Editor's note: This article was originally published on Substack on June 10, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

SpaceX is not a normal IPO.

A normal IPO asks investors one simple question: is this company worth buying at this price?

SpaceX asks a harder question:

What exactly are investors paying for?

Are they buying a rocket company?

A satellite broadband company?

A defense infrastructure provider?

An AI compute platform?

A long-duration bet on orbital infrastructure?

Or are they buying the Elon Musk premium?

That distinction matters because each version of SpaceX deserves a different valuation.

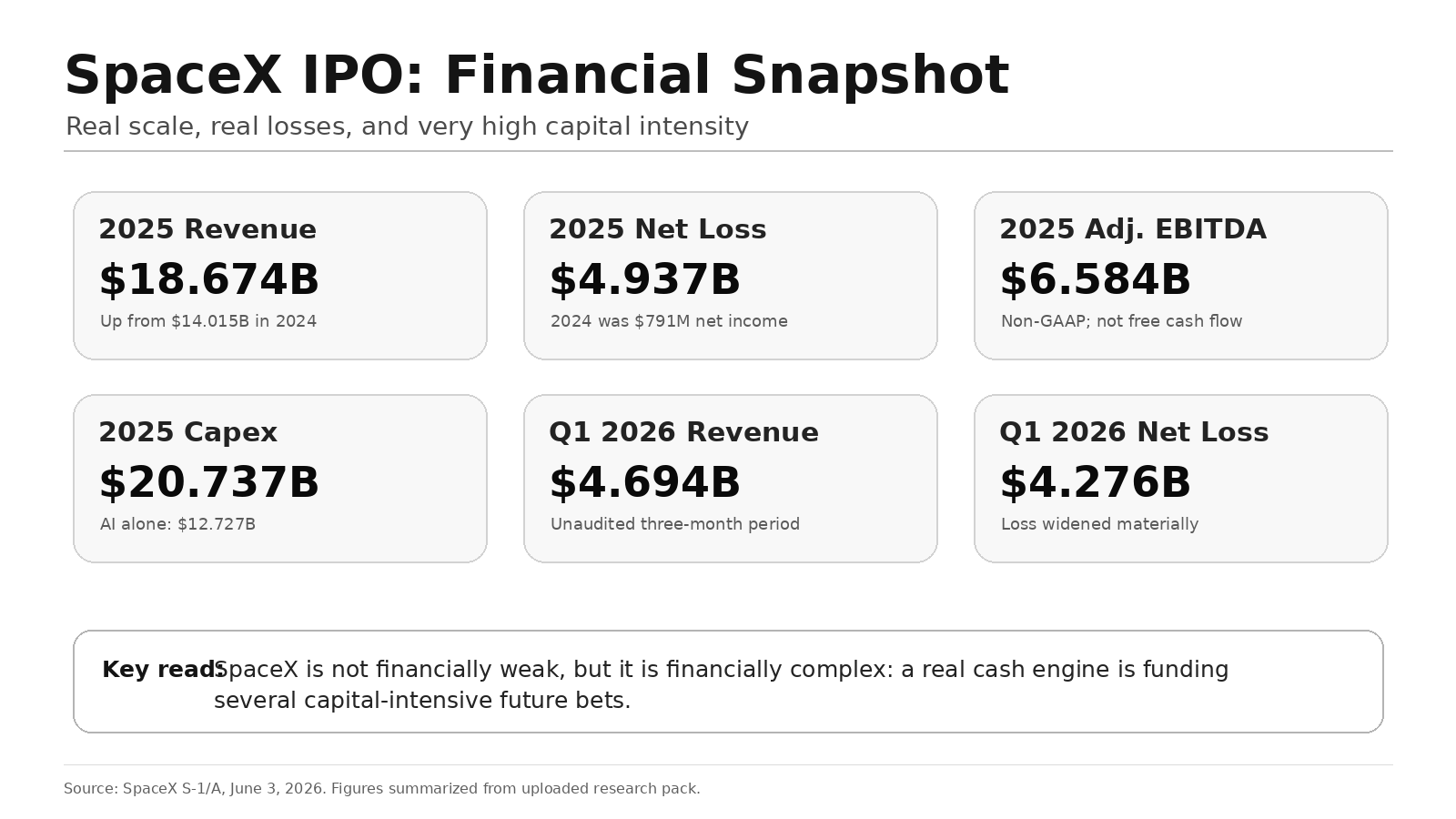

According to SpaceX’s June 2026 S-1/A filing, the company generated $18.674 billion in revenue in 2025, but also reported a $4.937 billion net loss and $20.737 billion of capital expenditures. Adjusted EBITDA was $6.584 billion, but that number excludes substantial depreciation, share-based compensation, and other adjustments.

That is the key tension.

SpaceX is not a concept company.

It has real revenue, real subscribers, real contracts, and real infrastructure dominance.

But it is also not a mature cash-flow compounder.

It is a capital-intensive infrastructure company that is using today’s cash engines to fund several much larger future bets.

That is why the SpaceX IPO is so difficult to value.

The question is not whether SpaceX is an extraordinary company.

The question is how much of its extraordinary future is already priced in.

SpaceX Is Not One Business

The biggest mistake investors can make is to value SpaceX as a simple launch business.

SpaceX does not merely sell rocket launches. It is trying to control the infrastructure layer of space.

That is a much larger ambition.

The company’s flywheel is powerful:

Reusable rockets reduce launch costs.

Lower launch costs make it cheaper to deploy Starlink satellites.

Starlink creates recurring revenue from global connectivity.

That revenue can support more launches, more satellites, Starship development, defense programs, AI infrastructure, and eventually orbital compute.

This is why SpaceX is different from traditional aerospace companies.

Traditional aerospace companies often sell expensive projects to governments.

SpaceX is building a vertically integrated infrastructure system.

It owns the launch capability.

It owns the satellite network.

It owns the customer relationship through Starlink.

It has government and defense relevance.

And now it is trying to connect that physical infrastructure to the AI compute boom.

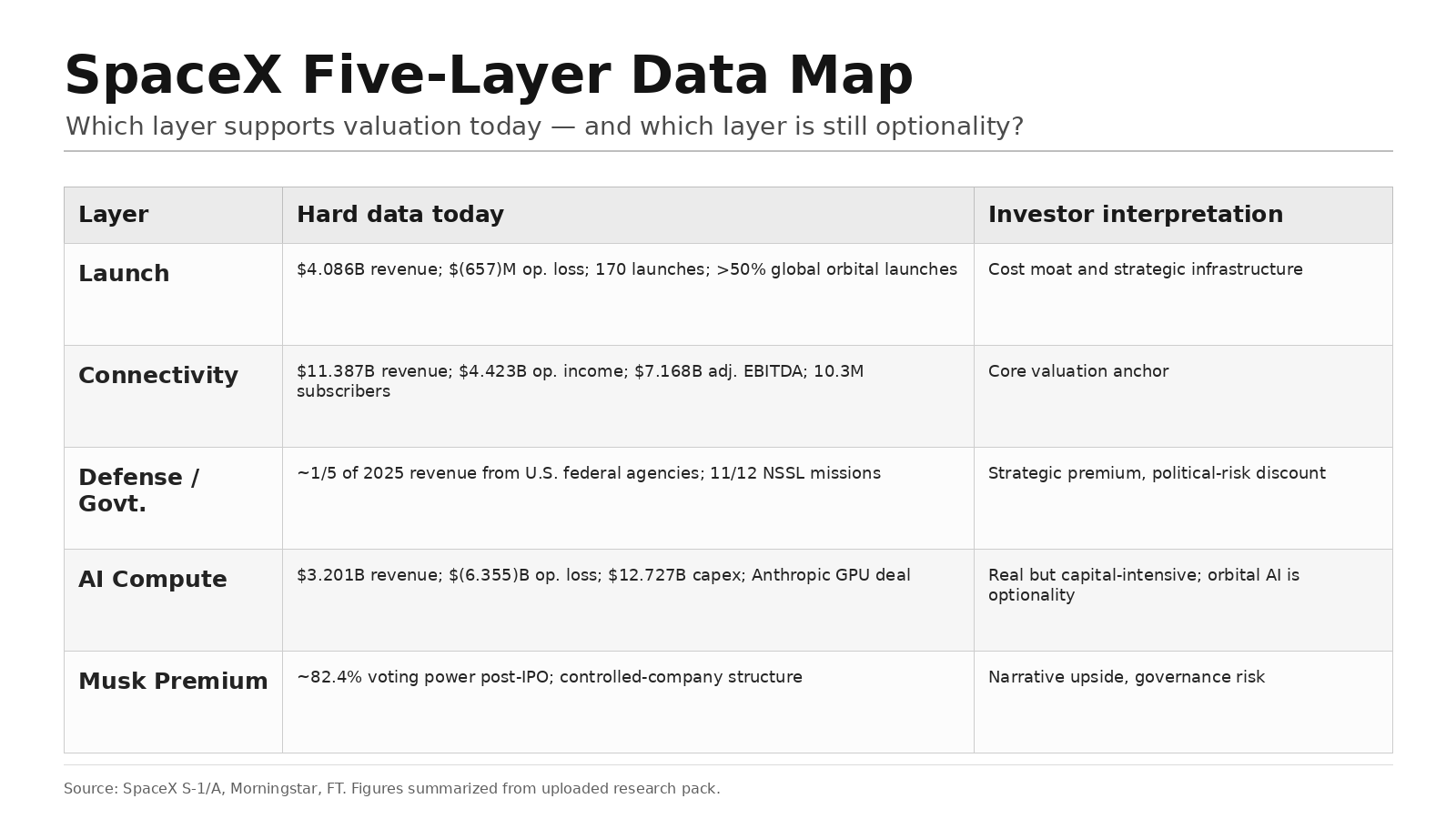

The S-1/A reports SpaceX through three operating segments: Space, Connectivity, and AI.

But from an investor’s perspective, SpaceX is better understood as five valuation layers:

- Launch infrastructure

- Starlink and Connectivity

- Defense and government infrastructure

- AI compute and orbital data centers

- Musk premium

These layers are not equal.

Some already generate strong operating profits.

Some create strategic cost advantages.

Some consume enormous capital.

Some are future options.

And some are narrative premiums that can expand or collapse with market sentiment.

A serious valuation must treat them differently.

The Five Layers of SpaceX — and Their Financial Reality

1. Launch Infrastructure: The Cost Advantage Layer

Launch is the foundation.

Without reliable, low-cost launch capability, the rest of SpaceX would be much weaker.

SpaceX’s reusable rocket advantage gives it a cost and frequency edge that traditional launch providers have struggled to match.

The filing says SpaceX completed 170 launches in 2025, up from 138 in 2024. Falcon 9 performed 165 of those launches and accounted for more than half of global orbital launches. SpaceX also says it delivered more than 80% of global mass to orbit.

Those numbers matter.

They show that SpaceX does not merely participate in the launch market. It dominates launch frequency and mass delivery.

But the financial role of launch is more complicated than it looks.

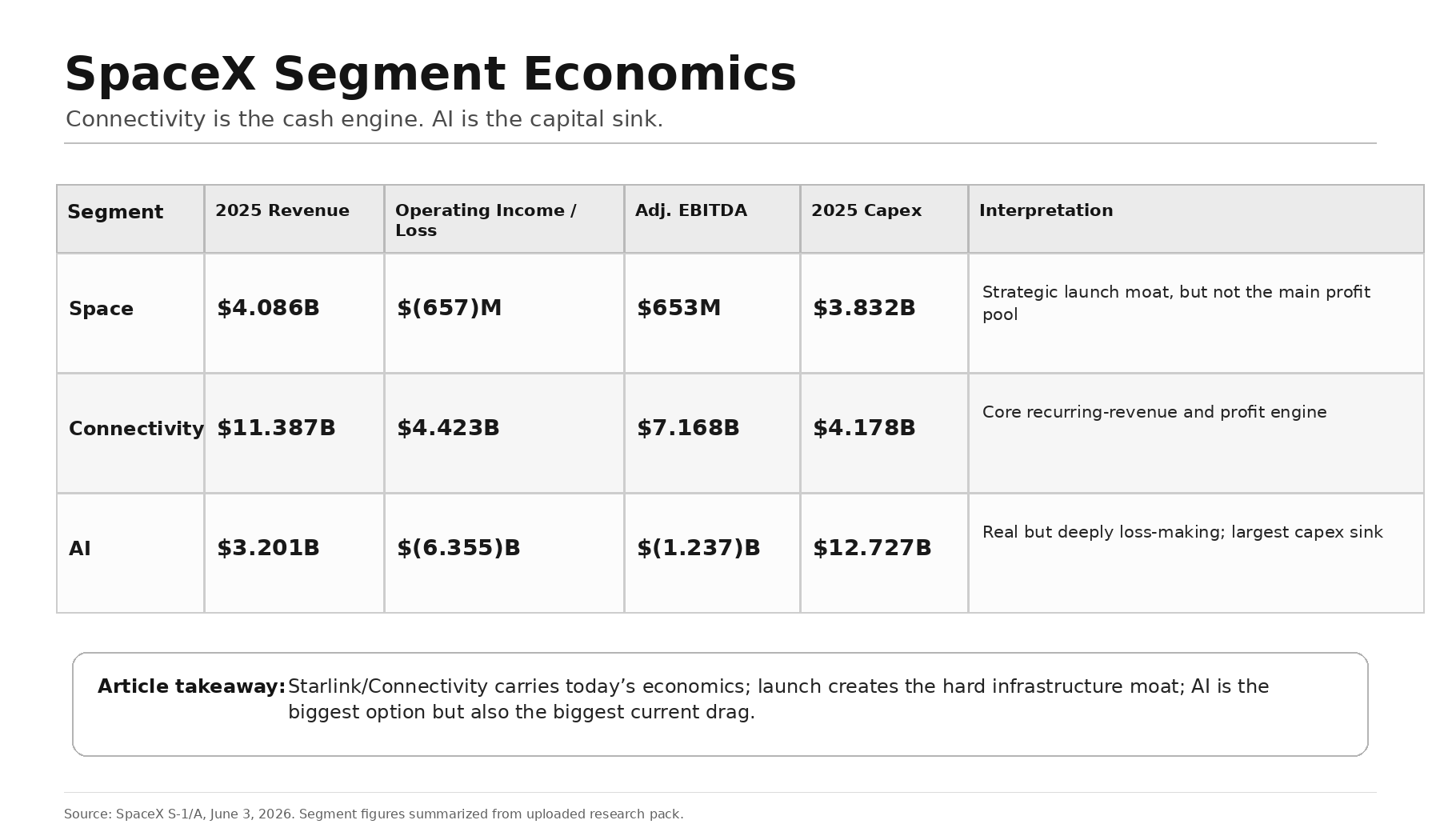

In 2025, the Space segment generated $4.086 billion of revenue. That included $2.576 billion from launch services and $1.510 billion from launch and development. But the segment still posted a $657 million operating loss, even though segment adjusted EBITDA was positive at $653 million.

This means launch is not currently the cleanest profit engine inside SpaceX.

Its more important role is strategic.

Launch is both a revenue business and a cost moat.

For external customers, SpaceX earns launch revenue.

For its own system, SpaceX lowers the cost of deploying Starlink satellites, defense payloads, and future orbital infrastructure.

That second point may be even more important.

Every Starlink satellite launched on a SpaceX rocket is a satellite SpaceX does not need to pay another launch provider to carry. Every improvement in launch cost can improve the economics of Starlink, Starship, defense missions, and future orbital AI infrastructure.

This is why launch should not be valued like a software business.

It is capital-intensive. It requires rockets, engines, launch facilities, manufacturing capacity, regulatory approvals, insurance, and constant reinvestment.

But it does deserve an infrastructure premium.

SpaceX also disclosed that Falcon 9’s original cost to orbit was about $2,700 per kilogram, which the filing says was roughly 85% below a historical NASA benchmark. It also disclosed that a Falcon 9 first stage has been reflown up to 34 times.

That is the real launch advantage.

Not just market share.

Not just revenue.

The real value is cost curve control.

Launch is the road to space.

SpaceX owns the road.

The valuation implication is clear:

Launch deserves a strategic infrastructure premium, but not a software multiple.

The bull case is not that launch fees alone make SpaceX worth more than one trillion dollars.

The bull case is that launch dominance gives SpaceX a lower cost curve across everything else it wants to build.

This is where Starship becomes important.

Falcon supports the current business.

Starship supports the long-term valuation dream.

If Starship becomes rapidly reusable at scale, it could lower the cost of deploying satellites, orbital hardware, and future space infrastructure.

If Starship is delayed or fails to reach the economics investors expect, many of SpaceX’s most ambitious future businesses become harder to justify.

SpaceX’s short-term financial base is Starlink.

Its long-term valuation leverage is Starship.

2. Starlink and Connectivity: The Real Cash Engine

Starlink is currently the most important financial asset inside SpaceX.

It changes the entire valuation debate.

Without Starlink, SpaceX would be much harder to value. Investors would mostly be paying for launch dominance, government contracts, Starship, and long-term space ambitions.

With Starlink, SpaceX has a recurring revenue engine.

The company is no longer only selling access to space.

It is selling internet access to consumers, enterprises, ships, aircraft, governments, remote regions, and military users.

The financial evidence is clear.

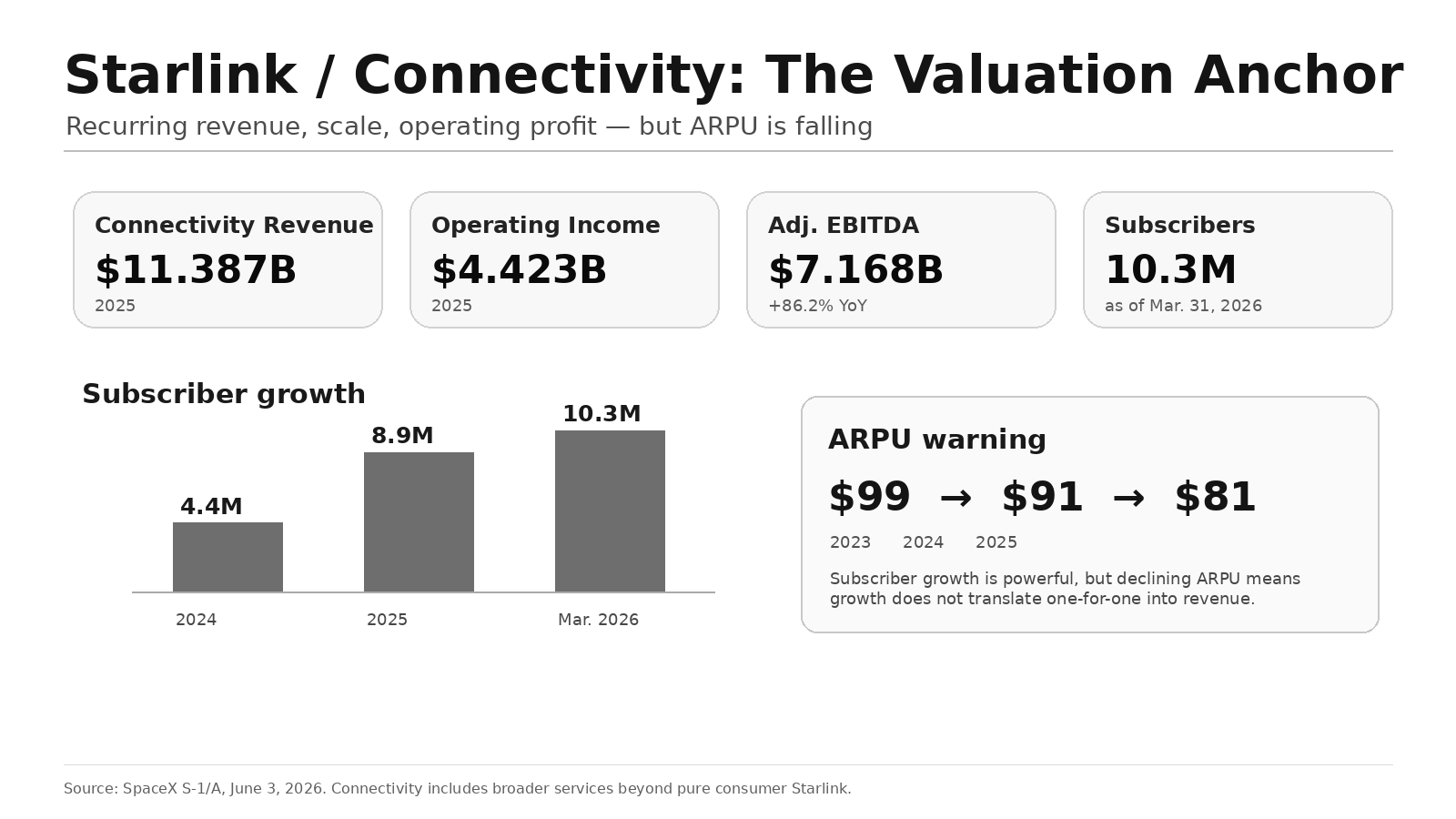

In 2025, SpaceX’s Connectivity segment generated $11.387 billion of revenue, representing about 61% of consolidated revenue. It produced $4.423 billion of operating income and $7.168 billion of segment adjusted EBITDA.

This is the strongest financial segment in the company.

Connectivity is not just the growth story.

It is the economic core.

The subscriber data also matters.

Starlink had 4.4 million subscribers at the end of 2024, 8.9 million subscribers at the end of 2025, and 10.3 million subscribers by March 31, 2026. Those subscribers were spread across 164 countries and other markets.

That is real scale.

But there is also an important warning inside the data.

Starlink’s 2025 ARPU was $81 per month, down from $91 in 2024 and $99 in 2023.

That means subscriber growth does not automatically translate into the same level of revenue growth.

As Starlink expands into more markets and lower-income regions, ARPU may continue to decline.

This is not necessarily bad.

Lower ARPU can still be profitable if scale, satellite utilization, and launch cost improve.

But investors should not assume that user growth alone solves the valuation question.

Starlink’s real financial questions are:

How high can long-term margins go?

How often must satellites be replaced?

How expensive is customer acquisition?

How much capacity is available per region?

Can Starlink maintain premium pricing in high-value markets?

Can it grow beyond low-density markets without competing directly against cheaper terrestrial networks?

This is where the market size question becomes important.

Starlink is strongest where terrestrial networks are weak, unavailable, fragile, or strategically insufficient.

Rural areas.

Maritime routes.

Aviation.

Disaster zones.

Military operations.

Remote industrial sites.

Developing markets.

Starlink is not necessarily the best internet for dense cities where fiber, cable, and 5G already work well.

The better way to understand Starlink is this:

It is not the internet for everyone.

It is the best internet for places where existing internet infrastructure is poor, unreliable, too expensive, or strategically vulnerable.

That is still a huge market.

But it is not unlimited.

This distinction matters for valuation.

If investors value Starlink as a high-growth edge-connectivity platform, the business can be seriously analyzed.

If they value it as a replacement for all terrestrial broadband, they may be paying for a market that does not really exist.

Starlink is the clearest valuation anchor inside SpaceX.

Launch dominance is strategic.

Starship is transformational.

AI compute is optionality.

Mars is narrative.

But Starlink is the financial core.

If Starlink compounds profitably, SpaceX has a much stronger valuation base.

If Starlink’s market size or margins disappoint, investors will be forced to rely more heavily on Starship, AI compute, and the Musk premium.

That would make the valuation much more fragile.

3. Defense and Government Infrastructure: The Strategic Premium Layer

SpaceX is not only a commercial company.

It is increasingly part of strategic infrastructure.

Launch systems, satellite networks, military communications, disaster response, and national security all make SpaceX more important than a normal private-sector business.

This layer does not need to look like a consumer internet business to be valuable.

Its value comes from strategic importance, contract durability, customer credit quality, and the difficulty of replacing the provider.

The filing gives several important data points.

SpaceX launched 11 of 12 medium and heavy national-security missions under the National Security Space Launch program in 2025. It also launched all five U.S. crew and cargo missions to the International Space Station that year.

The filing also says approximately one-fifth of SpaceX’s 2025 revenue came from U.S. federal agencies.

That is a meaningful exposure.

It supports the idea that SpaceX is not only a private growth company. It is also becoming part of U.S. strategic infrastructure.

But this layer is a double-edged sword.

Government exposure creates a moat.

It also creates political risk.

Defense contracts can be durable, but they are not politically neutral.

Starlink can be valuable in conflict zones, but that also makes it sensitive.

National security relevance can protect a company, but it can also invite regulatory scrutiny, audits, procurement risk, funding delays, and political controversy.

There is also a disclosure issue.

The filing does not fully separate government revenue by NASA, Department of Defense, Space Force, Starshield, or other programs.

That means investors should not treat defense and government exposure as a fully transparent standalone profit center.

The right conclusion is not simply “government contracts are good.”

The better conclusion is:

Government exposure gives SpaceX strategic value, but it also makes SpaceX politically non-neutral.

The valuation implication is clear:

Defense and government infrastructure deserve a strategic premium, but they also deserve a political-risk discount.

4. AI Compute and Orbital Data Centers: The Option Layer

The newest version of the SpaceX story is AI infrastructure.

This is the most exciting part of the IPO pitch.

It is also the easiest part to overvalue.

AI data centers on Earth face real bottlenecks: electricity, cooling, land, permitting, grid interconnection, and geographic concentration.

SpaceX’s long-term idea is that orbital infrastructure could eventually become a new compute layer.

Instead of only building data centers on Earth, SpaceX could deploy computing systems in orbit.

That connects SpaceX directly to the AI infrastructure trade.

Nvidia represents the compute engine.

Optical networking companies represent data movement.

Power and cooling companies represent the physical constraints of AI factories.

SpaceX represents a more speculative possibility: that the next layer of infrastructure may extend beyond Earth.

But the financial reality is very different from the story.

AI is already a reportable segment, but it is currently a heavy capital sink.

In 2025, SpaceX’s AI segment generated $3.201 billion of revenue, including $1.844 billion from advertising and $1.357 billion from AI Solutions and Infrastructure. But the segment reported a $6.355 billion operating loss and negative $1.237 billion of segment adjusted EBITDA.

It also consumed $12.727 billion of capital expenditures in 2025, more than the Space and Connectivity segments combined.

This is the key point:

AI is real, but it is not yet a mature profit engine.

It is the largest current capital sink inside the company.

The filing also discloses a major Anthropic agreement. The May 2026 agreements cover access to approximately 325,000 NVIDIA GPUs and specify $1.25 billion of monthly payments through May 2029, subject to ramp provisions and termination rights.

That makes the AI segment more tangible than a vague story.

There is real compute infrastructure.

There is a real customer relationship.

There is real revenue potential.

But investors still need to separate terrestrial AI infrastructure from orbital AI compute.

Terrestrial AI compute is already commercial.

Orbital AI compute is not.

The filing targets initial orbital AI compute satellite deployments as early as 2028. It does not disclose current orbital-compute revenue.

The risk factors are serious: radiation, thermal cycling, debris, limited repairability, shortened useful lives, replacement capital expenditures, bandwidth, latency, and operating conditions no one has proven at scale.

Orbital AI compute depends on Starship.

It depends on launch cost.

It depends on satellite manufacturing.

It depends on cooling.

It depends on repair economics.

It depends on customer demand.

It may become a real business.

But today, it should be treated as optionality, not as the core valuation anchor.

A future option can be valuable.

But it should not be valued like current earnings.

If orbital AI compute becomes commercially viable, it could expand SpaceX’s addressable market dramatically.

If it remains technically possible but economically unattractive, investors who paid for it upfront may be disappointed.

The valuation implication is simple:

Terrestrial AI is real but deeply loss-making.

Orbital AI is a powerful call option.

Neither should be treated as proven cash-flow support for a $1.75 trillion valuation.

5. The Musk Premium: The Narrative and Governance Layer

The Musk premium is real.

It is also unstable.

Elon Musk has repeatedly shown an ability to turn difficult engineering missions into capital market narratives. Tesla proved that markets can assign enormous value to a founder-led company with a huge future vision.

But the Musk premium is not the same as a margin of safety.

It can expand valuation in bull markets.

It can also magnify downside when expectations change.

This is especially important because SpaceX is not isolated from Musk’s broader ecosystem.

Tesla, xAI, X, Neuralink, and other Musk-controlled companies create both strategic possibilities and governance questions.

Could SpaceX benefit from AI demand across the Musk ecosystem?

Possibly.

Could conflicts of interest, management distraction, or related-party complexity become risks?

Also possibly.

The filing also makes the control structure clear.

Musk is expected to retain approximately 82.4% of voting power after the IPO. SpaceX would be a controlled company under Nasdaq rules.

That does not automatically make the company uninvestable.

Founder control can support long-term decision-making.

But it also means outside shareholders will have limited control over governance.

The financial reality is simple:

The Musk premium is not a revenue line.

It is not free cash flow.

It is not a replacement for unit economics.

It is a capital-market premium attached to a founder, a mission, and a track record.

That premium may be justified.

But it cannot be treated as downside protection.

Founder premium and key-person risk are the same coin.

Investors cannot accept one and ignore the other.

The valuation implication is clear:

The Musk premium can lift valuation, but it cannot replace cash flow.

A Simple Map of the Five Layers

The cleanest way to understand SpaceX is to separate the layers by financial quality.

This is the key point:

SpaceX has five powerful layers, but not all five have the same financial evidence today.

Starlink is the financial core.

Launch is the cost moat.

Defense is the strategic premium.

AI is the capital-intensive option.

The Musk premium is the narrative accelerator.

A good valuation must treat them differently.

The Financial Picture: Strong, but Not Simple

SpaceX is financially stronger than a concept company, but weaker than a mature cash-flow compounder.

In 2025, SpaceX generated $18.674 billion of revenue, up from $14.015 billion in 2024.

But profitability moved in the opposite direction.

The company went from $791 million of net income in 2024 to a $4.937 billion net loss in 2025.

Operating income also deteriorated, moving from $466 million of operating income in 2024 to a $2.589 billion operating loss in 2025.

Adjusted EBITDA rose from $5.350 billion in 2024 to $6.584 billion in 2025.

That sounds positive.

But investors should be careful.

Adjusted EBITDA is not free cash flow.

The filing shows $6.701 billion of depreciation and amortization in 2025, and capital expenditures of $20.737 billion.

This is why SpaceX cannot be valued like a software company.

The company is scaling revenue, but also scaling capital intensity.

The same pattern continued into Q1 2026.

Revenue was $4.694 billion.

Net loss was $4.276 billion.

Operating loss was $1.943 billion.

Adjusted EBITDA was $1.127 billion.

This is not a simple story of profitable growth.

It is a story of one very profitable segment funding several very expensive growth ambitions.

The segment data makes that clear.

Connectivity generated $4.423 billion of operating income in 2025.

Space lost $657 million.

AI lost $6.355 billion.

In other words:

Starlink and Connectivity are carrying the economic story.

Launch supports the moat.

AI is consuming capital.

That is not necessarily bad.

Many great infrastructure companies require enormous upfront investment.

But it does mean investors must be precise.

SpaceX is not financially weak.

But it is financially complex.

Its cash engine is real.

Its capital needs are also real.

The Valuation Problem

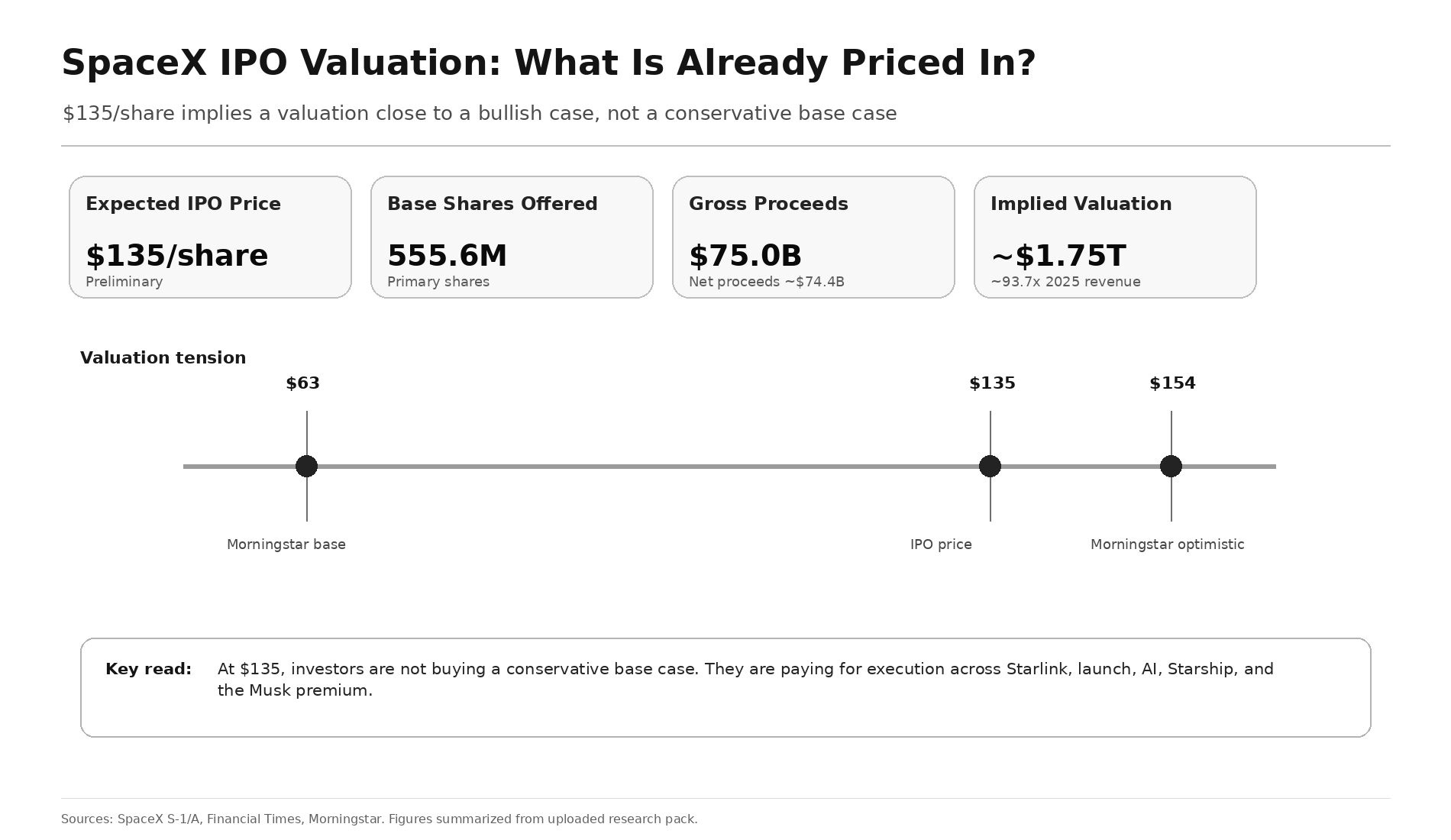

The preliminary IPO price is $135 per share.

The company is offering 555,555,555 primary shares, implying roughly $75 billion of gross proceeds and about $74.4 billion of estimated net proceeds.

Financial Times reported that the offering would value SpaceX at approximately $1.75 trillion.

At that valuation, SpaceX would trade at roughly 93.7 times 2025 revenue.

That is an extraordinary multiple for a capital-intensive infrastructure company.

It implies that investors are not only paying for what SpaceX is today.

They are paying for several future businesses at once.

They are paying for:

Starlink growth.

Launch dominance.

Defense infrastructure.

Starship success.

Terrestrial AI contracts.

Orbital AI compute.

Mars ambition.

And the Musk premium.

That does not automatically make the valuation wrong.

But it makes the margin of safety thin.

Morningstar estimated SpaceX’s fair value at $63 per share, or roughly $780 billion of equity value. Its optimistic scenario is $154 per share.

That is a useful range.

The base-case valuation is far below the expected IPO price.

The optimistic case is above it.

This tells us something important:

At $135 per share, investors are not paying for a conservative base case.

They are paying for something much closer to a bullish execution case.

That does not mean the IPO is doomed.

It means the price already assumes a lot.

SpaceX can be a great company and still be expensive.

In fact, that is often where investors make the biggest mistakes.

They confuse business quality with investment quality.

Business quality asks: is this company extraordinary?

Investment quality asks: what price am I paying for that extraordinary future?

For SpaceX, the answer to the first question may be yes.

The answer to the second question is much harder.

A Better Way to Think About SpaceX’s Valuation

Investors should not ask only:

Is SpaceX worth $1.75 trillion?

That question is too simplistic.

The better question is:

Which parts of SpaceX can support that valuation?

Starlink and Connectivity should carry the highest valuation weight because they have the clearest revenue, operating income, subscriber base, and adjusted EBITDA.

Launch should be valued as strategic infrastructure and a cost moat, not as a standalone high-margin software-like business.

Defense and government exposure should receive a strategic premium, but also a political-risk discount.

AI should be split into two pieces.

Terrestrial AI infrastructure is real, but deeply loss-making and capital-intensive.

Orbital AI compute is a future option, not current earnings power.

Mars should be treated as narrative value, not as a core valuation pillar.

The Musk premium can explain why investors are willing to pay more, but it should not be mistaken for downside protection.

This leads to a clear conclusion:

If most of SpaceX’s valuation is supported by Starlink, launch dominance, and defense infrastructure, the valuation can be seriously debated.

If most of the valuation depends on AI optionality, Mars, and the Musk premium, the safety margin becomes much thinner.

That is the line investors need to draw.

IPO Size Matters

A mega IPO does not just create a new stock.

It forces capital to choose.

That is why the size of the SpaceX IPO matters.

A $75 billion offering is not a normal capital raise.

It is a market event.

The structure is important.

The S-1/A describes the IPO as a primary offering by the company. That means the base shares are offered by SpaceX, not by named selling shareholders.

That is better than a pure insider liquidity event.

It means the proceeds can support the company’s growth projects.

But it also means the market must absorb a very large amount of new equity.

A $75 billion primary offering removes liquidity from the market.

Even if demand is strong, investors must fund it somehow.

Some funds may reduce exposure to other high-growth technology names.

Some individual investors may sell portions of Nvidia, Tesla, Palantir, crypto, or smaller AI infrastructure stocks to participate.

Some institutions may rebalance growth portfolios.

That does not mean Nvidia is broken.

It does not mean AI infrastructure is over.

It simply means SpaceX could become a new magnet for growth capital.

The SpaceX IPO may not end the AI trade.

But it can compete with AI stocks for capital in the short term.

The Index Question

There is another market issue investors should not ignore: index inclusion.

If SpaceX becomes one of the largest public companies in the United States shortly after listing, it may eventually become relevant for major indexes.

That could create passive buying pressure.

But it could also force portfolio rebalancing.

Business Insider reported that revised Nasdaq-100 rules could make a very large IPO eligible rapidly, though actual inclusion remains discretionary and not guaranteed. The same report cited an analyst estimate that potential passive buying could reach around $36 billion.

This is not an official index forecast.

It is scenario analysis.

But it matters because SpaceX is not only a stock offering.

It is a potential index event.

This does not determine whether the stock is a good long-term investment.

But it can affect short-term market structure.

A company can be fundamentally attractive and still create temporary pressure on other crowded assets simply because capital has to be reallocated.

Should Investors Buy on Day One?

The most honest answer is:

Only if they know which version of SpaceX they are buying.

Buying SpaceX on the first day is not simply buying a great company.

It is buying a highly valued, capital-intensive, founder-controlled infrastructure company with several unproven but enormous growth options.

That may be attractive for investors with a ten-year horizon and high risk tolerance.

But it is dangerous for investors who are only chasing the next famous ticker.

The worst reason to buy SpaceX is fear of missing out.

The second worst reason is selling a company you understand deeply to buy a company you have not valued.

The real risk is not missing SpaceX.

The real risk is paying for every possible future before the company has proven which ones will become real cash flow.

Our View

SpaceX deserves to be studied seriously.

Not because it is automatically cheap.

Not because every Elon Musk company deserves a premium.

Not because space is an exciting story.

SpaceX deserves serious research because it may redefine what an infrastructure company can be.

Traditional infrastructure means railroads, ports, power grids, telecom towers, and data centers.

SpaceX is trying to build a new infrastructure stack:

Launch infrastructure.

Satellite internet.

Defense communications.

AI compute.

Orbital data centers.

Possibly interplanetary transport.

That is why the company can command such an extraordinary valuation.

But that is also why the valuation is risky.

The market is not only paying for what SpaceX is today.

It is paying upfront for several futures that have not yet been fully proven.

Our conclusion is simple:

SpaceX may deserve an infrastructure premium.

But investors should be careful not to pay a fantasy premium.

At the current expected IPO valuation, Starlink and Connectivity are the strongest financial foundation.

Launch is the cost moat.

Defense is the strategic premium.

AI is real but capital-intensive.

Orbital compute is still an option.

Mars is still narrative.

The Musk premium is powerful, but it is not cash flow.

The right question is not whether SpaceX is a great company.

It probably is.

The right question is:

Which future are investors paying for?

The cash-flow SpaceX?

The infrastructure SpaceX?

The AI-option SpaceX?

The Mars-narrative SpaceX?

Or the Musk-premium SpaceX?

If investors cannot answer that question, they are not investing in SpaceX.

They are buying the story.

And stories can be powerful.

But valuation decides whether a powerful story becomes a great investment.

Sources

- Space Exploration Technologies Corp. Form S-1/A, SEC, June 3, 2026.

- Morningstar, “5 Things Investors Should Know Before Buying SpaceX Stock,” May 21, 2026.

- Financial Times, “SpaceX files to raise $75bn in world’s biggest IPO,” May 20, 2026.

- Business Insider, “SpaceX could join the Nasdaq 100 just days after its IPO,” June 5, 2026.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-10 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments