Stablecoins are often described as digital versions of the U.S. dollar. A user deposits one dollar, receives one stablecoin, and expects to redeem it later for the same amount. To understand how do stablecoins make money, however, investors must examine what happens to the dollar while the stablecoin remains in circulation.

The issuer does not normally leave every customer dollar in a non-interest-bearing account. It can hold reserves in cash, short-term U.S. Treasury securities, repurchase agreements, and other highly liquid assets. Those assets generate interest, creating a potentially large revenue stream for the company operating the stablecoin.

Open USD, or OUSD, is a planned stablecoin announced by Open Standard on June 30, 2026. It uses the same basic reserve-income engine, but its proposed difference is how that income is distributed. Open Standard says that, after a management fee covering operating costs, reserve earnings are intended to flow to the partners that help distribute and use OUSD.

OUSD is expected to launch later in 2026. It does not yet have a live operating record, meaningful circulating supply, or tested redemption history.

Readers who want the full competitive and margin thesis can continue with our deeper analysis of Open USD's distribution model.

Key Takeaways

- Stablecoin issuers earn interest from the cash and short-term Treasury assets held in reserve.

- Reserve income depends mainly on average balances and interest rates, not simply transaction volume.

- USDC shows how large this business can become when billions of dollars remain in circulation.

- OUSD proposes to share more reserve income with payment platforms, wallets, exchanges, and other distribution partners.

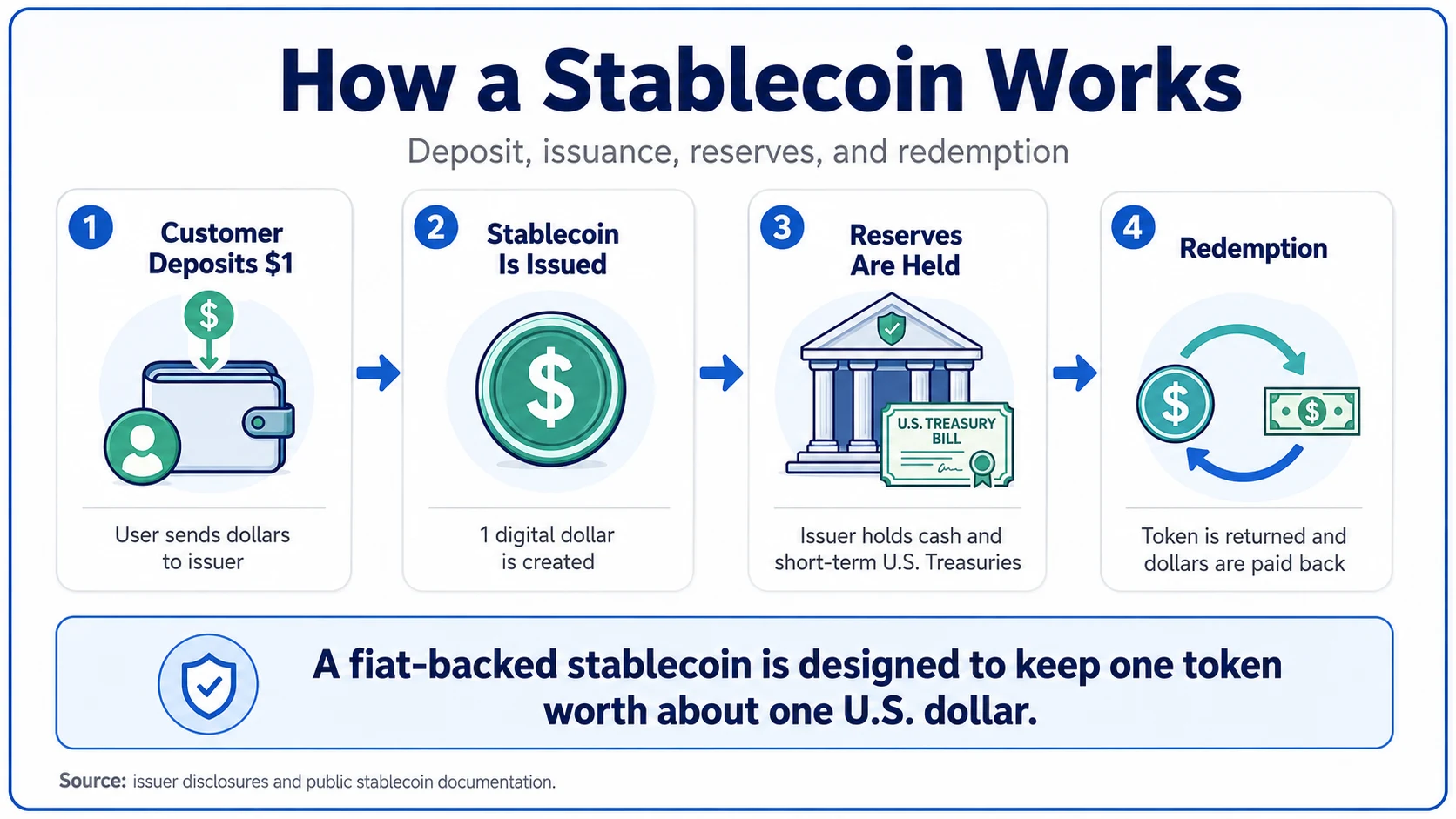

How Does a Stablecoin Work?

A fiat-backed stablecoin usually follows a simple process. A customer or financial institution sends dollars to an issuer. The issuer creates an equivalent number of stablecoins and holds assets intended to support redemptions. When the stablecoin is returned, the issuer destroys, or burns, the token and sends dollars back to the eligible customer.

In simplified form:

Customer deposits $1 → issuer creates one stablecoin → issuer holds $1 of reserve assets

The reserve gives users confidence that the stablecoin can remain worth approximately one dollar. The quality and liquidity of those reserves are therefore central to the stability of the product.

A stablecoin backed mainly by short-term Treasury bills and cash should generally be better positioned to meet redemptions than one backed by long-duration bonds, corporate credit, or assets that are difficult to sell quickly. Full backing alone is not enough. The reserves must also be available when users want their money back.

Source: issuer disclosures and public stablecoin documentation.

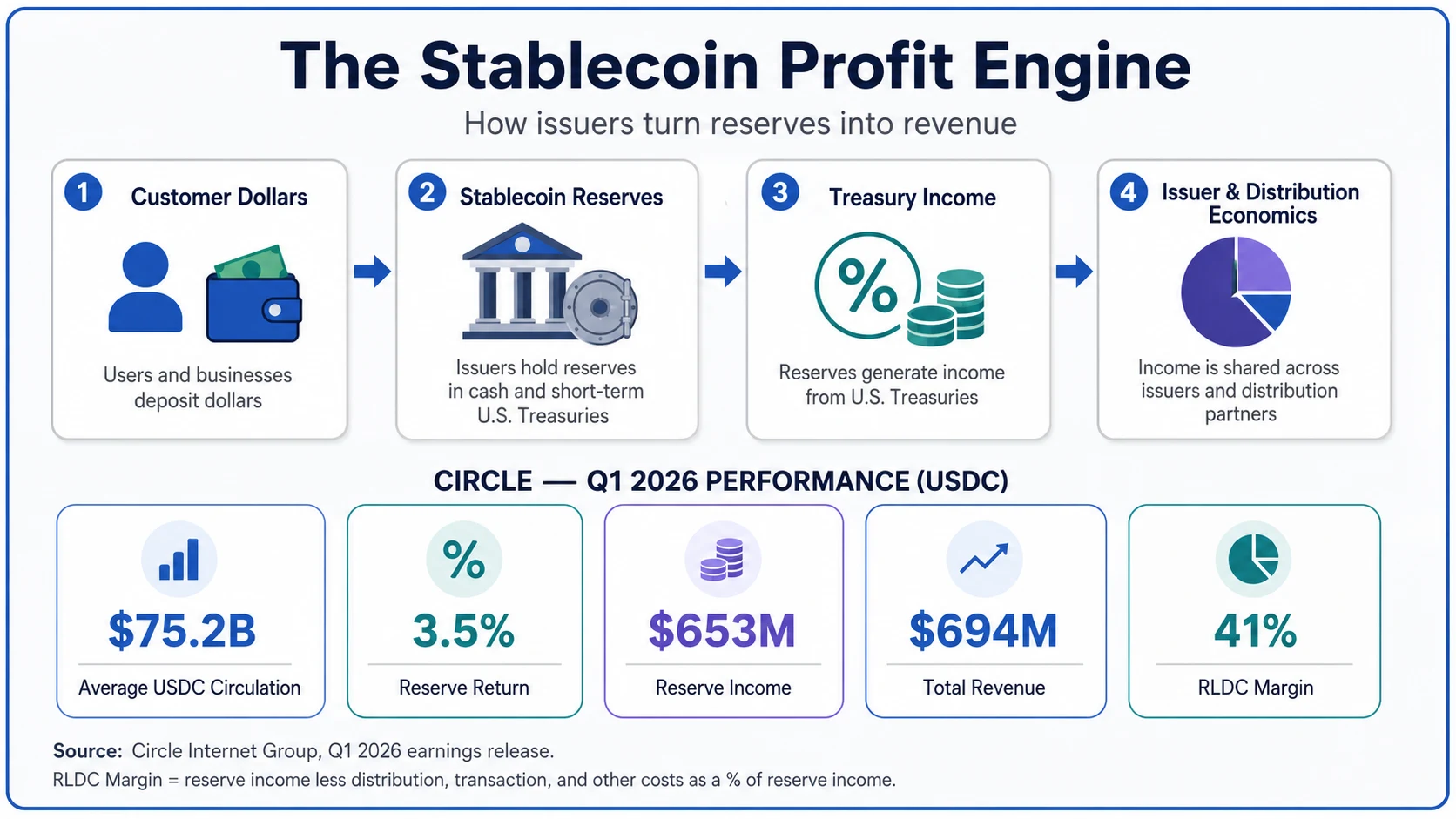

How Do Stablecoin Companies Make Money?

The core revenue equation is:

Reserve income = average stablecoin balance × reserve yield

In plain English, a stablecoin company's gross reserve income is the average dollar amount left in circulation multiplied by the interest rate earned on the assets backing it.

Suppose a stablecoin has an average circulating balance of $10 billion and its reserve assets earn 4% annually. Before custody costs, compliance expenses, operating costs, and partner payments, those reserves could generate approximately $400 million in annual income.

This is why stablecoin issuance is mainly a balance-sheet business rather than a transaction-volume business. A token can move between wallets many times without increasing the amount of reserve assets supporting it. Transaction activity may help adoption, but reserve income is determined mainly by how much money remains in the system and how much interest the reserves earn.

