A report that Meta may offer AI compute capacity to outside customers triggered a sharp selloff in neocloud stocks such as CoreWeave and Nebius. The market quickly turned one headline into a larger story: Meta bought too much compute, AI capex is finally peaking, and the hardware cycle is approaching a demand cliff.

That reading goes too far.

Meta is not signaling a retreat from AI infrastructure. It is still locking down massive amounts of future capacity while creating more ways to monetize that capacity when internal demand and infrastructure deployment do not line up perfectly. Compute can go into its advertising recommendation systems. It can feed Meta Superintelligence Labs. It can be packaged into model API services. It can also be leased to outside customers that urgently need large-scale clusters.

The important shift is not that Meta has stopped spending. The important shift is that Meta is trying to make AI infrastructure more flexible.

Meta's own guidance points in the opposite direction of a slowdown. In Q1 2026, the company raised full-year capital expenditure guidance to $125 billion to $145 billion, up from the prior range of $115 billion to $135 billion. AP reported that Meta also guided Q2 revenue to $58 billion to $61 billion after Q1 revenue grew 33% year over year to $56.31 billion.

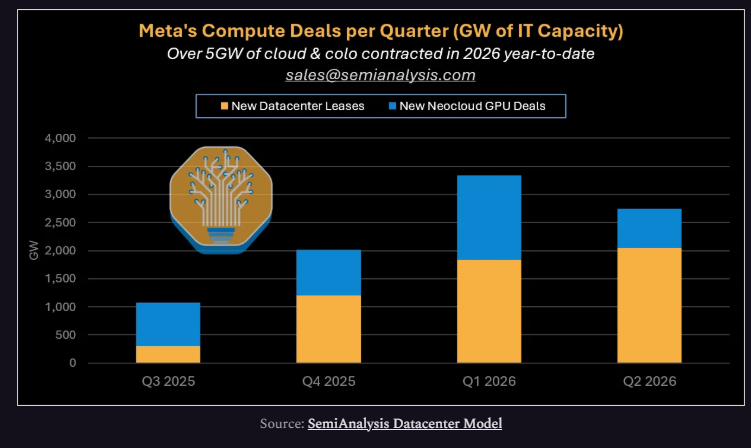

SemiAnalysis reached a similar conclusion from the infrastructure side. In its July 3 report, "Meta Compute: Everyone Wants To Be A Neocloud," the firm said Meta had signed more than 5GW of data center capacity in the first half of 2026 across cloud leasing and colocation, excluding the full progress of its self-built projects.

SemiAnalysis also showed satellite and aerial imagery of Meta's two largest data center campuses, which together represent roughly 2.5GW of capacity under construction.

If Meta were preparing to pull back from AI infrastructure, the numbers would not look like this. It is not reducing future capacity. It is accelerating the process of securing it. Some capacity may become available for external customers in certain windows, but that does not automatically mean structural oversupply. It means the buildout is large enough that Meta needs more than one outlet for the compute it is bringing online.

AI infrastructure does not move in a perfectly synchronized chain. GPUs arrive on one schedule. Data centers come online on another. Training runs, inference workloads, recommendation systems, and product launches all scale at different speeds. A company building ahead of demand will inevitably see temporary mismatches. The real question is whether that slack has high-value uses.

This is where Meta differs from a pure neocloud.

CoreWeave and Nebius primarily monetize GPUs through external leasing contracts and RPO growth. Meta does not need to sell GPU hours to prove that its compute is valuable. Its highest-quality compute monetization path may sit inside the advertising system, which remains the company's strongest business.

MarketWatch reported that Meta's ad impressions across its family of apps rose 19% year over year in Q1 2026, while the average price per ad increased 12%. According to eMarketer estimates cited by The Wall Street Journal, Meta's global net ad revenue is expected to reach $243.46 billion in 2026, ahead of Google's projected $239.54 billion. If that forecast holds, Meta would become the world's largest digital advertising platform by net ad revenue.

That is the underappreciated part of Meta's AI capex story. Investors often focus on Llama, Meta Superintelligence Labs, Claude access, or a potential cloud business. But Meta's most reliable AI return may never appear as a standalone line item called AI revenue. It may show up in ad pricing, advertiser ROAS, user time spent, recommendation quality, and commercial conversion.

Larger recommendation models can make content distribution more precise. Better content distribution increases engagement. Better engagement expands ad inventory. More precise ad matching improves advertiser returns. Stronger returns support higher ad prices. In that loop, GPUs are not simply rental assets. They are inputs into Meta's ad-pricing machine.

That path fits Meta's DNA. Meta is exceptional at consumer distribution, recommendation systems, ad matching, and attention monetization. It does not need to become CoreWeave to monetize compute. If GPUs keep improving the output of its advertising system, Meta is already monetizing a large part of its AI infrastructure internally.

The second outlet is Meta Superintelligence Labs.

MSL is the upside case for Meta's compute demand, but it is not the most dependable base case. If Meta catches OpenAI, Anthropic, or Google in frontier models, internal demand for training, inference, product integration, and distribution could absorb enormous amounts of compute. External leasing would then be a secondary option.

But frontier AI is not a linear engineering problem. More GPUs do not automatically translate into faster model leadership. If MSL succeeds, the upside expands. If it develops more slowly, Meta still needs other ways to justify the scale of its infrastructure spend. That is why recommendation systems, model partnerships, and external leasing matter. Meta is not putting every dollar of compute behind one path. It is building several potential payback routes for the same infrastructure base.

The third outlet is a Bedrock-like model API service.

SemiAnalysis reported that Meta may be in talks with Anthropic to obtain private deployment access to Claude. If that happens, Meta would not only offer its own models. It could package Claude and other frontier model capabilities into its own data centers and compute stack for internal teams or external customers.

That opportunity is real, but it should not be confused with Meta simply becoming another AWS. Amazon Bedrock, Azure AI, and Google Vertex are not just collections of GPUs. They sit on top of enterprise sales teams, procurement relationships, security compliance, billing systems, customer success, developer ecosystems, and long operating histories with enterprise buyers.

Meta has advertisers, consumers, creators, merchants, and distribution. It does not yet have the same enterprise cloud muscle as AWS, Azure, or Google Cloud. The more natural path is not a generic cloud platform. It is AI embedded into the business surfaces Meta already controls: ad agents, creative generation, marketing automation, Instagram and WhatsApp business messaging, commerce support, sales conversion, and consumer AI on smart glasses.

The fourth outlet is short-duration, high-priced compute leasing.

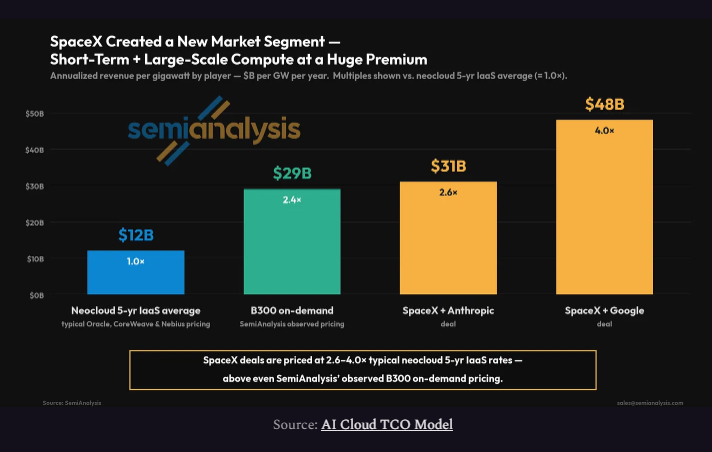

SpaceX and xAI have shown a new form of AI compute product: large scale, short duration, high price, cancelable, and dynamically reallocatable. They are not merely selling generic GPU hours. They are selling large clusters that are available now. For customers that urgently need compute and cannot wait for new data centers, time itself becomes part of the product.

What SpaceX did well was not simply owning compute. It turned compute into a higher-quality contract. A normal neocloud often needs multi-year commitments to support financing. It buys GPUs, builds clusters, borrows capital, and needs long-term offtake agreements to make the asset base financeable. SpaceX and xAI offered something different: immediately available large-scale clusters for customers with extreme urgency and high willingness to pay. Shorter duration, higher pricing, and more flexibility changed the economics.

That creates a new dividing line in AI infrastructure. Having GPUs is no longer enough. The higher-value question is who can turn GPUs into the best-quality cash flow.

SemiAnalysis' criticism of Oracle points to that issue. Oracle's AI compute is more closely tied to long-term cloud contracts that support financing, revenue visibility, and the OCI growth story. That model is stable, but it may not capture the highest price during periods of extreme scarcity.

SpaceX showed a different model. It sold immediate cluster availability, time urgency, and dispatch flexibility. Short-duration, high-priced, cancelable contracts turn compute from fixed infrastructure into a more liquid scarcity asset. Oracle has not packaged capacity in that same form. Long-term contracts create certainty, but they also reduce the ability to reprice capacity during the tightest windows.

That is the part Meta should study: not the act of selling compute, but the contract design.

If Meta simply rents out spare GPUs as ordinary bare-metal capacity, the market will compare it with CoreWeave, Nebius, and Oracle Cloud. That is not the best path. Meta should target only a small number of high-credit, high-urgency, high-willingness-to-pay customers and offer short-duration, cancelable, reclaimable compute contracts.

The strategic value is not just rental revenue. It gives Meta's AI capex more flexibility. When MSL or the ad recommendation system needs capacity, compute can return to internal use. When internal workloads temporarily lag infrastructure availability, capacity can be leased to customers such as Anthropic, Google, or xAI that urgently need large clusters. Meta's advantage is not that it can become a cloud vendor. Its advantage is that its advertising cash flow and internal demand allow it to tolerate more short-term utilization risk than a typical neocloud.

That is where Meta's financial strength matters. The company can fund AI infrastructure from a massive advertising business, a large cash base, and recurring operating cash flow. Those numbers are not just proof that Meta can afford AI capex. They explain why Meta has more contract freedom than a finance-dependent neocloud. A neocloud needs long-duration contracts to support the asset base. Meta can afford to keep more optionality.

The risk is that Meta may not execute this well.

SpaceX's strengths are engineering speed, resource mobilization, capital market narrative, and extreme execution culture. Oracle's example shows that owning GW-scale capacity does not automatically mean selling compute into the best contract structure. Meta's operating DNA is closer to ad recommendations, social distribution, and consumer products than enterprise cloud operations. Short-duration compute leasing may look like an asset transaction, but in practice it requires heavy operating capability: customer negotiation, delivery assurance, SLA management, security isolation, technical support, contract administration, and rapid capacity scheduling.

Meta is strongest in advertising, not enterprise infrastructure operations. It is excellent at turning attention into ad revenue. It is excellent at recommendation systems and consumer distribution. It has not yet proven that it can serve enterprise cloud customers like AWS, Azure, or Google Cloud. If Meta Compute turns into a generic neocloud strategy, Meta could end up in a lower-margin, operationally heavy, highly competitive market where its natural advantages matter less.

The better strategy is layered compute allocation.

The base layer should be recommendation systems and Family of Apps advertising efficiency. The next layer should be MSL and Meta's own frontier models as the high-upside internal option. Above that, model APIs and Claude-like access can be packaged into commercial workflows, but the first priority should be advertising, marketing, commerce messaging, and consumer AI surfaces. The outer layer should be SpaceX-style large-customer compute leasing: short-duration, high-priced, cancelable, and useful for monetizing temporary slack without giving up strategic control.

The order matters. If external leasing becomes the center of Meta Compute, Meta will be dragged into neocloud valuation logic. If external leasing remains a marginal monetization tool while the core capacity keeps feeding ads, models, and commercial distribution, Meta has a chance to earn a much higher return than generic GPU rental.

For AI hardware stocks, Meta Compute is not evidence that demand has peaked. Based on Meta's capex guidance, SemiAnalysis' data center work, and the current market for large-scale compute contracts, Meta is not preparing to cut AI infrastructure spending. The more important shift is that the compute market is starting to stratify.

At the top are companies like Meta, with internal demand, advertising cash flow, distribution, and a balance sheet that allows compute to move between internal and external use.

A second category includes unusual players like SpaceX and xAI, which can use engineering speed, capital access, and scarce capacity to create short-duration, high-priced contracts.

A third category includes cloud providers such as Oracle, which own large-scale compute but need to prove that capacity is being turned into high-quality cash flow rather than merely long-duration infrastructure revenue.

A fourth category includes neoclouds such as CoreWeave and Nebius. They may still benefit from GPU scarcity, but their valuations will increasingly depend on contract quality, financing costs, power access, customer concentration, and pricing flexibility.

The market used to ask who had GPUs. The next question is who can turn GPUs into the highest-quality cash flow.

Meta Compute does not mark the end of AI capex. It marks the second phase of AI capex. In the first phase, the market rewarded construction scale. In the second phase, the market will demand a clear payback path. Compute is still scarce, but owning compute is no longer enough. The scarce capability is turning compute into a high-ROIC business system.

Meta's best path is not selling compute. It is turning compute into better ads, stronger models, larger distribution, and higher-value commercial applications. Meta can offer compute, but it should not become a low-margin GPU rental company.

If Meta simply rents out spare GPUs, it is entering a heavy operating business with pricing risk and weaker customer relationships than the cloud incumbents. If it uses external leasing to improve capex flexibility while keeping core capacity focused on advertising, model services, and commercial distribution, it is turning AI infrastructure into a strategic asset.

The important question is not whether Meta has too much compute. The important question is whether Meta can prove that massive AI capex is not just a cost, but an asset that can be repriced across ads, models, customers, and distribution.

That is the next phase of the AI infrastructure race.

Related Reading

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

How to Read the AI Cycle: CapEx, Supply Bottlenecks, and the Semiconductor Trade

AI infrastructure spending is still expanding, but the semiconductor equity trade is becoming more fragile. The next phase depends on CapEx, supply bottlenecks, usage, pricing, and earnings revisions.

NVIDIA’s Next Bottleneck Isn’t GPUs. It’s Data Movement.

Why AI factories are moving from copper to optical connectivity — and which suppliers deserve deeper research

Sources & Notes

Sources for this article are listed below. Meta Q1 2026 financial and advertising metrics are cited in text only. Required SemiAnalysis screenshots remain placeholder comments where the original report images were not publicly retrievable in this environment.

| Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|

| Meta beats revenue expectations, boosts capital spending forecast for 2026 | Associated Press | 2026-04-29 | Market reporting | Used for Meta Q1 2026 revenue, Q2 revenue guidance, and updated 2026 capex guidance. |

| Meta's ad impressions continue to mount | MarketWatch | 2026-04-29 | Market reporting | Used for Q1 2026 ad impressions and average price per ad. |

| Google Set to Lose Its Digital-Ad Crown | The Wall Street Journal / eMarketer | 2026-04-13 | Market reporting | Used for eMarketer's 2026 global net ad revenue forecast for Meta and Google. |

| Meta reportedly plans to rent out its AI compute, sending AI stocks tumbling | Tom's Hardware | 2026-07-02 | Market reporting | Used for public reporting on Meta Compute, neocloud market reaction, CoreWeave, Nebius, SpaceX-style compute leasing, and referenced SemiAnalysis capacity context. |

| Meta Compute: Everyone Wants To Be A Neocloud | SemiAnalysis | 2026-07-03 | Manual Source | Original report referenced for Meta capacity, data center campus imagery, Anthropic / Claude private deployment discussion, and SpaceX / xAI compute leasing comparisons. Screenshots require manual source access. |

FAQ

Does Meta Compute mean Meta has too much AI compute?

Not necessarily. Meta is still raising capex guidance and securing future capacity. Meta Compute is better understood as a flexible monetization layer for temporary capacity mismatches.

Why is Meta different from a neocloud?

A neocloud primarily monetizes external GPU leasing. Meta can also monetize compute internally through advertising recommendations, consumer AI products, model services, and business tools.

What is the key investment question for Meta AI capex?

The key question is whether Meta can turn compute into high-quality cash flow across ads, models, APIs, and selective leasing rather than becoming a low-margin GPU rental business.

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security.

Comments