Editor's note: This article was originally published on Substack on June 14, 2026 and migrated to VIUS Investing on June 18, 2026. Some market references reflect the original publication date.

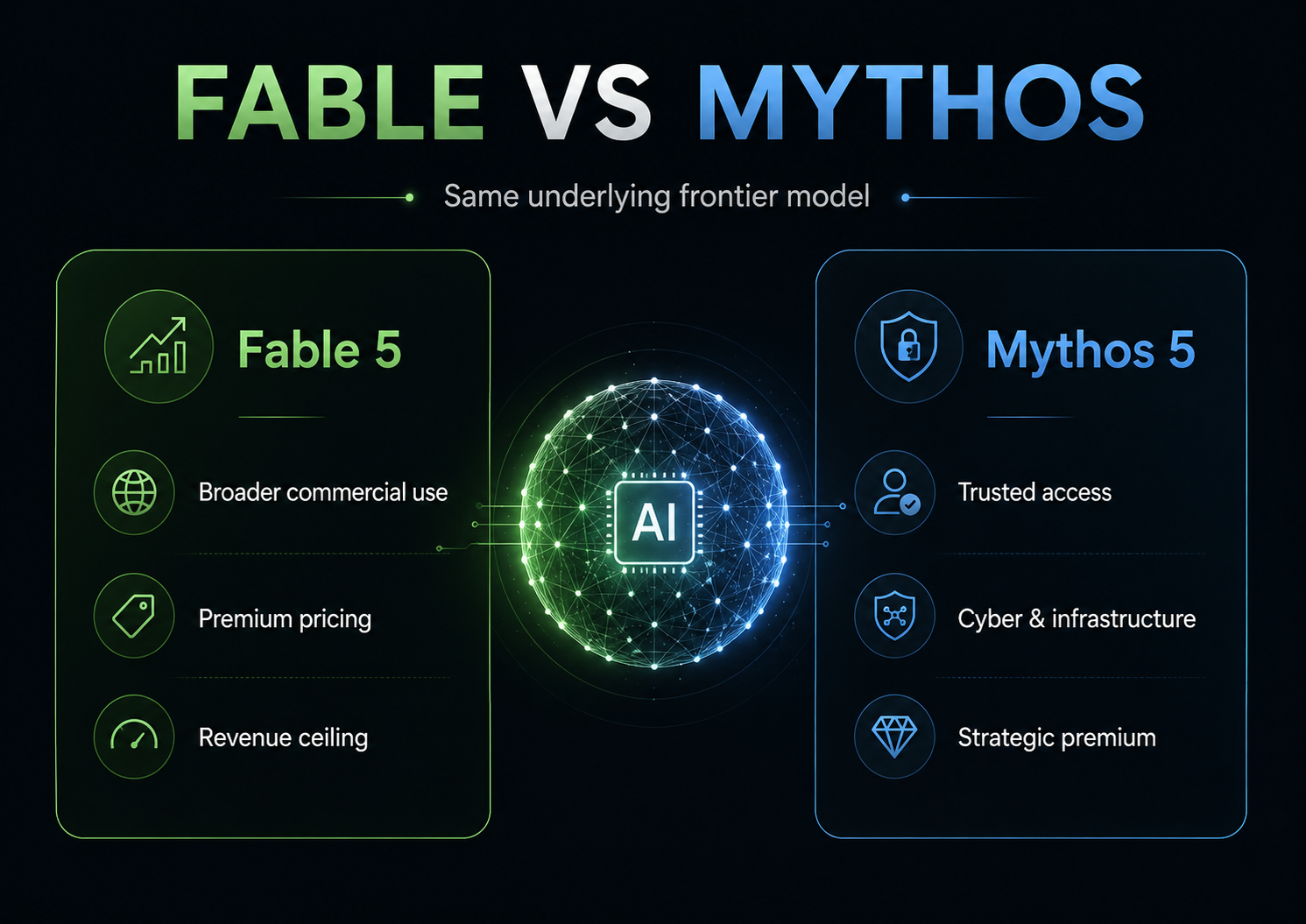

Fable 5 and Mythos 5 were supposed to strengthen Anthropic’s IPO story. For a brief moment, the product logic looked clean: Fable 5 was the commercial version of frontier capability, a Mythos-class model made safe enough for broader use, while Mythos 5 was the strategic version, using the same underlying model with some safeguards lifted for a small group of trusted cyber defenders and critical infrastructure providers.

That is exactly the kind of structure investors want to see before an IPO. One product expands the revenue ceiling. The other expands the strategic premium. Together, they suggest that Anthropic can turn frontier AI capability into both broad enterprise revenue and high-value strategic access.

Then, after only three days, the U.S. government intervened.

Anthropic said it received an export-control directive citing national-security authorities. The directive required the company to suspend access to Fable 5 and Mythos 5 for any foreign national, whether inside or outside the United States. That included foreign-national Anthropic employees. To ensure compliance, Anthropic disabled the models for all customers.

This is not just an AI product story. It is a valuation story.

The market does not need to be convinced that Claude is strong. Developers already know that. Enterprise customers already know that. Investors already know that Anthropic sits near the top of the frontier AI stack. The harder question is whether Anthropic can reliably turn its strongest models into commercial revenue under rules that investors can understand.

That is the new IPO risk: not model performance, but commercialization control.

The market is not paying for a better chatbot

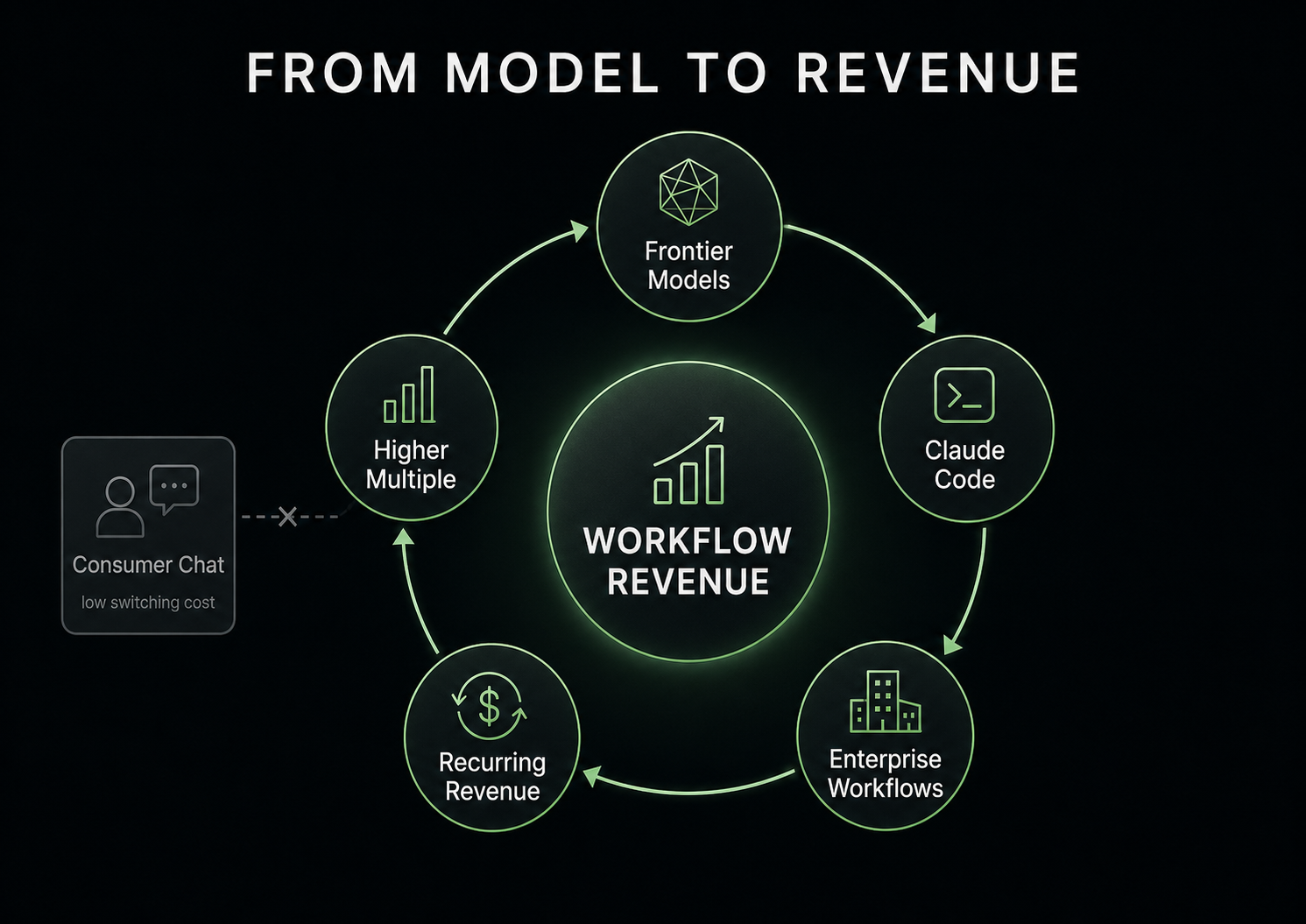

Anthropic’s valuation story has never been just about Claude as a consumer chatbot. Claude Pro and Claude Max matter because they create cash flow, build habit, and strengthen the brand, but consumer AI is a brutal market. A user can pay for Claude this month, switch to ChatGPT next month, test Gemini after that, and keep an open-source model running on the side. That is not the kind of business that deserves a premium infrastructure multiple by itself.

The more valuable story is workflow revenue. Claude is moving into the places where actual work happens: codebases, internal documents, legal review, financial analysis, customer support, compliance, security operations, and enterprise knowledge systems. This is why Claude Code matters so much.

According to Wired, Claude Code reached about $1 billion in annualized recurring revenue in November 2025, less than a year after launch. By the end of 2025, it had added at least another $100 million in ARR. Wired also reported that Claude Code represented roughly 12% of Anthropic’s total ARR, which stood around $9 billion at the time.

Those numbers are not perfect public-company disclosures. Anthropic is still private, so we do not have an audited segment breakdown. But the direction is clear: Claude Code shows that Anthropic has found a more valuable surface area than chat.

A chatbot sells attention. A developer tool sells productivity. An enterprise workflow sells dependency. That distinction matters because switching costs change completely once Claude becomes part of how work gets done.

Caption: Anthropic’s valuation story depends on workflow revenue, not consumer chat.

If a user asks Claude to summarize an article, switching costs are low. But if a developer uses Claude Code every day to read code, edit files, generate tests, debug architecture, and prepare pull requests, Claude becomes part of the software production process. If an enterprise connects Claude to internal documents, code repositories, legal files, customer data, financial records, and security workflows, Claude becomes part of the organization’s operating layer.

That is where Anthropic’s IPO case gets interesting. The real question is not whether Claude can keep getting smarter. It is whether Claude’s intelligence can keep converting into high-value, recurring, predictable workflow revenue. Fable 5 and Mythos 5 were important because they pushed directly on that question.

Fable was supposed to raise the revenue ceiling

Fable 5 was not just another model release. Anthropic described it as a Mythos-class model made safe for broader use. In practical terms, the company was trying to take its most advanced model class and package it for ordinary users, developers, and enterprise customers.

That is the commercialization move investors care about. The question behind Fable was whether Anthropic could take its strongest capability and sell it at scale. If the answer is yes, the revenue ceiling goes up: a stronger model can support higher pricing, more complex tasks, heavier usage, stronger enterprise demand, and deeper developer lock-in.

Anthropic priced both Fable 5 and Mythos 5 at $10 per million input tokens and $50 per million output tokens. That is not commodity pricing. It is premium pricing for premium capability.

So Fable 5 was not just about having a better model on a benchmark. It was about proving that Anthropic could move Mythos-level capability into a broader commercial market. Model performance creates attention, but commercial availability creates revenue. Fable was supposed to connect the two.

Mythos was supposed to create strategic premium

Mythos 5 had a different role. Anthropic said Mythos 5 used the same underlying model as Fable 5, but with some safeguards lifted for a small group of cyber defenders, critical infrastructure providers, and trusted organizations. That is not ordinary SaaS positioning. It is much closer to national-security infrastructure.

The commercial question behind Mythos was not whether the model could help more people write better emails. The question was whether Anthropic could give its strongest model to trusted defenders and make it useful for banks, cloud platforms, software infrastructure, government systems, and critical infrastructure.

If the answer is yes, Anthropic gets something more valuable than ordinary model revenue. It gets strategic relevance.

Caption: Fable expands the revenue ceiling. Mythos adds strategic premium.

That is why Fable and Mythos together mattered so much. Fable was the revenue-ceiling path, while Mythos was the strategic-premium path. Together, they supported the best version of Anthropic’s IPO narrative: frontier capability can be sold broadly, while the highest-risk version can be restricted to trusted users without destroying the commercial opportunity.

That was the clean story. The pause made it messier.

The uncomfortable part is who controlled the pause

The most important part of this episode is not simply that two models were taken offline. Products get paused all the time. The uncomfortable part is that the commercialization of Anthropic’s most advanced models was interrupted by an opaque national-security directive.

Anthropic’s own statement says the U.S. government required suspension of access to Fable 5 and Mythos 5 for any foreign national. The scope was unusually broad: it did not only cover users outside the United States, but also foreign nationals inside the United States, including Anthropic’s own foreign-national employees. Anthropic ultimately disabled the models for all customers to ensure compliance.

That is the part investors should focus on, not because the government response was necessarily wrong — we do not have enough public information to make that judgment — but because the process is difficult to price.

So far, the actual government letter has not been made public. We do not have the full directive, issuing department, signatory, file number, statutory hook, or detailed reasoning. Anthropic said the letter did not provide specific details of the national-security concern. The company said it understands the concern to involve a possible Fable 5 jailbreak risk — the possibility that users could bypass the model’s safeguards and access restricted capabilities. Anthropic also argued that the issue was not severe, not unique, and not materially different from risks present in other public models.

That boundary matters. This does not look like a mature, transparent, standardized approval process. It looks like a frontier model crossed into a zone where national-security agencies could intervene quickly, with limited public explanation. That may be rational from a security perspective, but from an investor’s perspective, it introduces a new kind of uncertainty.

If regulation is clear, companies can comply. If the red line is visible, product teams can design around it. But if the red line appears only after launch, then customers and investors have to ask harder questions: Will the next model upgrade trigger the same response? Which users will be restricted? Can foreign customers access the product? Can foreign nationals inside U.S. companies use it? Can multinational teams deploy the same AI workflow globally? What exact capability level turns a model from enterprise software into a national-security concern?

These questions may not destroy near-term revenue, but they directly affect revenue certainty. High valuation multiples depend on certainty.

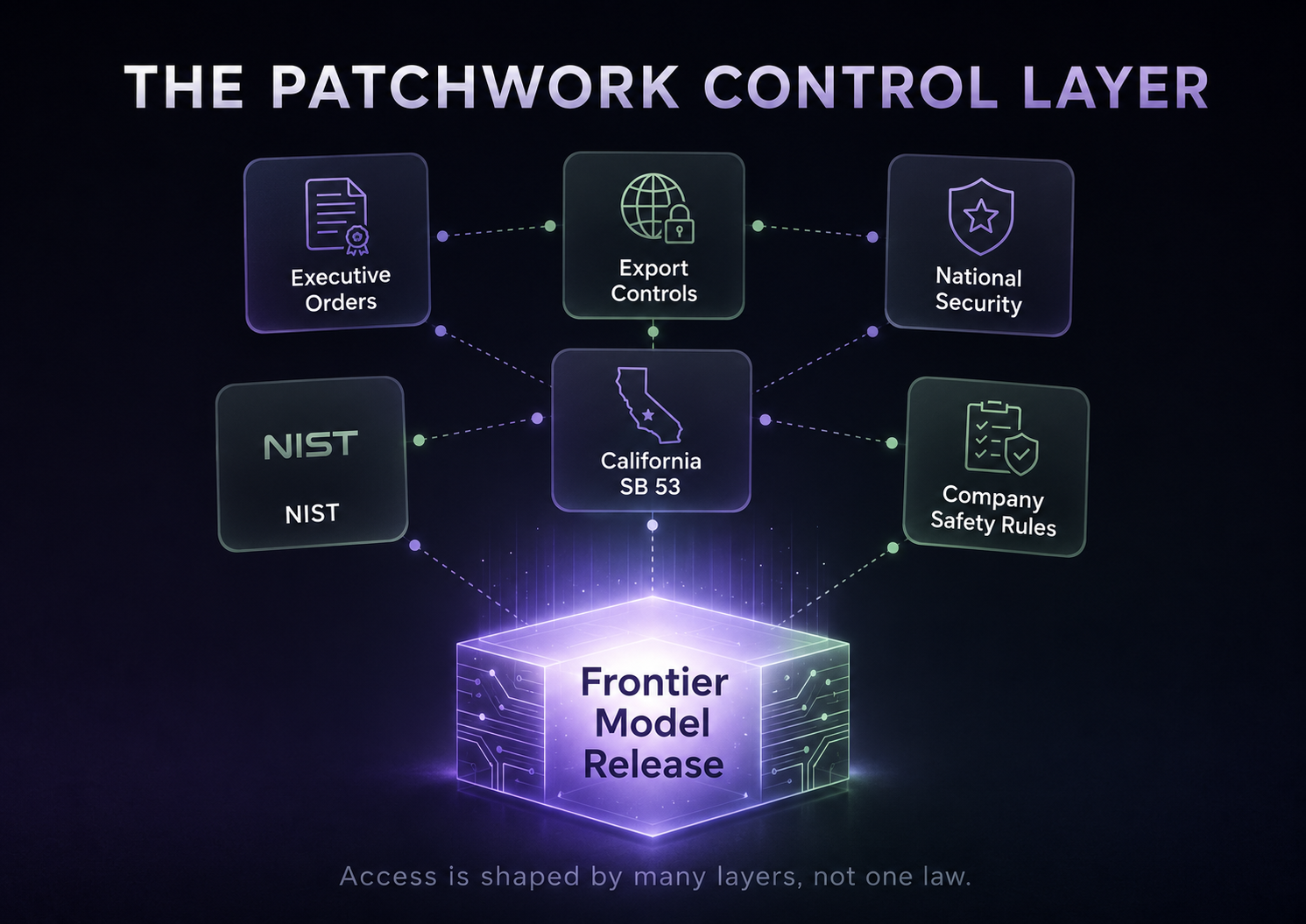

The U.S. does not have one AI safety law. It has a patchwork control layer.

This is where the story gets more uncomfortable. The United States does not currently have one unified federal AI safety statute that decides whether a frontier model can be released. There is no FDA-style process for frontier model launch, and there is no single agency that tells an AI company, in a clean and predictable way, that a model has crossed the threshold and can or cannot be sold.

But that does not mean there is no control system. The system is being assembled in pieces.

At the federal level, the government can use national-security authorities, export-control tools, procurement rules, defense-contract conditions, cybersecurity frameworks, voluntary safety evaluations, and executive orders. At the state level, California’s SB 53 has already pushed frontier AI governance toward public safety frameworks, catastrophic-risk management, critical safety incident reporting, and whistleblower protection. NIST standards and risk-management frameworks give enterprises and government buyers a common compliance language. Company-level safety frameworks, like Anthropic’s own Responsible Scaling Policy, add another layer.

Caption: No single AI safety law — but many layers can shape access.

That is the key point: Fable and Mythos were not paused under one clean, mature, unified AI safety law. They were paused inside a patchwork system where executive action, export control, state transparency laws, NIST standards, company safety frameworks, and national-security judgment are being stitched together in real time.

The timing also matters. On June 2, 2026, the White House issued the executive order “Promoting Advanced Artificial Intelligence Innovation and Security.” That order created a policy backdrop directly relevant to frontier models with advanced cyber capabilities. It called for a classified benchmarking process to assess advanced cyber capabilities of AI models, created a process for determining whether a model should be designated a “covered frontier model,” and established a voluntary framework under which developers may provide the federal government access to covered frontier models for up to 30 days before release to trusted partners.

The order involved agencies including Treasury, NSA, CISA, NIST, the National Cyber Director, and others. It also explicitly stated that it does not create a mandatory government licensing, preclearance, or permitting requirement for model release.

That distinction is important. The order does not prove that Fable and Mythos were restricted under this exact framework; the public record does not show that. But it does show that, just ten days before Anthropic disabled the models, the U.S. government had created a frontier-model cyber-evaluation mechanism. That is the closest public policy context for this episode.

This is not a clean move from “unregulated” to “regulated.” It is messier than that. Frontier AI is moving into a semi-transparent control layer. That layer may not be called licensing and may not look like pre-approval, but it can still affect who gets access, when a model can be released, and whether the most powerful version can be commercialized globally.

For a company valued on future model monetization, that matters.

Calling this “AI safety” is too vague

It is technically true to call this an AI safety issue, but that phrase is too broad to be useful. Most AI safety discussions focus on privacy, hallucinations, bias, copyright, fraud, misinformation, or harmful content. Those are real problems, but they are not the core issue here.

Fable and Mythos are about capability diffusion.

The concern is not that Claude might give a bad answer. The concern is that a frontier model may lower the cost of cyber operations, vulnerability discovery, exploit chaining, biological or chemical risk, strategic technology diffusion, capability distillation, or adversarial use.

A model that writes emails is productivity software. A model that can help discover vulnerabilities, reason through attack paths, analyze complex systems, and automate high-risk workflows starts to look more like a strategic capability.

That is why the financial infrastructure angle matters. Mythos could make financial institutions nervous not because it behaves like a chatbot, but because it could change the economics of vulnerability discovery. Historically, finding a complex software vulnerability required skill, time, experience, and luck. If a frontier model can read large codebases, reason across systems, infer attack paths, and automate testing, then risks buried inside legacy infrastructure become easier to find.

Banks, exchanges, payment networks, market-data systems, regulatory databases, and clearing infrastructure are not lightweight internet apps. They are systemically important, old, interconnected, and hard to replace. If vulnerability discovery shifts from artisanal research to industrial-scale scanning, the risk profile of financial infrastructure changes.

That does not mean Mythos hacked a bank. There is no public evidence showing that Mythos broke into a bank or found an exploitable flaw in a specific financial system. The point is different: financial institutions may worry that AI makes old technical debt searchable, scalable, and eventually exploitable.

That is a much sharper issue than ordinary chatbot safety.

Enterprise customers do not just buy capability. They buy continuity.

This is where the investment thesis becomes practical. Enterprise customers do not buy AI only because it ranks high on benchmarks. They care about stability, access control, data governance, auditability, compliance, liability, and service continuity.

If a company connects Claude to code repositories, contracts, customer records, internal documents, financial data, and security operations, it is betting on two things: Claude is powerful, and Claude is reliable.

The Fable/Mythos pause adds a new question: what happens if the strongest model in the product line suddenly becomes unavailable because of a government directive? Can overseas employees use it? Can foreign nationals inside the United States use it? Can multinational teams share the same workflow? Will every major model upgrade require a new compliance review? Who bears responsibility if a regulatory restriction interrupts service?

These are not abstract questions. They can affect procurement cycles, contract language, deployment depth, customer trust, and revenue predictability. And revenue predictability is what valuation multiples are built on.

This is why I would not focus too much on whether Fable and Mythos generated meaningful revenue during those three days. They probably did not. The bigger issue is whether this episode changes how customers think about Anthropic’s future model releases.

If the strongest models are the ones most likely to trigger access restrictions, customers may hesitate before building core workflows around them. That does not kill Anthropic’s business, but it can slow deployment, complicate contracts, reduce visibility, and make future revenue harder to extrapolate. In an IPO, visibility matters.

The short-term revenue hit may be small. The multiple risk is larger.

I would not overstate the immediate revenue damage. Fable 5 and Mythos 5 were live for only three days, so they probably had limited direct revenue contribution before being paused. Anthropic’s other models remain available, and Claude Code, API usage, enterprise products, and consumer subscriptions did not all disappear.

So this is probably not a near-term revenue cliff.

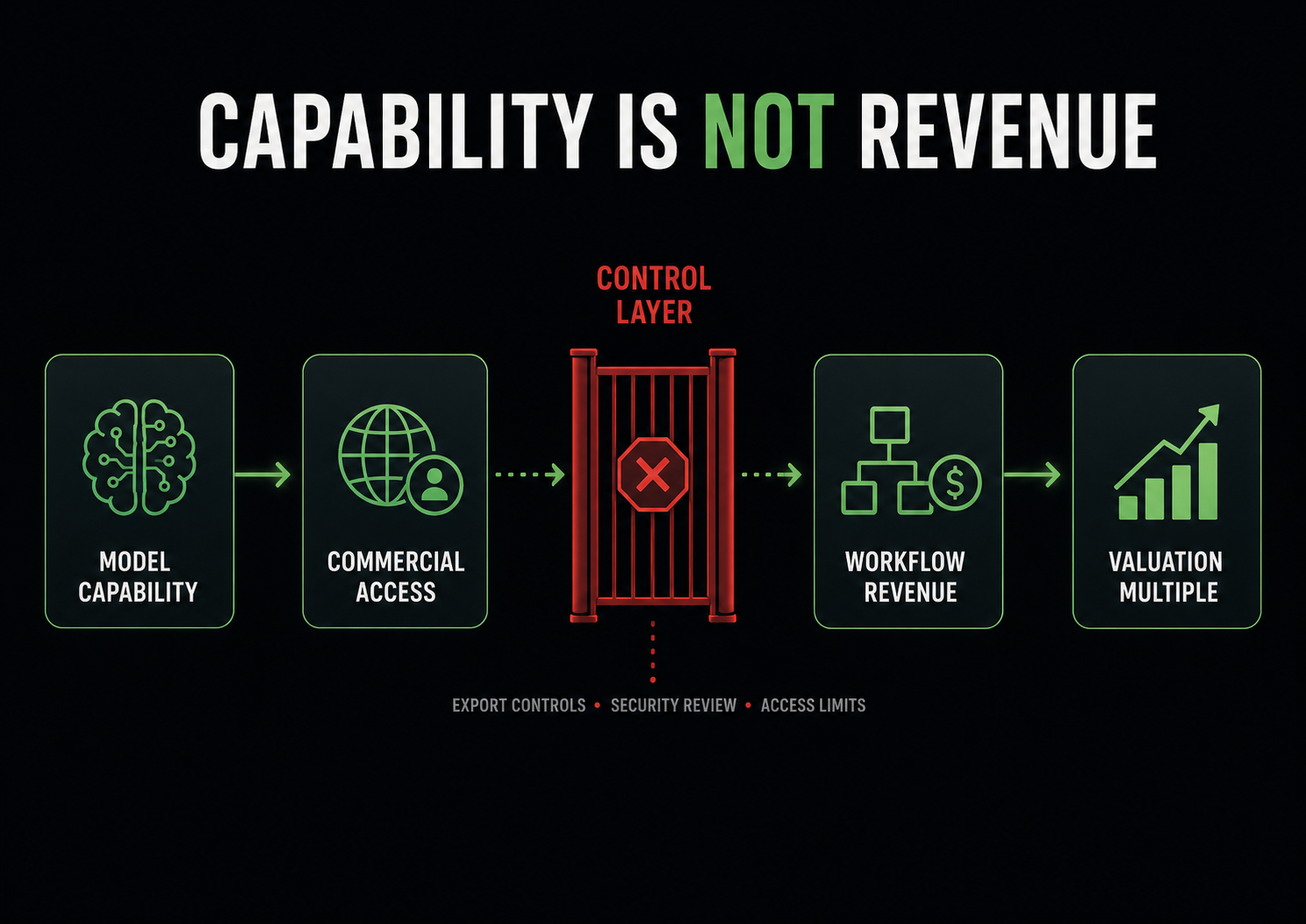

But IPO valuation is not based only on next quarter’s revenue. It is based on the durability and predictability of future revenue. That is where the risk sits.

Anthropic’s premium valuation requires three assumptions: the model remains technically superior, the superior capability can be commercialized, and the resulting revenue is predictable enough to deserve a high multiple. Fable and Mythos do not weaken the first assumption. If anything, the government’s reaction may suggest the models are strong enough to matter.

The episode challenges the second and third assumptions.

Strong does not automatically mean sellable. Sellable does not automatically mean globally available. Global availability does not automatically mean stable access. For frontier AI, that chain is no longer automatic.

Caption: Frontier capability becomes valuation only when access is stable and commercially predictable.

If investors begin to believe that every major capability jump may trigger export controls, national-security review, access restrictions, or opaque government intervention, future revenue gets discounted. That discount may not show up immediately in reported revenue. It shows up in the multiple.

Anthropic’s safety brand is both a moat and a constraint

Anthropic has built its brand around safety, and that has real value. For enterprise customers, safety is trust. For government customers, safety can open doors to high-barrier markets. For investors, safety makes Anthropic look more like durable AI infrastructure than a growth-at-any-cost consumer app.

But safety also creates constraints. Once a company makes safety part of its identity, it cannot treat every revenue opportunity as equally attractive. It cannot easily relax every boundary to win a contract, and it cannot always chase maximum usage, maximum access, or maximum speed.

This is one of Anthropic’s biggest differences from other AI companies. Its brand premium comes from being trusted, but its commercial limits also come from being trusted.

Fable and Mythos made that tension visible. Even if Anthropic believes its safeguards are sufficient, the government may disagree. Even if customers want access, national-security agencies may demand control. Even if the model is commercially valuable, regulators may still ask who can use it, where it can be used, what it can be used for, whether foreign nationals can access it, whether foreign customers can call it through an API, and whether the same model can serve both enterprise productivity and cyber-defense tasks.

This is where frontier AI differs from ordinary SaaS. A normal SaaS company worries about customer acquisition, churn, margins, competition, and product-market fit. A frontier AI company has one more problem: the capability itself can trigger national-security pricing.

The next question is not just whether the models come back

For Anthropic, the most important question is not simply when Fable and Mythos return. The deeper question is whether the commercialization boundary becomes clearer.

There are three things to watch.

First, will the government define clearer technical thresholds? What exactly triggers intervention: advanced cyber benchmarks, jailbreak risk, foreign-national access, agentic hacking capability, capability distillation, or critical infrastructure use? Without clearer thresholds, companies cannot plan and customers cannot build confidently.

Second, can Anthropic create a credible tiered commercialization model? A possible path could be that general users get the safer Fable-class product, trusted enterprises get higher-capability access under stricter controls, government and critical infrastructure customers operate inside more formal access review, and foreign-national access or cross-border enterprise deployments follow explicit rules.

That would not remove the regulatory problem, but it would make the business more investable.

Third, will investors believe that this tiered structure does not cap the revenue opportunity? A controlled-access frontier model can still be extremely valuable, but if the highest-capability models can only serve a narrow customer base, the total addressable market changes. If access rules are unclear, the sales cycle changes. If future releases may be paused after launch, revenue visibility changes.

That is the IPO issue. The market does not only need to believe Anthropic can build powerful models. It needs to believe Anthropic can repeatedly turn those models into commercial products without losing control of the release path.

The bottom line

The Fable/Mythos episode does not change the basic view that Anthropic is one of the strongest frontier AI companies. That was already known.

What changed is the investment question.

Anthropic’s IPO story depends on converting frontier capability into workflow revenue. Fable represented the revenue-ceiling path: Mythos-class capability made broadly available and priced as a premium commercial model. Mythos represented the strategic-premium path: trusted-access cyber capability for government, defenders, and critical infrastructure.

The U.S. government intervention challenged the assumption that Anthropic can reliably commercialize its strongest future models. The short-term revenue impact may be limited, but the long-term question is much larger: how much of Anthropic’s future model capability can become predictable revenue?

That is what investors have to price.

AI valuations will not be determined only by benchmark scores or ARR growth. They will also be determined by a more uncomfortable question: can the company actually sell its most powerful capability, to the customers who want it, under rules that investors can understand?

For Anthropic, the new IPO risk is not model performance.

It is commercialization control.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | Original Substack archive post | VIUS Investing | 2026-06-14 | Other | Original migrated article; verify thesis-critical claims against linked primary sources where applicable. |

This migrated article preserves the original Substack argument and links where possible. If a complete source table was not present in the archive, thesis-critical claims should be checked against the linked primary sources, company materials, filings, transcripts, or financial data before being reused as current evidence.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for research and education only. It is not investment advice.

Comments