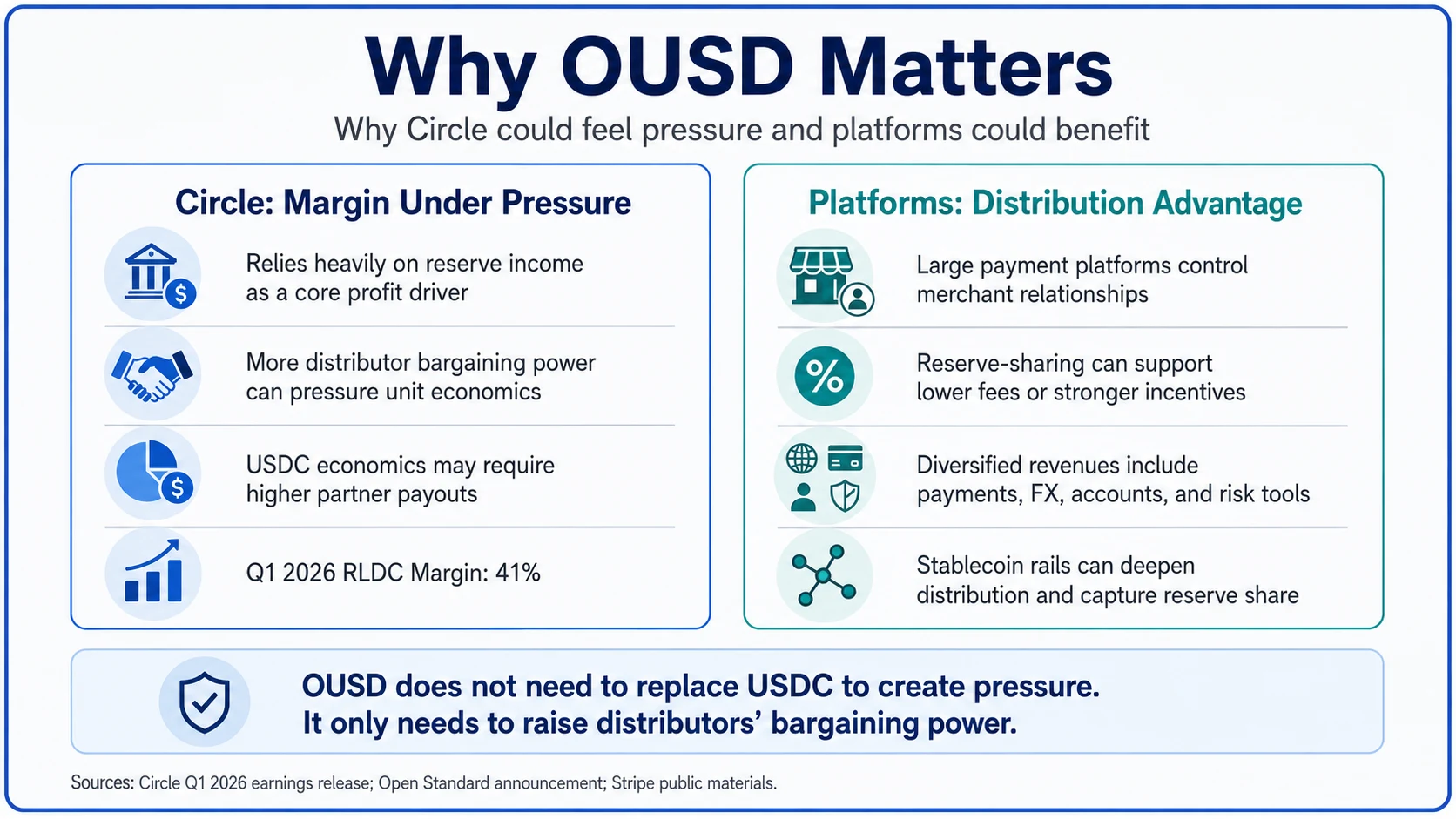

Circle Internet Group's first-quarter 2026 results provide a real-world example. Average USD Coin, or USDC, circulation reached $75.2 billion, and the reported reserve return rate was 3.5%. Circle generated $653 million of reserve income during the quarter and $694 million of total revenue and reserve income. Revenue less distribution costs produced an RLDC margin of 41%.

These figures show why stablecoins became especially profitable when short-term interest rates increased. Billions of dollars held as digital cash can generate Treasury income for the company managing the reserve system.

Source: Circle Internet Group, Q1 2026 earnings release. Circle defines RLDC margin as total revenue and reserve income less total distribution, transaction, and other costs, divided by total revenue and reserve income; this official definition supersedes the shortened footnote embedded in the graphic.

Do Stablecoin Holders Receive the Interest?

Usually, the holder of a standard payment stablecoin does not automatically receive the interest generated by the reserves.

A user may hold $1,000 of USDC or USDT while the underlying reserve assets generate income for the issuer. The user receives the liquidity and convenience of a digital dollar, while the issuer captures the reserve yield.

Some exchanges, wallets, or payment platforms may offer rewards to stablecoin users, but those rewards are generally provided under separate commercial arrangements. They are not necessarily a direct legal claim on the reserve income.

Economically, a stablecoin can function like an interest-free liability for the issuer. The company receives customer funds, invests the reserves in liquid interest-bearing assets, and keeps what remains after paying custody, compliance, operating, and distribution costs.

Why Do Stablecoin Issuers Pay Distribution Partners?

Issuing a stablecoin does not automatically create demand. The token needs to be available on exchanges, wallets, blockchains, payment applications, and merchant platforms. It also requires trading liquidity, fiat conversion, and integrations with financial institutions.

The companies that control those channels can demand part of the economics. Circle, for example, incurs substantial distribution, transaction, and other costs related to the growth and circulation of USDC.

Reserve income is not the same as profit retained by shareholders. A large part of the revenue supports exchanges, platforms, liquidity, and other distribution relationships.

This creates a structural tension. The issuer wants to retain as much reserve income as possible, while exchanges and payment platforms want compensation for bringing users, merchants, and balances into the system.

What Is Open USD?

Open USD, or OUSD, is a planned dollar stablecoin announced by Open Standard on June 30, 2026. It should not be confused with the older Origin Dollar, which also uses the ticker OUSD.

Open Standard says businesses will be able to mint and redeem OUSD without issuance or redemption fees. It also says that participating partners will receive reserve earnings after a management fee covering operating costs is deducted.

More than 140 companies were included in the initial partner coalition. The project is intended for payments, financial infrastructure, exchanges, wallets, and merchant platforms.

Open Standard is led by Zach Abrams, a cofounder of stablecoin infrastructure company Bridge. Stripe completed its acquisition of Bridge on February 4, 2025. Public materials describe Open Standard as the company launching OUSD. They do not establish that Stripe directly issues the stablecoin.

That distinction matters. OUSD is better understood as a planned partner-oriented stablecoin closely connected to the Bridge and Stripe infrastructure ecosystem, rather than simply "Stripe's stablecoin."

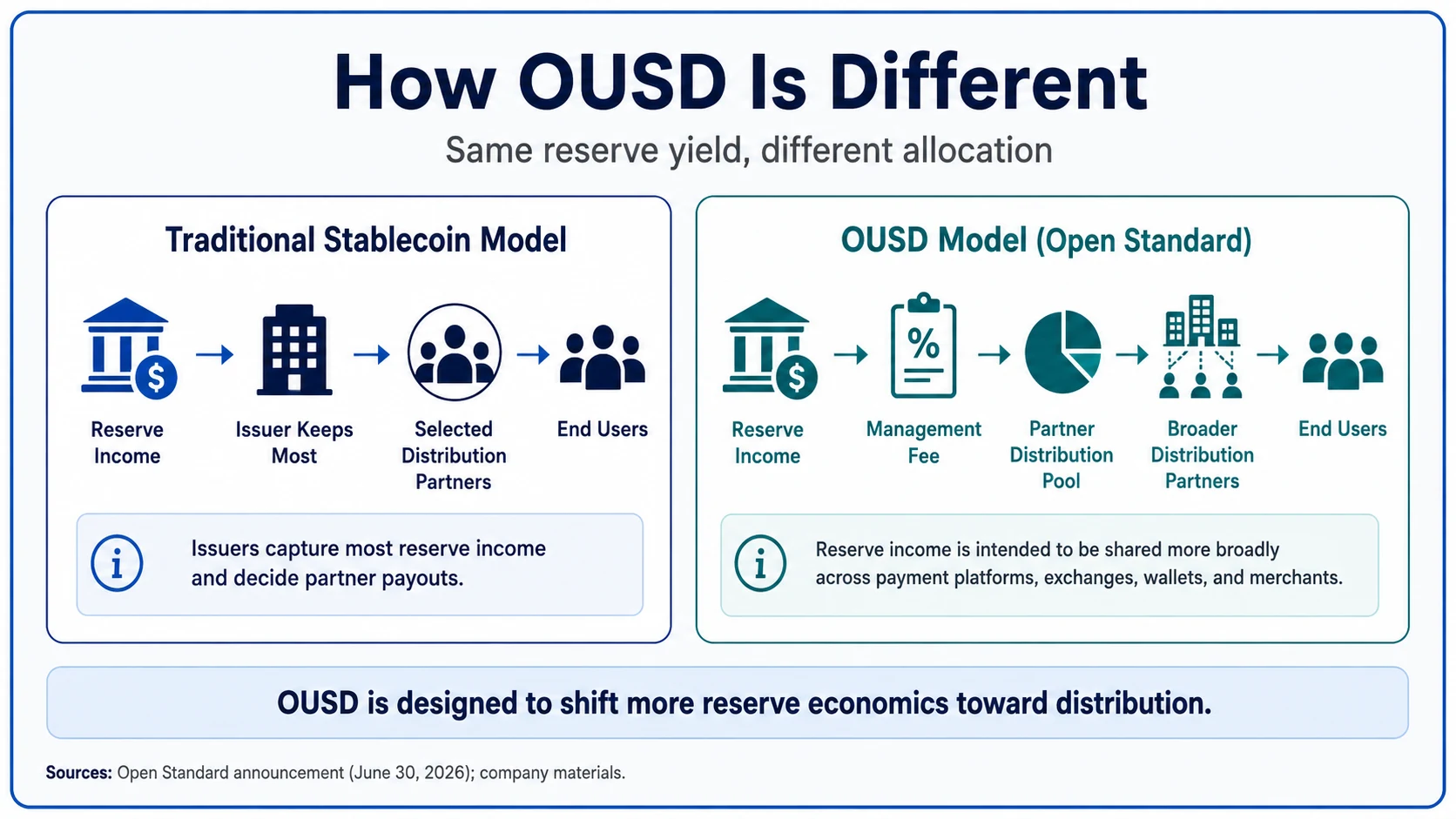

How Is OUSD Different From USDC?

OUSD and USDC are expected to generate income from broadly similar sources: reserves held in cash and liquid short-term assets. The proposed difference is who receives more of the income.

Under a conventional issuer-led model, the issuer earns the reserve yield and negotiates payments with selected distribution partners. Under the OUSD model, a management fee is deducted first and a larger share of the remaining reserve economics is intended to flow to the partners helping distribute and use the stablecoin.

The difference can be simplified as follows:

Traditional model: Reserve income → issuer → selected partner payments

OUSD model: Reserve income → management fee → broader partner distribution

OUSD is therefore not introducing a new type of stablecoin yield. It is proposing a different allocation of the same underlying economics.

Source: Open Standard announcement, June 30, 2026.

Why Would Payment Platforms Support OUSD?

A payment platform could use its share of reserve income in several ways. It could retain the income as additional profit, reduce merchant fees, subsidize cross-border transfers, or offer rewards to customers that maintain stablecoin balances.

Sharing reserve income may give platforms a stronger incentive to make OUSD the default asset inside their products. This matters because most businesses do not choose a stablecoin in isolation. Their payment provider, exchange, wallet, or financial software platform often determines which assets are easiest to use.

Stripe's scale illustrates the power of distribution. Businesses operating on Stripe generated $1.9 trillion in total volume during 2025. That figure should not be treated as a forecast of future OUSD volume, but it demonstrates the size of the merchant network Stripe already controls.

Through Bridge, Stripe has also expanded into stablecoin infrastructure, wallets, issuance tools, fiat conversion, and payment orchestration. This gives Stripe a position across several layers of the stablecoin payment stack.

Could OUSD Replace USDC?

A direct replacement is unlikely to be the first effect. USDC already has established liquidity, institutional integrations, exchange support, blockchain availability, and a history of processing large redemptions. OUSD has not yet launched and therefore has no comparable operating record.

The earlier pressure may appear in Circle's profit margins. If large distribution platforms can earn a greater share of reserve income through OUSD, they may demand better commercial terms from Circle. Circle would then need to choose between paying partners more or risking the loss of future balances and payment activity.

OUSD would not need to overtake USDC in circulating supply to create this pressure. It would only need to become a credible alternative for the platforms that control distribution.

Sources: Circle Q1 2026 earnings release; Open Standard announcement; Stripe public materials.

What Happens When Interest Rates Fall?

The stablecoin reserve model becomes less profitable when short-term interest rates decline. At a 5% reserve yield, $10 billion of average balances can generate roughly $500 million of annual gross income. At a 1% yield, the same balances produce only about $100 million.

This creates an important test for OUSD. When yields are high, reserve income can fund attractive partner rewards and payment subsidies. When yields fall, the amount available for distribution becomes much smaller.

A sustainable stablecoin therefore needs advantages beyond Treasury income. These may include lower settlement costs, reliable redemption, strong liquidity, broad integrations, efficient cross-border payments, and useful financial software.

What Are the Risks of OUSD?

OUSD's partner coalition gives it potential distribution, but it does not guarantee adoption. Investors and users will still need to examine:

- The final reserve composition and custody structure

- Who is legally responsible for redemption

- Which users can redeem directly

- The management fee charged by Open Standard

- How partner payments are calculated

- Secondary-market liquidity

- The concentration of balances among large platforms

- Performance during a banking or market disruption

The partner-allocation formula will be particularly important. A system based mainly on balances may favor large exchanges and wallets. One based on transaction volume could create incentives to manufacture activity. A system based on merchant adoption may allow the largest payment platforms to capture most of the income.

Sharing reserve economics does not guarantee that ordinary users will benefit. The income could move from stablecoin issuers to a small group of powerful distribution platforms without materially reducing customer costs.

The Business Model in One Sentence

Stablecoin users provide the balances, reserve assets generate the income, and the central competitive question is who captures that income.

USDC represents an issuer-led model in which Circle earns reserve income and pays for distribution. OUSD proposes a more distribution-led structure in which payment platforms and other partners receive a larger share of the economics.

Whether that structure succeeds will depend on more than the number of companies supporting its announcement. OUSD must turn potential partners into live integrations, live integrations into lasting balances, and those balances into a stable network capable of processing redemptions under pressure.

Frequently Asked Questions

How Do Stablecoin Issuers Make Money?

The answer to "how do stablecoins make money?" is that issuers generally earn interest from the cash, Treasury bills, and other liquid assets held in reserve. Their revenue depends mainly on average circulating balances and the return earned on those reserves.

What Is Stablecoin Reserve Income?

Reserve income is the interest generated by the assets backing a stablecoin. Short-term U.S. Treasury securities can generate income while users hold the corresponding stablecoins.

Do USDC Holders Receive Circle's Reserve Income?

Standard USDC holders do not automatically receive the interest generated by Circle's reserve assets. Some platforms may separately offer rewards or incentives.

What Is Open USD?

Open USD, or OUSD, is a planned dollar-backed stablecoin announced by Open Standard in June 2026. Its proposed model shares more reserve economics with participating distribution partners.

Is OUSD Owned or Issued by Stripe?

Public materials describe OUSD as a project launched by Open Standard. Stripe's connection comes through its acquisition of Bridge and its broader involvement in stablecoin infrastructure.

Why Could OUSD Affect Circle?

OUSD could give payment platforms and other distributors greater bargaining power. Circle may need to share more USDC reserve income with partners to defend distribution and future growth.

Is OUSD Already Available?

No. Open Standard announced OUSD on June 30, 2026 and said it was expected to launch later in the year. It does not yet have the operating record of established stablecoins such as USDC or USDT.

Sources

- Open Standard, "Introducing Open USD" — June 30, 2026.

- Stripe, "Stripe Completes Bridge Acquisition" — February 4, 2025.

- Circle Internet Group, Q1 2026 Earnings Release — May 2026.

- Stripe, 2025 Annual Update — 2026.

- Bridge Product Overview — current product information.

Frequently Asked Questions

How do stablecoin issuers make money?

The answer to 'how do stablecoins make money?' is that issuers generally earn interest from the cash, Treasury bills, and other liquid assets held in reserve. Their revenue depends mainly on average circulating balances and the return earned on those reserves.

What is stablecoin reserve income?

Reserve income is the interest generated by the assets backing a stablecoin. Short-term U.S. Treasury securities can generate income while users hold the corresponding stablecoins.

Do USDC holders receive Circle's reserve income?

Standard USDC holders do not automatically receive the interest generated by Circle's reserve assets. Some platforms may separately offer rewards or incentives.

What is Open USD?

Open USD, or OUSD, is a planned dollar-backed stablecoin announced by Open Standard in June 2026. Its proposed model shares more reserve economics with participating distribution partners.

Is OUSD owned or issued by Stripe?

Public materials describe OUSD as a project launched by Open Standard. Stripe's connection comes through its acquisition of Bridge and its broader involvement in stablecoin infrastructure.

Why could OUSD affect Circle?

OUSD could give payment platforms and other distributors greater bargaining power. Circle may need to share more USDC reserve income with partners to defend distribution and future growth.

Is OUSD already available?

No. Open Standard announced OUSD on June 30, 2026 and said it was expected to launch later in the year. It does not yet have the operating record of established stablecoins such as USDC or USDT.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Introducing Open USD | Open Standard | June 30, 2026 | Company announcement | OUSD announcement, planned launch, partner structure, minting and redemption approach, and reserve-income distribution model. |

| 2 | Stripe completes Bridge acquisition | Stripe | February 4, 2025 | Company announcement | Stripe's acquisition of Bridge and Zach Abrams's role as Bridge cofounder. |

| 3 | Q1 2026 earnings release | Circle Internet Group | May 2026 | Company IR | Average USDC circulation, reserve return rate, reserve income, total revenue and reserve income, and RLDC margin. |

| 4 | Stripe's 2025 annual letter | Stripe | 2026 | Company update | Businesses on Stripe generated $1.9 trillion in total volume during 2025. |

| 5 | Bridge product overview | Bridge | Current | Company information | Bridge's stablecoin infrastructure capabilities, including issuance, wallets, conversion, and payment orchestration. |

Primary company announcements and financial disclosures support the operating, financial, and forward-looking claims in this guide.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments