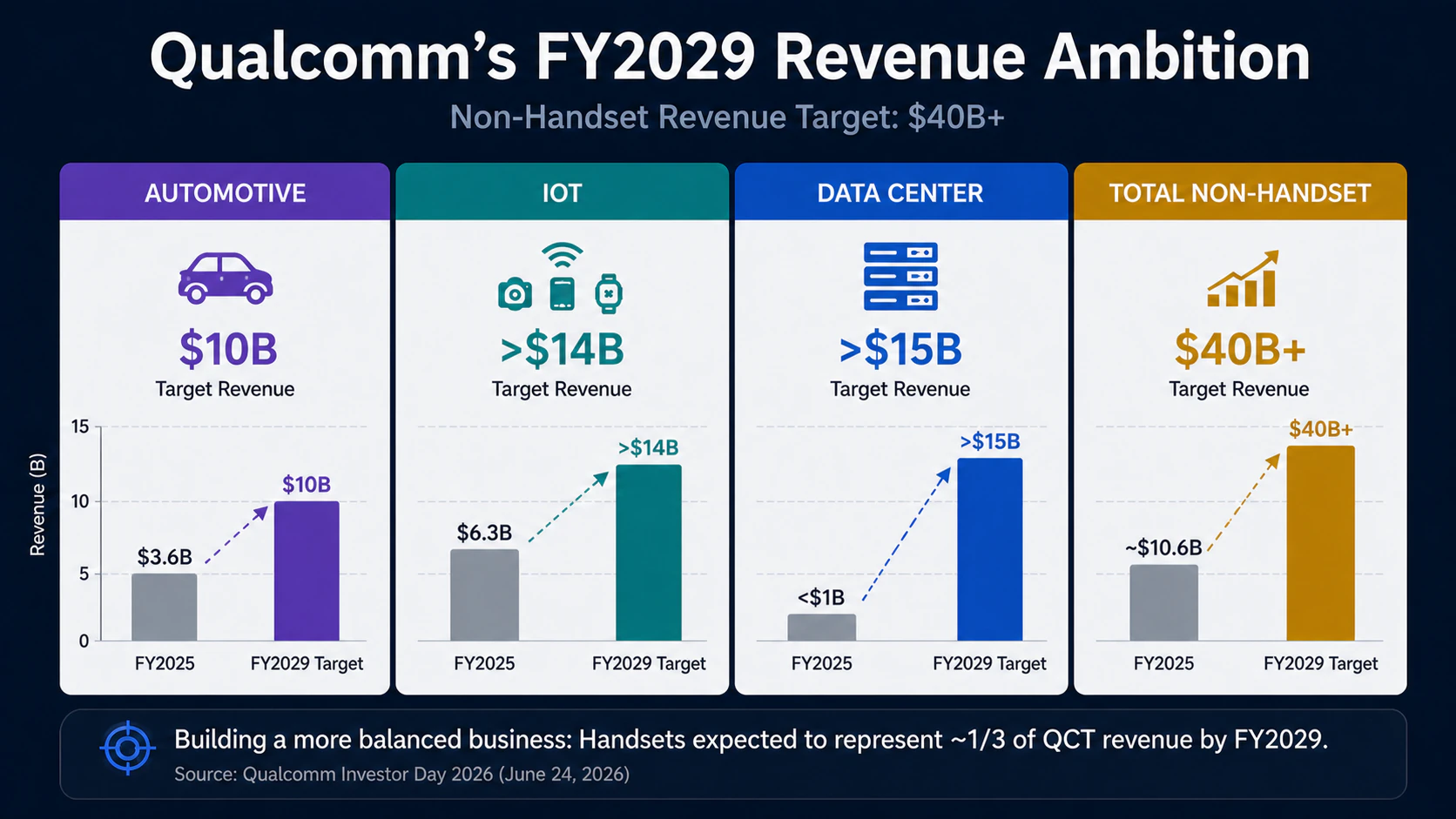

Qualcomm’s latest Investor Day presented a company that looks increasingly different from the one investors have followed for the past two decades. Management raised its fiscal 2029 non-handset revenue target to $40 billion, set a goal of more than $15 billion from data centers, increased its automotive target to $10 billion, and expanded its automotive design-win pipeline to $65 billion. Robotics and industrial AI were positioned as part of the next wave of Physical AI, while the new Dragonfly portfolio extended Qualcomm’s computing roadmap from edge devices into large-scale data centers.

Despite that broader strategy, Qualcomm currently trades at roughly 19 times trailing earnings. The shares were recently around $178, with a market capitalization of approximately $191 billion.

That apparent contradiction has encouraged a familiar argument: Qualcomm is being valued as a smartphone supplier even though it is becoming an AI infrastructure company. There is some truth to that view, but it gets the order of evidence wrong. Qualcomm has expanded its addressable markets and established credible product roadmaps. It has not yet changed the financial structure that determines how the market values the business.

The existing valuation reflects the company Qualcomm is today. A higher multiple will depend on whether management can convert its Investor Day targets into revenue, operating profit, and cash flow over the next several years.

Qualcomm’s Earnings Are Still Governed by the Handset Cycle

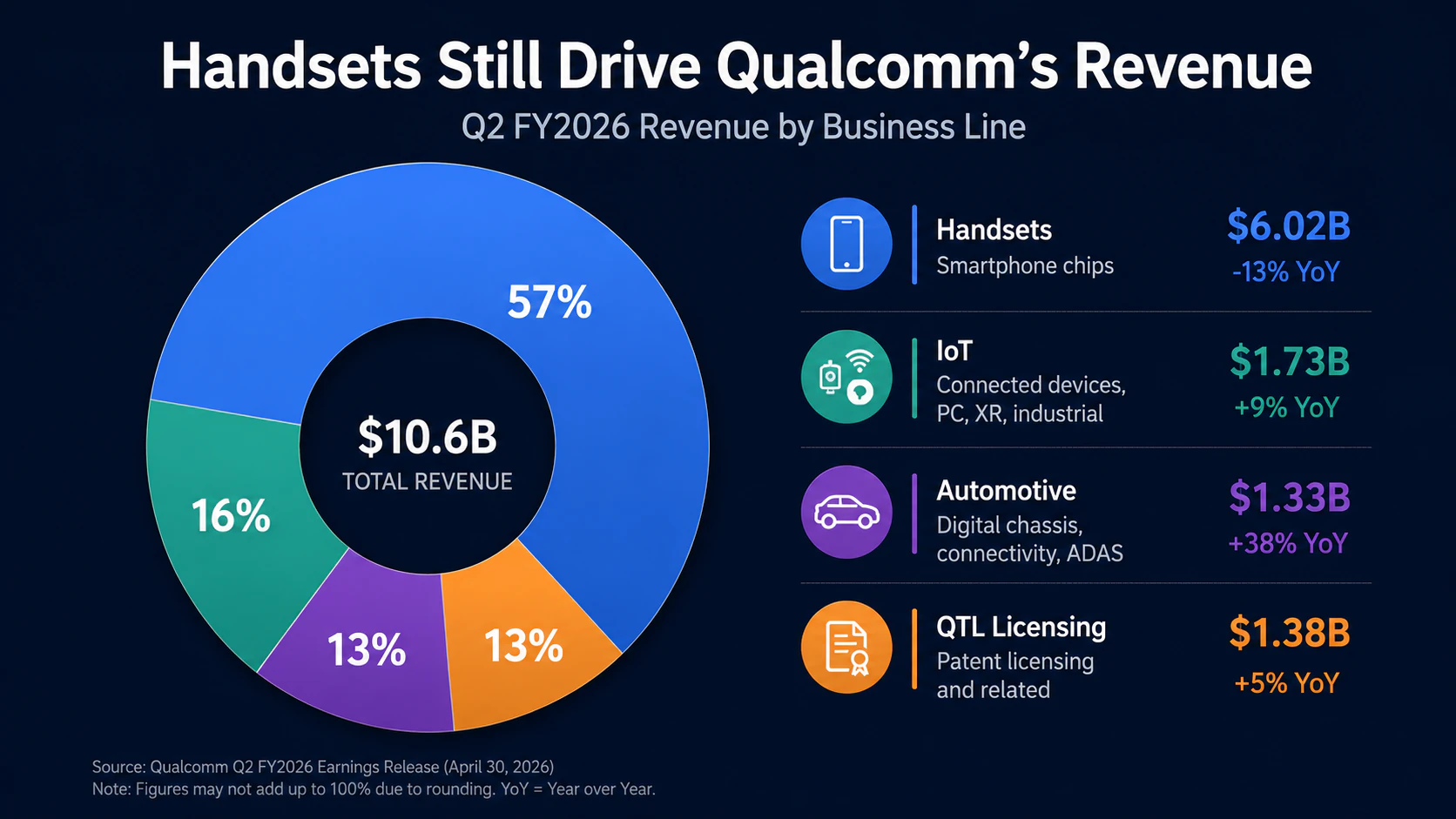

Qualcomm reported fiscal second-quarter revenue of $10.6 billion. The mix remained heavily dependent on handsets, while automotive and IoT were smaller but faster-growing businesses. QTL continued to provide a high-margin licensing foundation.

The diversification businesses are no longer immaterial. Automotive set a quarterly record, while combined automotive and IoT revenue increased 20% year over year. The problem is one of scale. The approximately $367 million year-over-year increase in automotive revenue and $145 million increase in IoT revenue were not enough to offset a roughly $905 million decline in handset revenue.

As a result, QCT revenue fell 4%. QCT earnings before tax declined more sharply, and the segment’s EBT margin fell from 30% to 27%. Qualcomm attributed the decline to lower revenue, higher operating expenses and product costs, partially offset by higher average selling prices.

This is the financial reason Qualcomm continues to trade like a mature handset semiconductor company. Investors have recognized the growth in automotive and IoT, but those businesses have not yet become large enough to prevent weakness in handsets from reducing total chip revenue and margins.

The QTL licensing segment provides an important earnings and cash-flow foundation. It generated $994 million of earnings before tax on $1.38 billion of revenue in the quarter, implying an EBT margin of roughly 72%. Yet licensing is also a relatively mature business. Its high profitability supports the valuation floor, but it does not by itself justify the multiple normally assigned to a company with rapidly expanding AI infrastructure revenue.

Qualcomm’s current valuation therefore reflects a mix of high-margin licensing, a large but cyclical handset franchise, and diversification businesses whose growth has not yet fully reached consolidated earnings.

Investor Day Raised the Growth Ceiling—and the Execution Burden

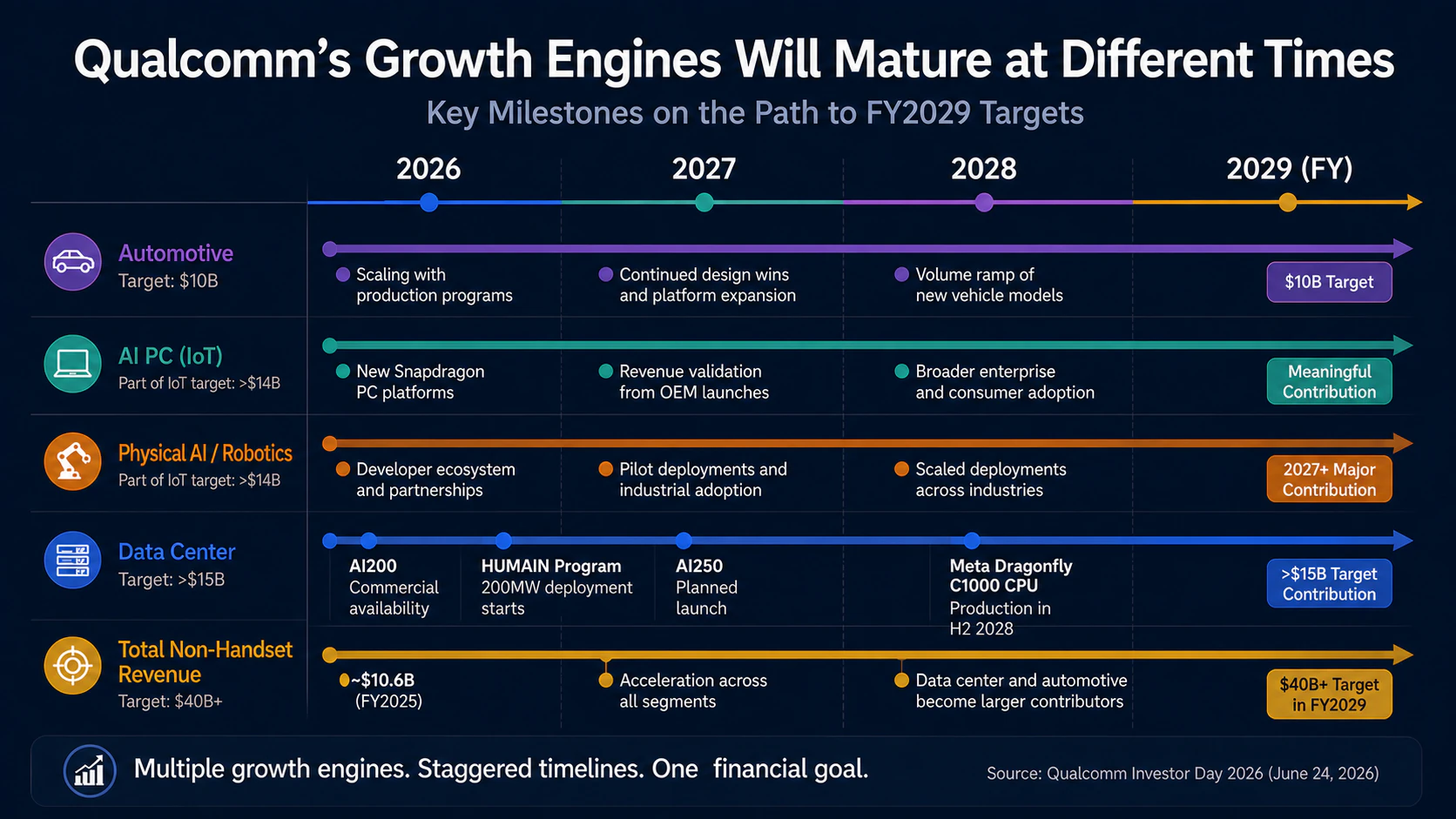

The most consequential feature of Qualcomm’s Investor Day was the scale of the 2029 targets. Management now expects non-handset revenue to reach $40 billion, approximately twice its previous target. That total includes more than $15 billion from data centers and $10 billion from automotive, with the remainder coming largely from IoT-related categories such as computing, industrial equipment, networking and robotics.

The objective is to reduce the extent to which the handset cycle controls QCT’s growth. Qualcomm is not forecasting a return to structurally high smartphone-unit growth. It is attempting to reuse the same underlying technologies—power-efficient computing, on-device AI, connectivity and system integration—across a much broader set of markets.

That distinction matters. A new product in an adjacent market may add revenue without changing how the company is valued. A new business capable of contributing several billion dollars of recurring revenue and operating profit can change the earnings mix, reduce cyclicality and support a higher multiple.

The 2029 roadmap describes that second outcome. The open question is whether the route from current results to those targets is sufficiently visible.

Automotive already has meaningful revenue and a multi-year production pipeline. IoT has scale but combines several businesses with different growth rates and competitive positions. Physical AI remains largely a design-win and product-development opportunity. Data center products offer the largest potential increase in revenue, but most of the associated financial contribution lies ahead.

Treating all four areas as equally mature would overstate the progress of Qualcomm’s transformation.

Automotive Is Already a Business, Not a Valuation Narrative

Automotive is the strongest evidence that Qualcomm can move beyond smartphones. Quarterly automotive revenue reached $1.33 billion, up 38% from the prior year. At the latest quarterly run rate, the business has already exceeded $5 billion on an annualized basis.

Reaching the fiscal 2029 target of $10 billion would require Qualcomm to roughly double that annualized level over the next three years. That remains demanding, but it does not require the creation of a new market from a near-zero base. The company already supplies production programs across digital cockpits, connectivity, advanced driver-assistance systems and centralized vehicle computing.

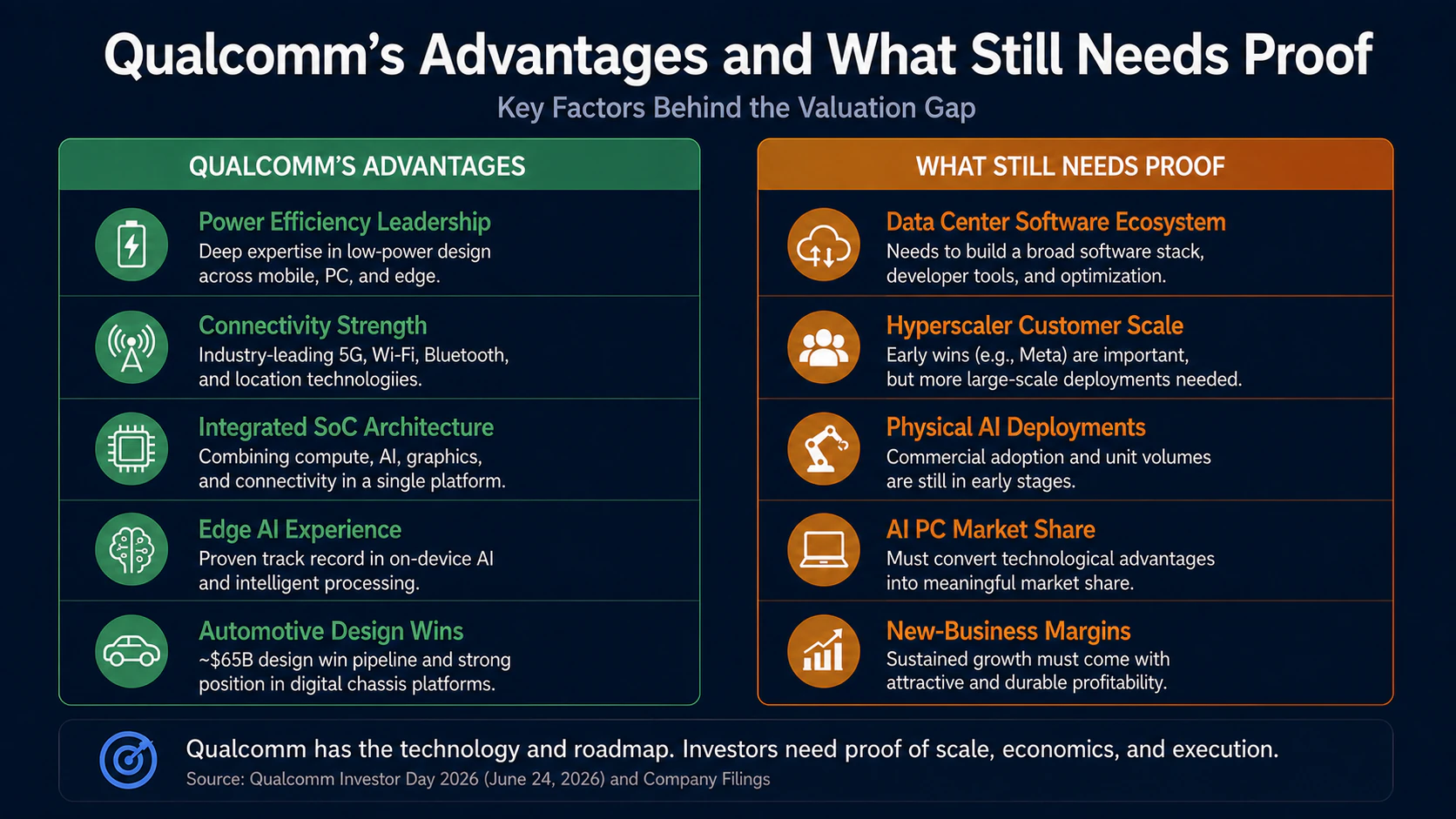

Qualcomm’s competitive position in automotive is based less on dominance in a single chip category than on its ability to combine several functions within the Snapdragon Digital Chassis. Its mobile heritage provides power-efficient processors, cellular connectivity, Wi-Fi, positioning and Android-related software expertise. That combination allows the company to compete for a larger portion of the electronics content in each vehicle.

The competitive landscape remains fragmented and formidable. Nvidia and Mobileye compete for advanced driving and centralized computing workloads. NXP, Texas Instruments and Renesas have entrenched relationships in automotive processing, connectivity and embedded control. Intel and other platform vendors are also pursuing the transition toward software-defined vehicles.

Qualcomm’s $65 billion automotive design-win pipeline indicates that automakers have selected its technology for a substantial number of future programs. It should not be interpreted as contractual backlog. Vehicle programs can be delayed, redesigned or launched at lower-than-expected volumes, and design awards typically convert into revenue over several years.

Even with that qualification, automotive has the best combination of current scale, visible customers and measurable quarterly progress among Qualcomm’s diversification initiatives. It is already contributing to revenue growth. The remaining valuation question is whether the business can preserve attractive margins as it moves into more complex computing and software platforms.

Qualcomm does not separately report automotive operating income, making that question difficult to answer from public segment disclosures. Revenue growth alone will not support a lasting rerating if new automotive products earn materially lower margins than the handset portfolio they are meant to supplement.

Physical AI Extends Qualcomm’s Edge Strategy, but Revenue Visibility Is Limited

Qualcomm’s case in Physical AI rests on a coherent technical premise. Robots, drones, industrial machines and autonomous devices must process sensor data with tight limits on power consumption, thermal output, latency and network availability. Those constraints resemble the engineering problems Qualcomm has spent decades addressing in smartphones.

The company’s edge platforms integrate CPUs, GPUs, neural-processing capabilities and multiple forms of connectivity in a single system. That architecture is relevant to machines that need to perform local inference and control tasks without relying continuously on a cloud data center.

The relevance of Qualcomm’s technology does not settle the commercial question. Physical AI is not yet reported as a distinct revenue category. It is embedded within the wider IoT segment, which also includes consumer devices, networking equipment, PCs and other industrial products. Fiscal second-quarter IoT revenue of $1.73 billion and 9% growth therefore cannot be attributed specifically to robotics or industrial AI.

This reporting structure creates two analytical problems. First, an improvement in IoT revenue could result from a recovery in conventional consumer electronics rather than a new Physical AI adoption cycle. Second, investors cannot yet measure the revenue base, customer concentration or profitability of Qualcomm’s robotics portfolio.

The company also faces competition from businesses with strong positions in adjacent markets. Nvidia’s Jetson platform benefits from its broader AI software ecosystem. NXP and Texas Instruments have long product cycles and established relationships in industrial systems. Other suppliers offer specialized vision, real-time control and embedded processors tailored to individual applications.

Qualcomm’s integrated hardware and connectivity provide a plausible advantage, particularly where energy efficiency and wireless communication are critical. Industrial adoption, however, also depends on software tools, functional safety, long-term product availability, developer support and customer qualification cycles. Strength in mobile hardware does not automatically translate into leadership in industrial automation.

Physical AI should therefore be treated as an extension of Qualcomm’s long-term edge-computing opportunity rather than as a major near-term earnings driver. The first meaningful evidence will come from named customers, production programs, unit deployments and greater disclosure around the composition of IoT growth.

AI PCs Can Be Verified Earlier, but Commercial Adoption Still Matters More Than Specifications

AI PCs sit at an intermediate point between Qualcomm’s established and emerging businesses. Snapdragon processors based on the Oryon CPU and Hexagon NPU give the company a credible Windows-on-Arm platform with advantages in battery life, integrated connectivity and on-device AI processing.

The opportunity is easier to verify than robotics because PC products have shorter launch cycles, visible OEM partners and measurable market-share data. New device generations can begin contributing to revenue within quarters rather than requiring the multi-year production cycle common in automotive and industrial equipment.

The obstacles are equally familiar. PC buyers assess software compatibility, enterprise management, application performance and total platform cost. Intel and AMD retain entrenched relationships with OEMs and corporate customers, while Apple has demonstrated the performance and efficiency benefits of vertically integrated Arm-based PCs within its own ecosystem.

For Qualcomm, the relevant test is not whether Snapdragon-powered laptops can meet benchmark thresholds. It is whether OEM model breadth, unit shipments and enterprise adoption become large enough to alter IoT revenue growth. Management will eventually need to provide more granular evidence—shipment volumes, customer penetration or the revenue contribution from compute—before the market can assign substantial value to the AI PC opportunity.

Over the next four to six quarters, this business should become easier to evaluate. Physical AI will likely take longer because industrial and robotics deployments require more extensive software integration and customer qualification.

Data Centers Represent the Largest Opportunity and the Highest Risk

Qualcomm’s re-entry into data centers is the most important new variable in its valuation. The company has introduced the Dragonfly portfolio, including server CPUs, AI inference accelerators, connectivity products and infrastructure-management software. It is also pursuing custom silicon, giving it a potential route into hyperscaler-specific designs rather than relying exclusively on merchant processors.

The strategy is focused on AI inference, performance per watt, memory capacity and total cost of ownership. That positioning differs from a direct attempt to displace Nvidia in large-scale model training. Qualcomm is trying to apply its expertise in efficient computing to workloads where power consumption, data movement and inference economics have become increasingly important.

AI200 is expected to become commercially available in 2026, followed by AI250 in 2027. Qualcomm has committed to an annual product cadence. The company has also announced a deployment program with HUMAIN targeting 200 megawatts of AI200 and AI250 rack solutions beginning in 2026.

These announcements provide more commercial substance than a product roadmap alone, but they do not yet establish the revenue or profitability needed to support a $15 billion data center target.

The Meta agreement is the clearest validation of Qualcomm’s server CPU strategy. Qualcomm and Meta are collaborating on a multi-generation CPU roadmap, and the first-generation Dragonfly C1000 is scheduled to enter production in the second half of fiscal 2028 for Meta’s future server fleet.

The agreement is significant because a hyperscale customer is incorporating Qualcomm into a long-term infrastructure plan. It validates customer interest and gives Qualcomm a demanding development partner. It does not disclose unit volumes, contract value or expected margins, and the production date means the principal financial impact remains more than two years away.

The data center competition is also considerably stronger than the simple market-growth narrative suggests. Qualcomm will face AMD, Intel, Arm-based processors and hyperscalers’ internal designs in CPUs; Nvidia, AMD and custom accelerators in AI inference; and Broadcom and Marvell in custom silicon and connectivity. Software compatibility, model support, networking, orchestration, data movement and reliability will matter alongside silicon performance.

Qualcomm’s acquisition of Alphawave Semi adds high-speed connectivity and semiconductor IP that can support the data center strategy. The proposed acquisition of Modular, expected to close in the second half of 2026, is intended to strengthen the software layer. Together, these moves indicate that management understands the need to provide more than a processor.

They also increase execution complexity and near-term spending. Qualcomm must integrate acquisitions, develop multiple generations of new chips, build software support and win customers while protecting QCT margins. The fiscal second-quarter filing already showed that higher operating expenses and product costs contributed to lower QCT profitability.

The data center roadmap can materially raise Qualcomm’s long-term earnings ceiling. Before it raises the valuation multiple, investors will need evidence of commercial shipments, additional customers, revenue milestones and margins capable of producing attractive returns on the required research and development.

The Timing of Revenue Matters as Much as the Size of the Targets

Qualcomm’s new businesses are not operating on the same schedule.

Automotive is already in the revenue-conversion phase. Its performance can be evaluated each quarter through reported sales growth, customer launches and the conversion of design wins into production.

AI PCs are in an early scaling phase. They could become visible in the IoT segment over the next several quarters, but Qualcomm needs broader commercial adoption and clearer disclosure.

Robotics and industrial Physical AI remain largely in the design and deployment phase. Meaningful consolidated financial contribution is more likely to emerge from fiscal 2027 onward than in the current quarter.

Data center revenue should arrive in stages. AI200 commercial availability and the HUMAIN program can provide initial accelerator revenue beginning in 2026. AI250 follows in 2027. Meta’s Dragonfly C1000 production is scheduled for the second half of fiscal 2028. The largest part of the data center target is therefore likely to be concentrated toward fiscal 2028 and 2029 rather than spread evenly across the next three years.

This back-end-loaded schedule helps explain why the market has not fully capitalized the 2029 targets. The farther a revenue opportunity lies in the future, the more time competitors have to respond and the greater the uncertainty around product execution, pricing and customer adoption.

A $15 billion revenue target may justify substantial value if it develops into a high-margin and defensible franchise. The same target deserves far less weight if most of the revenue requires aggressive pricing, heavy capitalized development or lower margins than Qualcomm’s existing handset business.

The Investor Day established the size of the ambition. Subsequent earnings reports must establish the economics.

What the July 29 Earnings Report Can—and Cannot—Prove

Qualcomm is scheduled to report fiscal third-quarter results on July 29.

Management previously guided to revenue of $9.2 billion to $10.0 billion, QCT revenue of $7.9 billion to $8.5 billion, QTL revenue of $1.15 billion to $1.35 billion and non-GAAP diluted EPS of $2.10 to $2.30. QCT EBT margin was expected to fall within a 25% to 27% range.

The current quarter was already expected to reflect substantial handset pressure. Qualcomm indicated that handset revenue from Chinese customers would bottom in fiscal Q3 and return to sequential growth in the following quarter, after memory-related reductions in OEM production and channel-inventory drawdowns.

That makes the fiscal fourth-quarter outlook more important than a modest beat against the Q3 guidance range. Several outcomes could provide legitimate positive evidence.

A stronger handset outlook would have the largest immediate effect on earnings estimates because smartphones still account for most of QCT revenue. Confirmation that Chinese Android demand has stabilized, combined with a sequential recovery stronger than previously expected, would reduce near-term downside risk.

Continued automotive growth above approximately 25% would strengthen confidence in the $10 billion fiscal 2029 target. Investors should also look for production launches and customer-program updates that explain where the growth is coming from.

An acceleration in IoT would matter more if management attributes it specifically to PCs, industrial AI or robotics. A recovery driven mainly by conventional consumer devices would improve quarterly results but provide less evidence that Qualcomm’s strategic expansion is taking hold.

Data center revenue is unlikely to be large enough this quarter to transform consolidated results. More realistic catalysts include confirmation that AI200 is shipping on schedule, the beginning of custom-silicon revenue, additional customer commitments, measurable progress with HUMAIN, or intermediate revenue targets for fiscal 2027.

QCT margins may ultimately be the most important measure. Qualcomm can increase revenue through lower-margin businesses without creating equivalent value for shareholders. If diversification revenue grows while QCT margin continues to contract because of product mix and higher development spending, the market may continue to resist a higher multiple.

A constructive earnings report would therefore combine several elements: stabilization in handsets, sustained automotive growth, better visibility into IoT’s composition, initial data center commercialization and margins that remain within or above guidance. One encouraging product announcement would not be enough.

Is a 19x Multiple Too Low?

At approximately 19 times trailing earnings, Qualcomm trades near its own 10-year median rather than at a valuation that assumes a successful transformation. That framing is important. The stock is not priced as though automotive, Physical AI and data centers will fail completely. It is priced as though those businesses will take time to offset the maturity and risks of the handset franchise.

There are sound reasons for that caution. Handsets still represent about 57% of revenue. Apple’s move toward internally developed modems creates a known long-term headwind. AI PC and Physical AI contributions are not separately disclosed. The Meta CPU program does not enter production until the second half of fiscal 2028. Meanwhile, investment in the new roadmap is already affecting operating expenses.

There is also a legitimate case that the valuation fails to reflect the probability of partial success. Qualcomm does not need every Investor Day target to be met in full for the earnings mix to improve. Automotive has already reached scale. IoT generates nearly $7 billion at its current annualized rate. Data center accelerators are scheduled to begin commercial availability before the Meta CPU program reaches production. The company also retains a profitable licensing franchise and completed $5.4 billion of share repurchases during the first half of fiscal 2026, followed by a new $20 billion authorization. The same return discipline applies to the broader question of whether AI infrastructure spending can earn an adequate payback.

The valuation question is therefore asymmetric in an important way. The current multiple requires evidence before assigning much value to the data center and Physical AI plans, but the company already has profitable businesses capable of financing those investments. That reduces the dependence on external capital while allowing Qualcomm to repurchase shares during the transition.

The principal risk is not that Qualcomm lacks the technology to enter new markets. It is that the investments take longer than expected, produce lower margins, or fail to grow fast enough to offset handset pressure. In that outcome, a valuation near the company’s historical range would be justified.

A rerating would require a different set of facts: non-handset revenue growing faster than the decline or maturity of handsets; automotive and IoT contributing measurable operating profit; data center products reaching commercial deployment with more than one major customer; and QCT margins stabilizing despite higher development spending.

Qualcomm Is Potentially Undervalued, but the Discount Is Conditional

Qualcomm’s current valuation appears conservative relative to the breadth of its strategy, but the market is not simply overlooking an established AI infrastructure franchise. It is discounting a transition whose strongest financial evidence still comes from automotive rather than Physical AI or data centers.

Automotive provides the most credible near-term path to the 2029 targets. AI PCs could become measurable over the next several quarters. Robotics and industrial AI require more customer and revenue disclosure. Data centers offer the largest potential change to Qualcomm’s earnings profile, although the most important CPU program does not reach production until 2028 and the accelerator business has yet to establish reported scale.

That leaves Qualcomm in an unusual position. Its existing handset and licensing franchises provide earnings and cash flow, while the new businesses create meaningful upside that is not yet fully visible in the income statement. The 19x multiple may look too low if management delivers even a substantial portion of the Investor Day roadmap. It could remain entirely appropriate if diversification raises revenue without improving consolidated growth, margins and earnings durability.

The July 29 report will not resolve the 2029 investment case. It can provide the first post–Investor Day evidence that the operating trajectory is moving in the promised direction. The most useful signals will be a handset recovery in the next-quarter outlook, sustained automotive growth, clearer sources of IoT expansion, early data center commercialization and stable QCT profitability.

Qualcomm’s valuation is unlikely to change simply because the company can be associated with data centers or Physical AI. It will change when those businesses begin to reduce handset dependence and contribute enough profit to make the historical valuation framework obsolete. Until then, the stock represents a conditional value opportunity: supported by current cash generation, but dependent on execution for a meaningful rerating.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Qualcomm Announces Second Quarter Fiscal 2026 Results | Qualcomm Investor Relations | 2026-04-29 | Company IR | Primary source for fiscal Q2 2026 revenue, QCT and QTL results, QCT revenue streams, margins, share repurchases, fiscal Q3 guidance, and China handset commentary. |

| 2 | Qualcomm Form 10-Q for the quarter ended March 29, 2026 | SEC EDGAR | 2026-04-29 | SEC | Primary filing for fiscal Q2 2026 consolidated results, segment performance, operating expenses, product costs, risks, and capital returns. |

| 3 | Qualcomm fiscal Q2 2026 earnings call transcript | Qualcomm Investor Relations | 2026-04-29 | Company IR | Management context for handset demand, automotive and IoT performance, data center commercialization, and fiscal Q3 guidance. |

| 4 | Qualcomm Investor Day 2026 | Qualcomm | 2026-06-24 | Company IR | Official event hub and presentation materials for the fiscal 2029 strategy, Physical AI, automotive, IoT, data center, and business-update roadmaps. |

| 5 | Qualcomm Investor Day 2026 Data Center Presentation | Qualcomm | 2026-06-24 | Company IR | Official presentation for Dragonfly product sequencing, fiscal 2026 AI200 sampling, second-half fiscal 2027 AI250 timing, second-half fiscal 2028 C1000 timing, and the statement that multi-billion-dollar data center revenue starts in fiscal 2027. |

| 6 | Qualcomm Accelerates Diversification with Comprehensive Strategy for Data Center | Qualcomm Investor Relations | 2026-06-24 | Company IR | Fiscal 2029 targets for $40 billion non-handset revenue, more than $15 billion data center revenue, $10 billion automotive revenue, more than $14 billion IoT revenue, and the $65 billion automotive design-win pipeline. |

| 7 | Qualcomm Unveils Comprehensive Data Center Roadmap for the Agentic AI Era | Qualcomm | 2026-06-24 | Company IR | Dragonfly C1000, AI300, HBC, custom silicon, connectivity, annual product cadence, commercial timing, and Meta roadmap context. |

| 8 | Qualcomm Unveils AI200 and AI250 | Qualcomm | 2025-10-28 | Company IR | Official product announcement and commercial-availability timing for AI200 in 2026 and AI250 in 2027. |

| 9 | Qualcomm and Meta Announce Strategic Multi-Generation Agreement on Data Center CPUs | Qualcomm | 2026-06-24 | Company IR | Official support for Meta's multi-generation Dragonfly C1000 CPU collaboration and planned use in Meta's next-generation server fleet. |

| 10 | HUMAIN and Qualcomm to Deploy AI Infrastructure in Saudi Arabia for Global Inferencing | Qualcomm | 2025-10-27 | Company IR | Official support for HUMAIN's targeted 200-megawatt deployment of Qualcomm AI200 and AI250 rack solutions beginning in 2026. |

| 11 | Qualcomm to Acquire Alphawave Semi | Qualcomm Investor Relations | 2025-06-09 | Company IR | Strategic rationale for adding high-speed wired connectivity, custom silicon, compute IP, and chiplet capabilities to Qualcomm's data center platform. |

| 12 | Qualcomm to Acquire Modular | Qualcomm | 2026-06-24 | Company IR | Official support for the planned Modular acquisition, software-stack rationale, and expected closing in the second half of 2026. |

| 13 | Qualcomm News and Events | Qualcomm | 2026-07-14 | Company IR | Official upcoming-events listing showing fiscal Q3 earnings scheduled for July 29, 2026. |

Financial results and guidance are based on Qualcomm's fiscal Q2 2026 earnings materials and Form 10-Q. Investor Day targets, product timing, and customer programs are forward-looking and may differ from actual results. Investor Day 2026 occurred on June 24, 2026; the article does not rely on dates printed inside illustrative graphics.

Related Reading

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

Serenity Is Watching CCXI: Humanoid Robots Finally Have a Public-Market Entry Point. But Is It a Good Investment?

CCXI could become a rare public-market window into humanoid robotics, but investors still need to separate theme exposure from proven economics.

AI Semiconductors Are No Longer Just About Compute. They Are About System Bottlenecks.

AI semiconductors are no longer just about raw compute. The real question is which system bottlenecks customers must solve next.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments