investor conviction becomes more extreme. A Bank of America survey found that 82% of fund managers considered long global semiconductor stocks the market’s most crowded trade, while hyperscaler free cash flow was coming under increasing pressure.

Semiconductor stocks illustrate the other side of the trade. The Philadelphia Semiconductor Index fell more than 11% after reaching a June record, even though it remained up sharply for the year and industry earnings were expected to grow substantially. The correction reflected concerns over valuations, the durability of AI spending and the cyclical nature of chip demand rather than clear evidence that infrastructure investment had ended.

AI capital expenditure is therefore simultaneously a source of economic growth, supplier revenue, corporate financing demand and valuation risk. The decisive variable is no longer the amount being spent. It is the return generated on that spending.

The return question is developed further in VIUS research on AI capital expenditure and token-cost payback periods and Meta’s effort to turn infrastructure spending into advertising, model and compute revenue.

The midterm elections will influence the market through policy, not through the vote alone

The November 3 midterm elections are likely to become a larger market variable as the year progresses, but their financial importance lies in the policies they may change.

Control of Congress will affect the administration’s ability to pass tax legislation, alter spending, extend industrial support, modify energy policy and pursue new tariff or regulatory measures. Expectations for a divided government may reduce the probability of large fiscal legislation. Continued unified control could increase policy implementation capacity while also widening the range of possible changes to deficits, trade and regulation.

The election period can influence markets even before the result. Governments facing voters have incentives to emphasize growth, employment, energy affordability and household purchasing power. Measures intended to support near-term demand can improve corporate revenue while worsening the fiscal outlook. Attempts to reduce energy prices may help inflation but affect energy-sector profitability. Tariffs may support certain domestic producers while raising costs for importers and manufacturers.

The election should therefore be treated as a catalyst that changes the probability of future fiscal, trade and regulatory outcomes. It is not separate from the Treasury market, the dollar or corporate earnings. Its importance comes from its ability to alter all three.

Why the market has remained unstable throughout 2026

The volatility of 2026 is not the product of one unusually nervous market or one unresolved Federal Reserve decision. It reflects the absence of a single variable powerful enough to dominate all the others.

Lower inflation can reduce expectations for policy tightening, while large Treasury issuance keeps long-term yields elevated. A strong dollar can attract global capital into U.S. assets while reducing the reported overseas earnings of multinational companies. AI investment can support economic growth and semiconductor demand while reducing hyperscaler free cash flow. War can benefit energy and defense companies while raising inflation and the equity risk premium. Fiscal support ahead of an election can strengthen demand while increasing the supply of government debt.

These forces operate over different time horizons. A CPI surprise can move interest-rate futures within minutes. Treasury issuance affects yields over months. AI capital expenditure enters depreciation schedules and income statements over several quarters. Election results can alter the policy environment for the following two years.

Frequent market reversals do not mean that prices are moving without logic. They mean that the marginal driver of valuation is changing more rapidly than it did during periods dominated by a single narrative.

A simpler framework for interpreting market moves

The number of variables does not require every market participant to become a macro trader. Most price movements can still be separated into three categories.

The first is a change in the discount rate. Inflation, Federal Reserve expectations, Treasury issuance and global demand for dollars alter the valuation multiple applied to a given stream of earnings. A company’s share price can decline even when its operating outlook has not changed.

The second is a change in expected cash flow. Persistent energy inflation, weaker customer demand, deteriorating margins or AI spending that fails to generate revenue can directly reduce the future earnings power of a business. A lower share price in that case reflects more than a temporary change in market sentiment.

The third is a change in the risk premium. War, elections and policy uncertainty can lower valuations before the effect on earnings becomes measurable. Whether the adjustment proves temporary depends on whether the uncertainty eventually becomes a change in costs, taxes, regulation, financing conditions or demand.

This framework is more useful than reacting independently to every economic release. The key distinction is whether an external event has changed the price investors are willing to pay for the same business, or whether it has changed the amount of cash the business is likely to produce.

Large institutions can profit from rapid changes in oil, rates, currencies, options and market probabilities. Individual investors generally do not possess the same information speed, trading infrastructure or hedging capacity. Their analytical advantage, where one exists, comes from operating on a longer time horizon and distinguishing temporary repricing from lasting deterioration in business economics.

The CPI report bought the market time, not certainty

The June inflation report materially reduced the case for an immediate Federal Reserve rate increase. That was sufficient to lower short-term yields and support a rebound in technology stocks. It was not sufficient to resolve the Treasury’s second-half financing needs, determine the path of oil prices, validate the return on hundreds of billions of dollars in AI investment or settle the fiscal and regulatory consequences of the midterm elections.

The next phase of the market will be shaped by whether lower inflation survives the renewed energy shock, whether private investors can absorb a larger volume of Treasury and corporate debt without demanding much higher yields, and whether technology companies can convert infrastructure spending into revenue and free cash flow.

One CPI report changed the probability of the next policy decision. It did not change the structure of the market. In 2026, stock prices are being determined by future cash flows, discount rates and risk premiums at the same time. That is why a single favorable data point can produce a strong rally without ending the volatility that created it.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Consumer Price Index — June 2026 | U.S. Bureau of Labor Statistics | 2026-07-14 | Government | Supports the 0.4% monthly CPI decline, 3.5% year-over-year headline CPI, 5.7% energy-index decline, flat monthly core CPI and 2.6% year-over-year core CPI. |

| 2 | 2026 CPI release calendar | U.S. Bureau of Labor Statistics | 2026 | Government | Supports the August 12, 2026 release date for the July CPI report. |

| 3 | Semiannual Monetary Policy Report to the Congress | Board of Governors of the Federal Reserve System | 2026-07-14 | Government | Supports Chairman Kevin Warsh's July 14 testimony and continued emphasis on price stability. |

| 4 | Treasury Announces Marketable Borrowing Estimates | U.S. Department of the Treasury | 2026-05-04 | Government | Supports the $671 billion July–September and $189 billion April–June privately held net marketable borrowing estimates. |

| 5 | Most Recent Quarterly Refunding Documents | U.S. Department of the Treasury | 2026-05-06 | Government | Supports the quarterly refunding process and the scheduled August 3 financing-estimate and August 5 refunding-document releases. |

| 6 | Traders expect Fed to skip July rate hike as inflation cools | Reuters | 2026-07-14 | News | Supports the shift in July rate-hike probability from about 35% before CPI to about 10% afterward, the Middle East energy context and the market-repricing discussion. |

| 7 | Markets’ 2026 watch list: Fed succession, political risk and AI of course | Reuters | 2025-12-30 | News | Supports the 2026 market outlook and the end-2026 10-year Treasury yield forecast of 4.25% in the cited Reuters poll. |

| 8 | Wall Street banks see AI ‘super cycle’ set to boost deals, financing | Reuters | 2026-07-14 | News | Supports Bank of America's nearly $500 billion of AI-related fundraising since 2025 and the roughly $13 billion Meta data-center financing package. |

| 9 | Global investors turn most bullish since February, BofA survey shows | Reuters | 2026-07-14 | News | Supports the July fund-manager survey, including 82% identifying long global semiconductor stocks as the most crowded trade. |

| 10 | Chip stocks hit rocky patch. What’s next? | Reuters | 2026-07-13 | News | Supports the more-than-11% decline in the Philadelphia Semiconductor Index from its June record and the valuation and AI-capex concerns behind the correction. |

| 11 | 2026 Primary Elections by State and Territory | Federal Voting Assistance Program | 2026 | Government | Supports the November 3, 2026 general election date. |

Figures and dates were checked against the linked BLS, Federal Reserve, Treasury and federal election sources, together with Reuters reporting. The CPI-repricing graphic was corrected before publication to remove unsupported oil-price and index figures from the supplied generated image.

Related Reading

America Is Rewriting Dollar Credibility

The U.S. is rebuilding dollar credibility through strong-dollar policy, Treasury demand, Fed uncertainty, stablecoins, AI infrastructure, and gold reserves.

The U.S. Economy and U.S. Fiscal System Are Demanding Opposite Monetary Policies

What broke on June 5 was not AI valuation, but the market’s faith in endless Quantitative Easing

Meta Does Not Have an AI Compute Glut

Meta Compute is not an AI capex retreat. Meta is still expanding data center capacity while turning AI compute into a flexible asset across ads, models, APIs, and external leasing.

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

Micron Is Trying to Escape the Memory Cycle. The Real Test Begins After 2027.

Micron’s AI memory boom is no longer just about one strong quarter. The real question is whether Strategic Customer Agreements, HBM demand, and record capex can turn a memory cycle into a more predictable AI infrastructure business.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments