AI companies are spending enormous amounts of money on chips, data centers, electricity, networking equipment, and cloud infrastructure. That has created a simple question for investors: is this just another technology boom, or is the financial structure underneath it becoming risky?

The answer is more complicated than saying “AI is a bubble” or “AI demand is real, so there is no problem.”

AI demand can be real and still create financial risk if companies invest too much, borrow too heavily, rely on weak customers, or build infrastructure around long-term contracts that become difficult to fulfill.

That is why investors are increasingly looking beyond GPU sales and the broader AI infrastructure cycle. They are asking a different set of questions: Who is financing the infrastructure? Who is signing the contracts? Who ultimately pays? And what happens if growth slows?

This guide explains the basics.

What Does “AI Infrastructure Credit Risk” Mean?

AI infrastructure credit risk is the risk that companies involved in building AI data centers, buying GPUs, or providing computing capacity may struggle to repay debt or meet financial obligations if expected customer payments do not arrive as planned.

A modern AI data center can cost billions of dollars. It requires servers, GPUs, cooling systems, power infrastructure, land, buildings, and networking equipment. Much of that spending happens before the full revenue is earned.

Companies can finance that buildout in several ways. Some use their own operating cash flow. Others borrow money, sign long-term leases, create joint ventures, or raise project debt backed by customer contracts.

The risk depends on the structure.

A company like Meta can spend heavily on AI while relying largely on cash generated by its advertising business. A neocloud provider may instead borrow against future payments from a small number of customers. Those two companies may report similar capital spending, but the financial risk is very different.

Why Are Investors Comparing the AI Boom With 2008?

Most people compare the AI boom with the dot-com bubble of 2000. That comparison focuses on stock valuations, speculative companies, and whether investors are paying too much for future growth.

A different argument was recently made by Groundbreaker Research in an essay titled The Second Derivative: Why No One Understands the AI Boom. The article argues that parts of the AI infrastructure buildout may be better understood through the lens of credit expansion.

The idea is straightforward. Data centers are expensive physical assets. Customers sign long-term compute contracts. Infrastructure companies use those contracts to support financing. The financing is then used to buy GPUs, build facilities, or expand capacity.

If customers keep paying and demand continues to grow, the system works.

If growth slows, contracts weaken, or customers become less able to pay, pressure can move backward through the chain.

That does not mean AI is already experiencing a 2008-style crisis. It means some of the financial connections that can transmit risk are starting to exist.

For a deeper analysis of the financing structures, company-level evidence, and the Groundbreaker thesis, read our full Market Notes report: Is the AI Bubble About to Break? The Real Risk May Be Hiding in the Credit System.

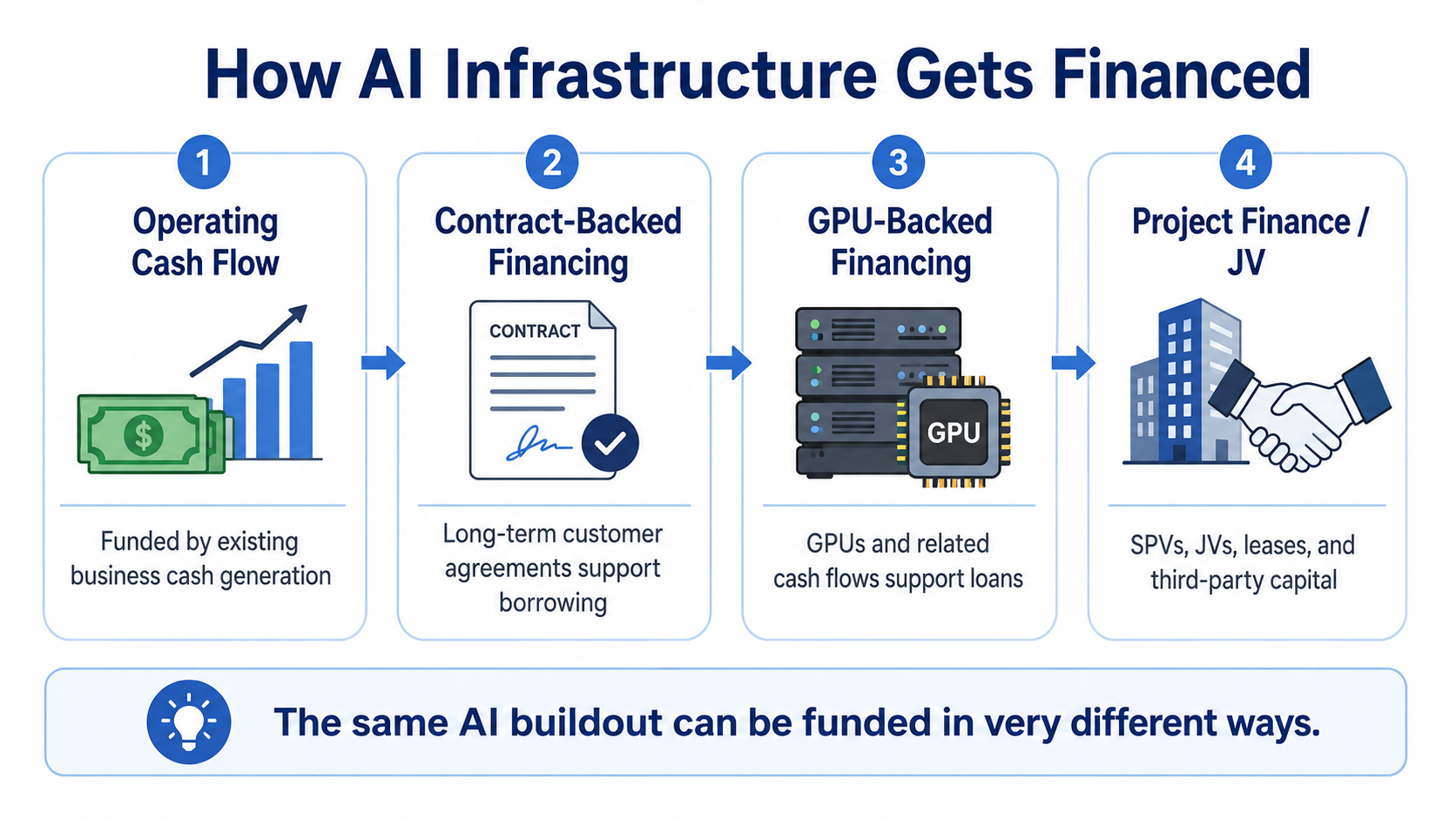

How Does AI Infrastructure Get Financed?

There are several major models.

Cash-flow-funded AI spending

The largest technology companies can often fund AI investment through their existing businesses.

Meta generates large amounts of cash from advertising. Microsoft earns money from software and cloud services. Alphabet generates cash from advertising and cloud computing. Amazon has AWS and its broader commerce business.

These companies can still overinvest, but they are not usually dependent on a single customer or a new financing round just to continue operating.

Contract-backed financing

Some infrastructure companies use long-term customer contracts to support borrowing.

For example, an AI infrastructure provider may sign a multi-year contract with a large customer. Banks or investors may then be willing to lend against the expected future cash flow from that contract.

This can make financing cheaper and help fund large projects.

The risk is customer quality. A contract with Microsoft is very different from a contract with a smaller, loss-making customer that must continue raising capital to pay future bills.

GPU-backed financing

GPUs are increasingly being used as financeable assets.

Companies including CoreWeave, Lambda, Crusoe, and IREN have used GPUs, GPU-related cash flows, customer contracts, or project assets to support debt financing.

This is important because GPUs are no longer only technology equipment. In some financing structures, they also function as collateral.

But GPUs are not real estate. They can become economically outdated much faster as new chip generations improve performance and energy efficiency. That creates a difficult question for lenders: how much will an older GPU still be worth several years from now?

Project finance and joint ventures

Some large AI infrastructure projects are financed through SPVs, joint ventures, leases, or project-level debt.

These structures can bring in outside capital and reduce the amount of money a parent company has to contribute directly.

The key question is what kind of credit support exists. Some projects rely on a strong parent company, long-term leases, customer prepayments, residual-value guarantees, or other forms of protection. Others are more exposed to customer concentration and refinancing risk.

Why Is CoreWeave Important?

CoreWeave is one of the clearest examples of AI infrastructure becoming more dependent on sophisticated financing.

By March 2026, CoreWeave had approximately $25.1 billion of debt principal outstanding. Its financing structures include project-level debt, equipment financing, customer contracts, cloud infrastructure, and data-center leases.

Some CoreWeave financing facilities use project assets and customer contracts as part of the collateral package. Other facilities have brought GPU- and HPC-backed lending into syndicated credit markets.

This matters because the financial chain becomes more connected.

A customer signs a long-term compute contract. CoreWeave raises financing. The financing pays for GPUs and infrastructure. Future contract cash flows are expected to service the debt.

If demand remains strong and customers pay, the system can work well.

If a major customer reduces spending, delays payments, or faces its own financing problems, the pressure may move from the customer to the infrastructure provider and then to lenders.

That is the type of credit transmission investors are trying to understand.

Is OpenAI the Center of the Entire AI Credit System?

No.

OpenAI is important, but it should not be treated as the entire AI industry.

The reason investors study OpenAI is that it combines several unusual characteristics: very rapid growth, very large external financing rounds, major losses, enormous compute commitments, and deep relationships with cloud providers and infrastructure companies.

OpenAI has entered large compute arrangements with companies including Microsoft, Oracle, and CoreWeave. It has also raised extremely large amounts of capital from strategic investors.

That creates an important question: how much of future compute spending will be covered by operating cash flow from products, and how much will depend on new equity financing, strategic investment, prepayments, or additional capital?

Public investors still do not have a complete answer because OpenAI does not publish the same level of audited financial disclosure as a public company.

That uncertainty makes OpenAI a useful stress-test node. It does not prove OpenAI will fail, and it does not mean every AI infrastructure company depends on OpenAI.

What Does “Second Derivative” Mean in the AI Boom?

The term sounds technical, but the idea is simple.

Imagine AI capital spending rises like this:

$100 billion $150 billion $220 billion $300 billion $380 billion

Spending is still growing.

But the important question is whether the growth rate itself is increasing or slowing.

A company or industry can still report higher revenue, more orders, and larger capital spending while the pace of growth begins to weaken.

That matters when companies have already signed long-term contracts, added debt, or built fixed assets based on stronger future growth assumptions.

For investors, the key question is not only whether AI is still growing. It is whether growth remains strong enough to support commitments created during the earlier period of faster expansion.

Why Is Meta Different?

Meta shows why all AI capital spending should not be treated the same way.

Meta has extremely strong operating cash flow from advertising. It is not a company that needs another financing round simply to continue building AI infrastructure.

At the same time, Meta is also using more sophisticated project structures.

Its Hyperion data-center project uses a joint venture in which Blue Owl owns 80% and Meta owns 20%. The structure includes third-party capital, long-term leasing arrangements, and residual-value support.

In July 2026, Meta announced plans to expand Hyperion from 2 gigawatts to 5 gigawatts, with investment expected to exceed $50 billion.

Meta’s stock also rebounded despite the expansion in AI spending.

That is important because it shows the market has not simply moved to a “less CapEx is better” regime.

Investors may still reward large AI investments when they believe the company has strong cash flow, credible monetization, and a better capital structure. Our analysis of Meta’s compute commercialization strategy examines that distinction in more detail.

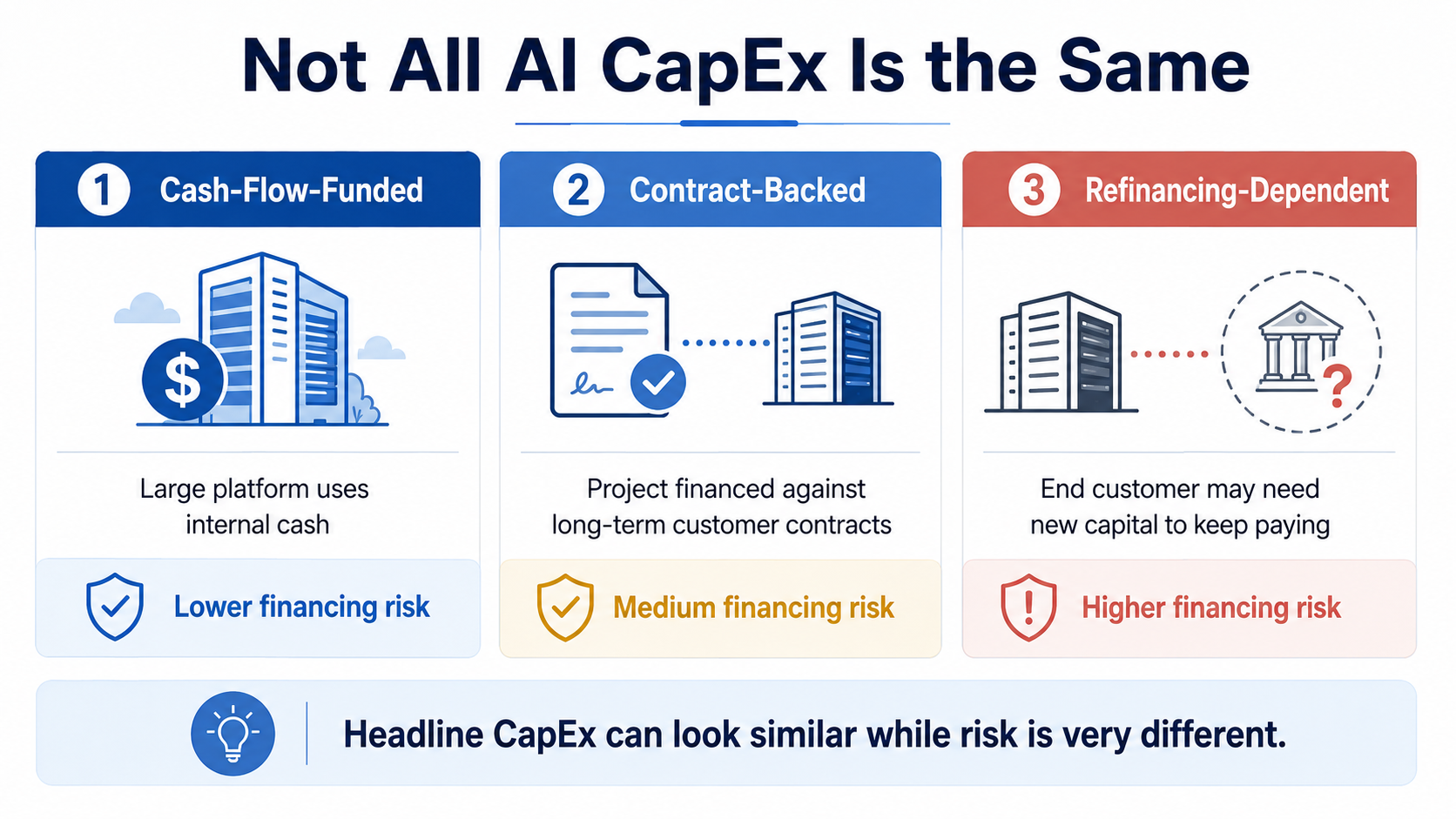

Does More AI CapEx Always Mean More Risk?

No.

Ten billion dollars of AI CapEx can represent very different financial structures.

A company may fund the spending from internal cash flow and already be earning measurable returns from AI.

Another company may finance the project against a long-term contract with an investment-grade customer.

A third company may borrow against a future contract signed by a loss-making customer that still depends on repeated financing rounds.

All three may report $10 billion of capital spending. The risk is not the same.

That is why investors should look beyond the headline CapEx number. Our guide to AI CapEx payback and token-cost economics explains how capital efficiency can change the return profile.

They should ask:

Who provides the capital?

Who owns the assets?

Who guarantees the contract?

Who ultimately makes the payment?

Does the customer generate cash, or does it need new financing to keep paying?

Are GPUs Becoming the Next “Subprime Mortgage”?

That comparison is too strong based on the current evidence.

GPU-backed lending is real. Some loans are rated, syndicated, or supported by customer contracts and project assets.

But there is not yet a mature, standardized GPU securitization market comparable to the U.S. mortgage market before 2008.

There is no broad, well-established market of standardized GPU asset-backed securities with long default histories, uniform residual-value curves, and large repeated issuance programs.

The better conclusion is that GPUs are becoming financeable assets, but the market is still developing.

The risk transmission channels exist. The system has not yet experienced broad failure.

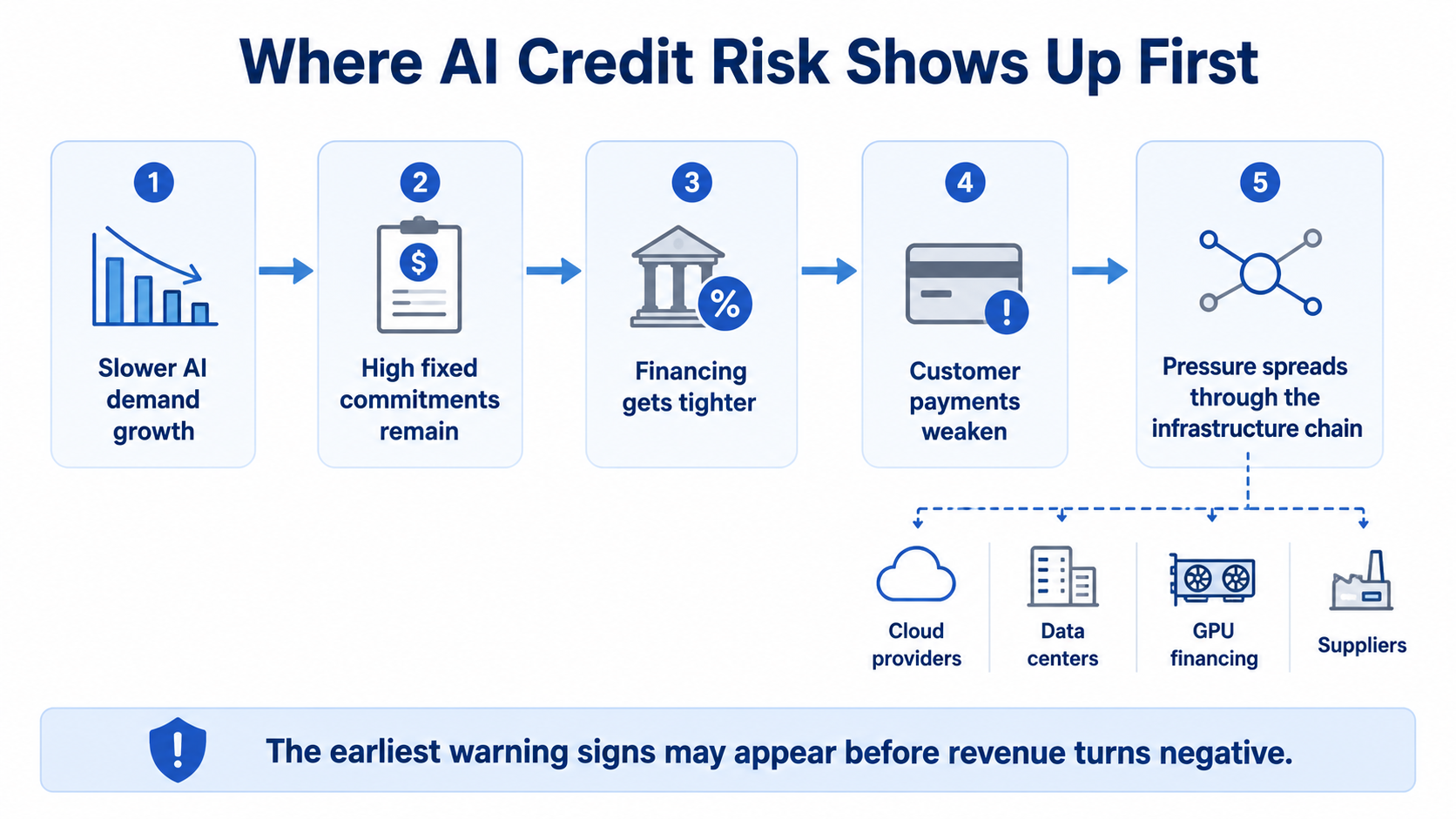

What Would Be a Real Warning Sign for the AI Bubble?

One signal alone would not prove a crisis.

A more serious warning would be several developments happening together.

AI revenue and usage growth begin to slow while capital commitments remain very high. Customers shorten contracts, delay payments, or renegotiate obligations. Project-finance costs rise. Lending standards tighten. GPU utilization or resale values weaken. Neoclouds need increasingly large amounts of new debt to support existing commitments. End customers require bigger financing rounds simply to keep paying for previously contracted capacity.

That combination would be far more important than a single weak quarter or a temporary decline in one AI stock.

So, Is the AI Bubble About to Burst?

Current evidence does not support that conclusion.

AI infrastructure creditization is real. Long-term contracts are supporting asset-level lending. GPUs are being used as collateral or financeable assets. Data centers are being funded through project debt, joint ventures, private credit, and SPVs.

But there is still no broad evidence of widespread defaults, frozen financing markets, forced GPU liquidations, large-scale collateral impairment, or cascading losses across the AI ecosystem.

The more important lesson is that investors may eventually stop treating all AI capital spending as economically equal.

Some companies are investing with operating cash flow and already seeing commercial benefits. Others are financing infrastructure against strong long-term customer contracts. Still others may be exposed to customers whose ability to pay depends on continued access to new capital.

Those structures should not receive the same risk assessment.

The earliest warning signs may appear before AI revenue falls and before GPU orders disappear. They may show up first in customer credit quality, financing costs, contract terms, asset utilization, GPU residual values, and the market’s willingness to distinguish between high-quality AI investment and expansion that depends on the next round of financing.

Key Takeaways

AI demand can be real while financial risk still grows underneath the infrastructure buildout.

GPU-backed lending, project finance, SPVs, private credit, and long-term compute contracts are becoming more important in parts of the AI ecosystem.

Hyperscalers such as Meta, Microsoft, Amazon, and Alphabet still have much stronger internal funding capacity than most neoclouds.

CoreWeave is one of the clearest examples of contract-supported, GPU-linked, asset-level AI infrastructure financing.

OpenAI is important as a stress-test node because it combines very large financing needs with large compute commitments, but it does not represent the entire AI industry.

The most useful question is no longer simply whether AI CapEx is rising. It is what kind of capital supports that spending and who ultimately bears the risk.

Frequently Asked Questions

What is AI infrastructure credit risk?

AI infrastructure credit risk is the possibility that companies building data centers, buying GPUs, or providing compute capacity may struggle to repay debt or meet obligations if customers do not pay as expected or financing conditions tighten.

How are GPUs used in financing?

GPUs can be used as collateral, part of equipment-financing structures, or as assets whose expected cash flows support lending.

Is CoreWeave too leveraged?

CoreWeave has a large debt load and significant future lease obligations, but leverage alone does not prove financial distress. The key variables are customer payment quality, contract performance, refinancing access, utilization, and asset value.

Is OpenAI causing an AI credit bubble?

There is not enough evidence to support that conclusion. OpenAI is an important customer and financing node, but the AI ecosystem is much broader. Its role should be analyzed as part of the network, not treated as the entire system.

Is Meta’s AI spending risky?

Meta’s capital spending is very large, but the company also generates substantial operating cash flow. Its risk profile is different from a company that depends on repeated financing or a small number of customers.

What should investors watch next?

The most important indicators include AI revenue growth, capital-spending growth, financing costs, customer concentration, contract duration, payment quality, GPU utilization, residual values, and whether companies increasingly need new capital to meet existing obligations.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | The Second Derivative: Why No One Understands the AI Boom | Groundbreaker Research | 2026-07-02 | Research essay | Core framework on second derivatives, credit structure, CapEx coordination equilibrium, and OpenAI as a stress-test node. |

| 2 | CoreWeave 2025 Form 10-K | SEC / CoreWeave | 2026-03 | SEC filing | Debt, leases, customer concentration, RPO, committed contracts, and financing structure. |

| 3 | CoreWeave 2026 Q1 Form 10-Q | SEC / CoreWeave | 2026-05 | SEC filing | Debt principal, debt service, capital spending, and current financing exposure. |

| 4 | CoreWeave DDTL 4.0 Overview | CoreWeave | 2026-03-31 | Financing document | Project-level collateral package, customer contract, data-center leases, DSCR, pricing, and non-recourse structure. |

| 5 | CoreWeave DDTL 5.0 credit agreement filing | SEC / CoreWeave | 2026-05-15 | Financing document | Publicly syndicated GPU/HPC-backed lending, pricing, maturity, and use of proceeds. |

| 6 | CoreWeave closes $3.1 billion DDTL 5.0 facility | SEC / CoreWeave | 2026-05-18 | Company financing announcement | Secondary trading, ratings, customer-contract support, and alignment with GPU infrastructure useful life. |

| 7 | Lambda Announces $500M GPU-Backed Facility to Expand Cloud for AI | Lambda / Business Wire | 2024-04-02 | Company financing announcement | GPU-backed special-purpose financing supported by GPU cash flows. |

| 8 | Upper90 closes $225M credit facility to Crusoe | Crusoe | 2025-03-27 | Company financing announcement | GPU asset-backed credit used for NVIDIA GPUs and related cloud infrastructure. |

| 9 | Crusoe secures $750M credit facility from Brookfield | Crusoe | 2025-06-11 | Private credit announcement | Private-credit participation in AI factories, data centers, and AI cloud expansion. |

| 10 | IREN Microsoft-backed project financing | SEC / IREN | 2026-06-01 | SEC filing | Microsoft contract cash flows, GPUs, project assets, DSCR, LTC, and limited parent support used in $3.6B financing. |

| 11 | Applied Digital $2.35B senior secured project notes | SEC / Applied Digital | 2025-11-20 | SEC filing | Project-company secured notes for Polaris Forge 1, including pricing and use of proceeds. |

| 12 | Applied Digital $2.15B senior secured project notes | SEC / Applied Digital | 2026-03-10 | SEC filing | Oracle-leased Polaris Forge 2 financing, lease-linked amortization, and completion guarantee. |

| 13 | Applied Digital $1.59B senior secured project notes | SEC / Applied Digital | 2026-06-16 | SEC filing | ELN-04 project financing, bridge-loan takeout, debt-service reserves, and lease-linked amortization. |

| 14 | Oracle FY2026 Form 10-K | SEC / Oracle | 2026-06 | SEC filing | CapEx, operating cash flow, free cash flow, debt financing, RPO, and customer prepayments. |

| 15 | Oracle fiscal 2026 results and capital funding update | SEC / Oracle | 2026-06 | Earnings disclosure | $638B RPO, $75B of prepaid or customer-supplied hardware, and FY2026/FY2027 funding plans. |

| 16 | Meta announces Hyperion joint venture with Blue Owl Capital | Meta | 2025-10-21 | Company announcement | Blue Owl 80% / Meta 20% ownership, development cost, leases, private securities, and residual-value support. |

| 17 | Meta 2026 Q1 Form 10-Q | SEC / Meta | 2026-04 | SEC filing | Hyperion lease commitments, residual-value guarantee, and project exposure. |

| 18 | Meta expands Louisiana data center to 5 gigawatts, investment crosses $50 billion | Reuters | 2026-07-13 | News | Hyperion expansion from more than 2GW to 5GW and planned investment above $50B. |

| 19 | Meta building cloud business to sell excess AI capacity, Bloomberg News reports | Reuters | 2026-07-01 | News | Potential commercialization of AI compute and contemporaneous stock-market reaction. |

| 20 | OpenAI raises $122 billion to accelerate the next phase of AI | OpenAI | 2026-03-31 | Company announcement | $122B of committed capital and participating strategic investors. |

| 21 | SoftBank execution of bridge facility agreement | SoftBank Group | 2026-03-27 | Financing announcement | $40B one-year unsecured bridge facility primarily supporting OpenAI follow-on investments. |

| 22 | SoftBank execution of second OpenAI investment tranche | SoftBank Group | 2026-07-01 | Financing announcement | $10B July OpenAI equity investment funded through borrowings under the bridge facility. |

| 23 | Morningstar DBRS takeaways on securitizable assets | Morningstar DBRS | 2026 | Rating agency research | GPU useful-life, depreciation, residual-value, and securitization challenges. |

This beginner guide uses primary filings and company financing documents for company-specific claims. The Groundbreaker essay is presented as a framework under examination, not as proof of a systemic AI credit crisis.

Related Reading

Is the AI Bubble About to Break? The Real Risk May Be Hiding in the Credit System

AI demand is still growing, but as GPUs, long-term compute contracts, project finance, and customer credit become more tightly connected, the real risk may be hiding in how the expansion is funded.

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

Meta Does Not Have an AI Compute Glut

Meta Compute is not an AI capex retreat. Meta is still expanding data center capacity while turning AI compute into a flexible asset across ads, models, APIs, and external leasing.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security.

Comments