Two of the hottest themes in the market today are AI and the space economy.

AI has already shown investors what an infrastructure boom can look like. The biggest long-term winner was not necessarily the most visible application company. It was the company that became difficult for the entire industry to work around. Nvidia did not become the defining AI stock simply because it sells GPUs. It became the center of the AI trade because its chips, networking, systems, software ecosystem, and developer dependence turned into a full infrastructure layer.

Nvidia's latest numbers made that position hard to ignore. Fiscal 2025 revenue reached $130.5 billion, and data center revenue alone reached $115.2 billion. That is what infrastructure status looks like when it has already been validated by customer demand, revenue, and capital allocation.

Now a similar question is starting to appear in the space economy.

Recent space-related news has looked fragmented on the surface. Rocket Lab announced an agreement to acquire Iridium in a deal valued at roughly $8 billion in enterprise value. SpaceX has been increasingly analyzed by Wall Street not just as a rocket company, but as a platform with launch, Starlink, and potential data infrastructure businesses. Space stocks have also become more sensitive to news flow: positive headlines can quickly push prices higher, but high valuations can also lead to sharp pullbacks.

Looked at one by one, these are just headlines.

Viewed through an investment framework, they all point to the same question: the space economy is moving from vision and technology into business-model validation and capital-market repricing.

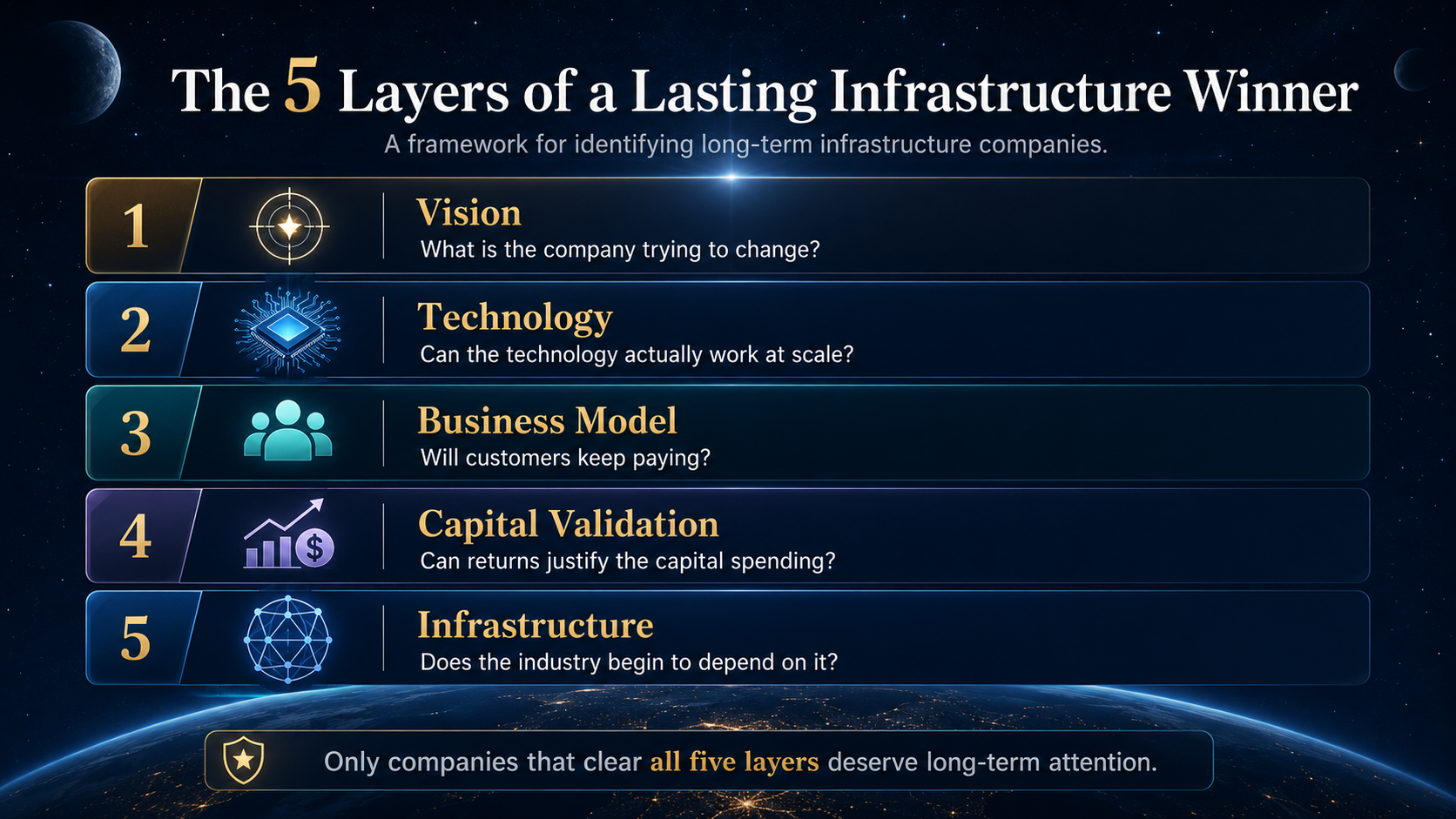

That is where major investment cycles become interesting. The real opportunity is not simply that a theme becomes popular or that a stock rises after a news event. The real question is whether a company can move through five layers of validation and eventually become part of the industry's core infrastructure.

The first layer is vision.

The vision behind the space economy is large enough to attract capital. Lower the cost of access to orbit. Build global satellite communications. Serve defense, aviation, maritime, emergency response, remote connectivity, and potentially future data transmission or orbital computing.

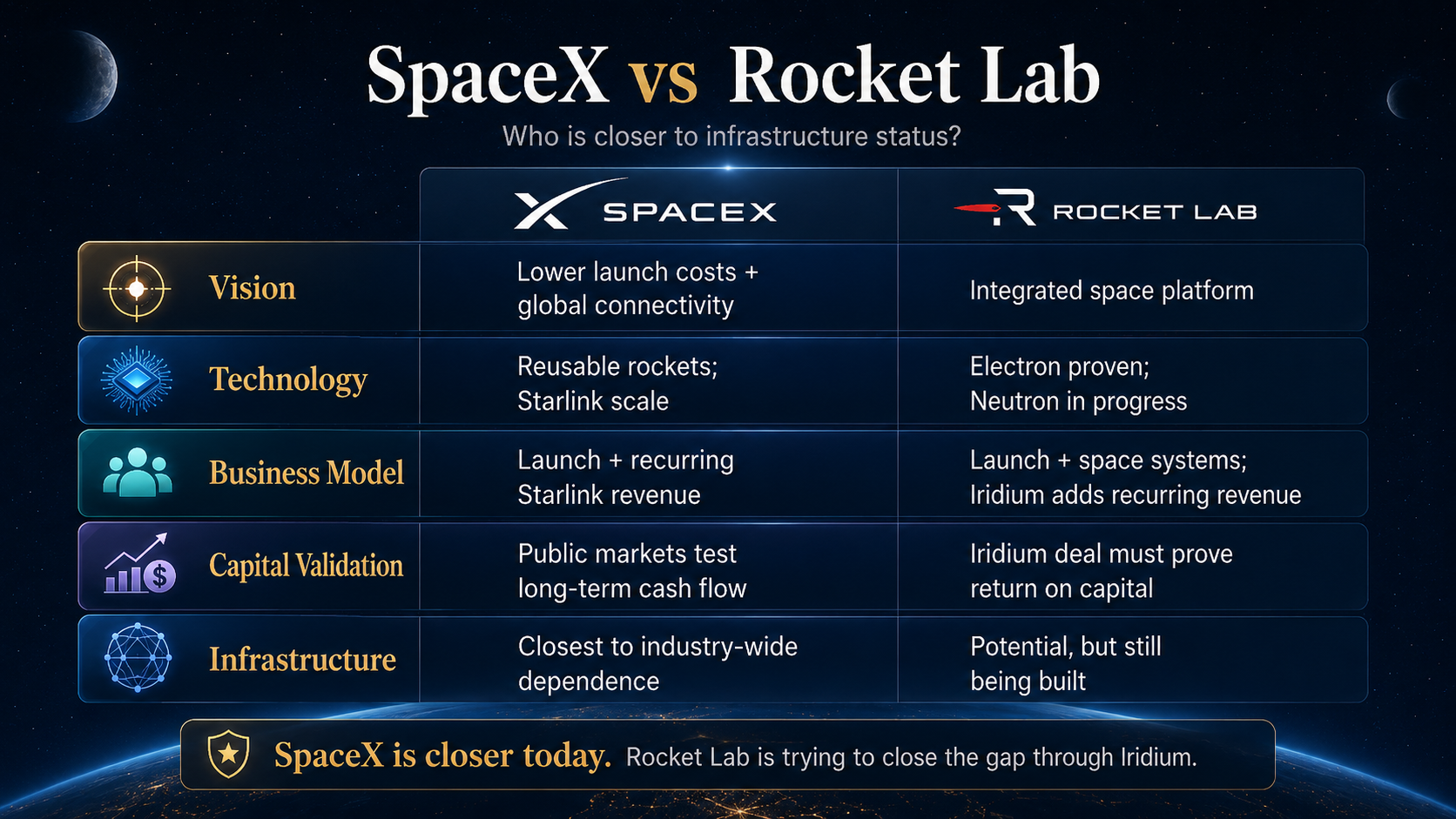

SpaceX has the clearest version of this vision: use reusable rockets to lower launch costs, then turn that cost advantage into a global communications network through Starlink. Rocket Lab's vision is also evolving. It started as a launch and space systems company, but by acquiring Iridium, it is trying to move closer to a full space platform.

But vision is only the first layer. It defines the ceiling. It does not define investment value.

Many major themes begin with powerful visions: clean energy, AI, autonomous driving, the metaverse, commercial space. The larger the story, the easier it is for investors to overlook the next layers of validation. The companies that survive cycles are not the ones with the biggest story. They are the ones whose story can be converted into technology, business model, capital returns, and eventually infrastructure status.

The second layer is technology.

SpaceX has already validated this layer better than anyone else in the industry. Falcon 9's reusable architecture and high launch cadence turned lower launch cost from a slogan into an operating reality. If Starship continues to progress, it could further reduce the cost of deploying Starlink and future orbital infrastructure at scale.

Rocket Lab is not a concept company either. Electron has proven its small-launch capability, and its space systems business gives it more than a single-product launch profile. The question for Rocket Lab is not whether it has technology. The question is whether that technology can support a larger business loop.

This layer matters, but it is also where investors often make mistakes.

Technological breakthroughs create excitement. They can also create sharp stock moves. But technology is not the end point. A rocket that reaches orbit does not automatically create durable profits. A satellite network in space does not automatically mean customers will pay for years. A large total addressable market does not mean every company in the theme will capture economic value.

AI went through the same separation. Many companies participated in the AI supply chain, but the market's long-term reward went to the company that turned technology into infrastructure. Nvidia is not special merely because it is "an AI company." It is special because its GPUs, CUDA ecosystem, networking, systems, and developer base became difficult for customers to replace.

The space economy will likely separate in the same way.

The third layer is business model.

This is why Rocket Lab's proposed acquisition of Iridium matters. The most important part of the deal is not the $8 billion headline number. It is why Rocket Lab wants Iridium in the first place.

Iridium owns a global satellite communications network, L-band spectrum, more than 2.55 million active users, over 500 partners, and customers across government, maritime, aviation, industrial, and emergency communications. Rocket Lab disclosed that Iridium generated roughly $871.7 million in 2025 revenue and about $495 million in OEBITDA, with a 57% OEBITDA margin.

That means Iridium is not just another space story. It has customers, spectrum, a network, and cash flow.

Those are exactly the pieces Rocket Lab has historically lacked. Launch answers the question: can you put assets into space? Iridium answers a different question: once they are there, can you operate a network, serve customers, and generate recurring revenue?

If Rocket Lab only remains a launch provider, it looks more like a contractor inside the space economy. If it can combine launch, satellite manufacturing, communications networks, spectrum, and customer relationships, it begins moving toward an infrastructure platform.

SpaceX has followed a similar logic. Its valuation debate is not supported only by launch. Launch creates the cost advantage. Starlink turns that advantage into a global communications network and recurring subscription revenue. Wall Street's discussion of SpaceX has also shifted away from rockets alone and toward a broader platform that includes launches, Starlink satellite internet, and potential AI-focused data infrastructure.

That is the core question of the third layer: will customers keep paying?

In the space economy, the companies worth studying are not simply the ones with the biggest market narrative. They are the companies that are moving into mission-critical customer workflows. Government communications, maritime connectivity, aviation, defense networks, remote broadband, disaster response - these are not casual use cases. Once a company becomes embedded in those workflows, value starts to look less like one-time hardware revenue and more like long-duration infrastructure revenue.

The fourth layer is capital validation.

This is the layer that matters most right now.

Rocket Lab's acquisition of Iridium is strategically easy to understand, but capital markets will not reward the strategy automatically. Investors will ask harder questions. Is $8 billion in enterprise value the right price? Will the financing structure dilute future shareholder returns? Can Iridium's cash flow support Rocket Lab's broader expansion? Will the combined company create real synergies, or is this simply a high-growth space company being combined with a mature communications asset?

SpaceX faces the same type of test as Wall Street gives it more public-market style scrutiny. Private markets can reward vision for a long time. Public-market investors reprice revenue, growth, capital expenditure, free cash flow, and valuation assumptions every day. A bullish analyst rating may show that Wall Street recognizes SpaceX's platform potential, but volatility across space-related stocks also shows that the market is no longer simply applauding a grand story. It is testing each business line's ability to deliver.

This is the hard part of the fourth layer.

Vision attracts capital. Technology creates valuation upside. Business model proves that revenue exists. Capital validation asks a tougher question: can the company's revenue cover its capital spending? When will free cash flow appear? Will debt, depreciation, R&D, launch risk, and regulatory risk consume future returns?

AI's recent adjustment follows a similar logic. The market is not rejecting AI. It is no longer rewarding every company tied to AI spending without discrimination. Nvidia has held its position because it converted AI infrastructure status into revenue, profit, and customer dependence. Other AI infrastructure companies will also need to prove that they are not just temporary beneficiaries of the spending cycle, but long-term parts of the industry's operating system.

The space economy is now moving toward the same kind of test.

The fifth layer is infrastructure.

This is what long-term investors are really looking for.

Infrastructure status does not simply mean a company is large or that it appears in the news. It means the industry begins to depend on it. Customers do not use it casually. They build around it. Its technology, network, cost structure, ecosystem position, and capital capacity become part of the foundation on which others operate.

Nvidia has moved close to this position in AI. Model training, inference deployment, AI data center architecture, high-performance networking, and the developer ecosystem all make it difficult for many customers to fully bypass Nvidia. That is why the company is not valued like a normal semiconductor cycle stock.

So who has a chance to reach that layer in the space economy?

SpaceX is currently the closest. It has low-cost launch capability, the Starlink network, consumer and enterprise users, government customers, and the potential to connect communications, data, and future orbital infrastructure. If SpaceX continues to use launch cost advantages to expand Starlink and extend it into enterprise, defense, mobile connectivity, and data infrastructure, it will not just be a space company. It could become part of the global connectivity layer.

Rocket Lab is not there yet, but it is trying to assemble the missing pieces. The significance of acquiring Iridium is that Rocket Lab does not want to remain only a launch and manufacturing company. It wants spectrum, network assets, customers, and cash flow. If the transaction closes and the integration succeeds, the investment debate around Rocket Lab changes. It becomes less about how many rockets it can launch and more about whether it can control a meaningful piece of space communications infrastructure.

But this is where investors need to stay disciplined.

Very few companies reach the fifth layer. Most stay at the vision stage. Some prove technology. Fewer build a durable business model. Many fail during capital validation. Only a small number become infrastructure.

That is why an investment framework matters.

Without a framework, Rocket Lab's Iridium deal is just an acquisition headline. SpaceX's valuation discussion is just another Wall Street note. AI infrastructure volatility is just a short-term market move.

Through the five-layer framework, they point to the same deeper question: capital is starting to identify the next generation of infrastructure companies.

AI has already shown that the largest long-term rewards in a major technology cycle often accrue to the infrastructure layer. Nvidia was not the earliest company to talk about AI. It was not the most visible consumer application. But it became the core infrastructure asset of the AI era.

The space economy may now be entering a similar selection process.

Does SpaceX have a chance to become the infrastructure company of the space economy? Yes. It is currently the closest. Does Rocket Lab have a chance? Also yes, but it still needs to prove the Iridium integration, its financing structure, customer synergies, and long-term cash-flow profile.

Headlines will pass. Stock prices will fluctuate. A company worth holding for the long term has to move through every layer: a large enough vision, real technology, a business model with recurring customer demand, capital returns that can survive public-market scrutiny, and finally a position that makes it difficult for the industry to work around it.

That is the essence of an infrastructure boom.

It is identified early by using the right investment framework.

Related Reading

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

SpaceX IPO: What Are Investors Really Paying For?

Starlink, Starship, AI compute, defense infrastructure, and the valuation risk behind the world’s most anticipated IPO.

If You Missed Nvidia’s 10x Run, Where Is AI’s Next Stop?

The Lesson From GTC Taipei: When Computing Starts Serving Agents, the Next Decade of Wealth Redistribution Begins

Sources & Notes

Sources for this article are listed below. Rocket Lab's Iridium transaction remains subject to stockholder approval, regulatory approvals, financing, and closing conditions.

| Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|

| NVIDIA Announces Financial Results for Fourth Quarter and Fiscal 2025 | NVIDIA Newsroom | 2025-02-26 | Company IR | Used for Nvidia fiscal 2025 revenue and data center revenue. |

| Rocket Lab to Acquire Iridium in Historic Deal Creating a Fully Integrated Space Company | Rocket Lab Investor Relations | 2026-06-29 | Company IR | Used for Iridium enterprise value, active subscribers, partner ecosystem, 2025 revenue, OEBITDA, transaction structure, and strategic rationale. |

| Dan Ives' Final Major Call At Wedbush: SpaceX | Investor's Business Daily | 2026-07-02 | Market reporting | Used for Wall Street discussion of SpaceX, analyst framing, and the view of SpaceX as more than a launch business. |

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security.

Comments