On July 2, 2026, Groundbreaker Research published a long-form essay titled The Second Derivative: Why No One Understands the AI Boom, offering a view that runs against much of the prevailing market narrative.

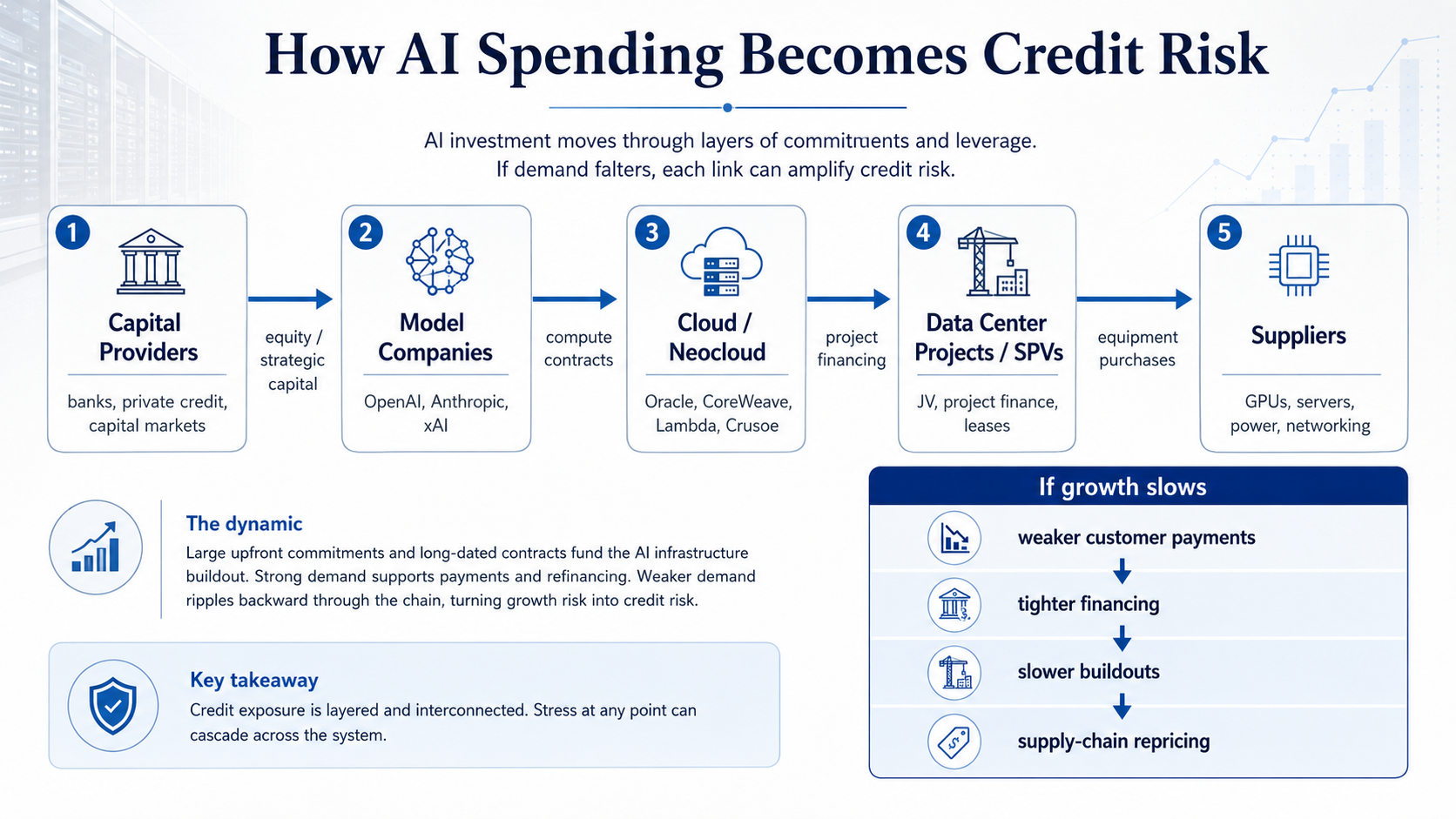

Investors often compare the current AI boom with the dot-com bubble of 2000, focusing on valuations, the survivability of today’s market leaders, and how far stocks could fall if the cycle turns. Groundbreaker argues that this may be the wrong comparison. The more relevant analogy, in its view, is the credit and real-estate expansion that preceded the 2008 financial crisis, because AI infrastructure is increasingly being built through a network of data centers, long-term compute contracts, GPU financing, project-level debt, and claims on future cash flows.

The core concept is the “second derivative.” Markets tend to focus on how large a business or industry has become and how quickly it is growing. Groundbreaker goes one step further and asks whether the growth rate itself is still accelerating or has begun to slow. A capital-spending cycle can remain positive in absolute terms while becoming structurally weaker if previous investment decisions, long-term contracts, and financing arrangements were all based on faster future growth than the system ultimately delivers.

That is the genuinely contrarian part of the argument. The question is not whether AI is real. Demand is clearly real. Chips are still being sold, cloud revenue is still expanding, model capabilities are improving, and hyperscalers continue to raise spending. The more difficult question is whether the financing structure underneath that growth is becoming dependent on a pace of expansion that may not be sustainable indefinitely.

We treated Groundbreaker’s framework as a research hypothesis rather than a conclusion. Over the past several days, we examined neocloud debt, GPU-backed lending, project finance, special-purpose vehicles, private credit, long-term customer contracts, and customer concentration. The result is more complicated than either “AI is the next 2008” or “AI demand is real, therefore there is no financial risk.”

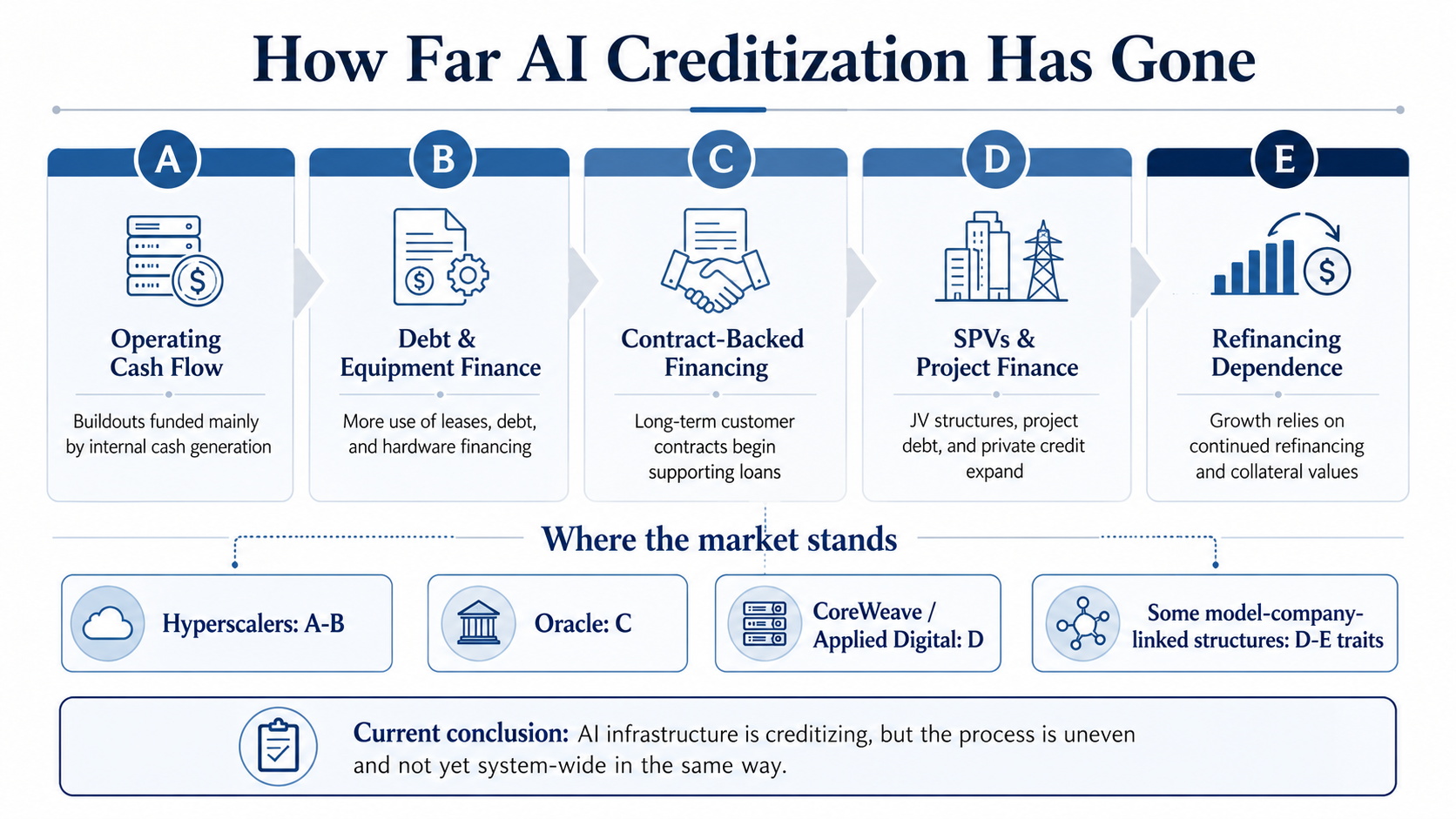

The evidence supports a more nuanced conclusion. AI infrastructure has already begun to undergo a meaningful process of creditization. Long-term customer contracts are being used to support asset-level lending, GPUs are increasingly serving as collateral or financing assets, data-center projects are being funded through SPVs, joint ventures, project debt, and private credit, and some of these loans have already been rated, syndicated, and made tradeable in secondary markets. Yet the process is highly uneven. CoreWeave and several data-center projects have moved deep into asset-level and project-based financing, while Meta, Microsoft, Amazon, and Alphabet still rely primarily on operating cash flow and investment-grade corporate credit.

The channels through which risk could move across companies, contracts, and physical assets now clearly exist. What has not yet occurred is broad evidence that the entire AI complex depends on continuous refinancing simply to remain operational.

That distinction matters.

AI Infrastructure Is No Longer Just Companies Spending Cash on GPUs

If Groundbreaker were merely using a colorful analogy, the argument would be easy to dismiss. What makes the framework worth taking seriously is that public financing documents already show concrete examples of AI infrastructure being financed through increasingly sophisticated credit structures.

CoreWeave is currently the clearest case.

By the end of March 2026, CoreWeave had approximately $25.1 billion of debt principal outstanding. During the first quarter alone, debt-service payments were about $1.8 billion. At the end of 2025, the company also had roughly $38.5 billion of undiscounted future payments tied to leases that had not yet commenced.

More important than the absolute debt load is the structure of the financing. CoreWeave’s DDTL 4.0 facility placed substantially all assets of the relevant project subsidiary, including cloud infrastructure, customer contracts, and data-center leases, into the collateral package. The parent company was generally not subject to ordinary recourse. DDTL 5.0 went further by bringing HPC- and GPU-backed lending into the syndicated market and allowing secondary trading.

At that point, lenders were no longer relying only on CoreWeave’s general corporate credit. They were lending against a package of GPUs, servers, project assets, customer contracts, and expected project cash flows.

This is close to the mechanism Groundbreaker describes: customers commit to long-term compute capacity, cloud providers raise financing against those commitments, the financing funds GPUs and data-center construction, and future contract cash flows are expected to service the debt.

CoreWeave is not an isolated case.

Lambda established a GPU-backed financing vehicle of up to $500 million as early as 2024, supported by GPUs and the cash flows they generate. Crusoe has used GPU asset-backed credit, Brookfield private credit, and data-center joint ventures with Blue Owl. IREN arranged $3.6 billion of financing backed by Microsoft contract cash flows, GPUs, and the assets of the project subsidiary. Applied Digital has issued secured notes through project subsidiaries, with some amortization schedules linked directly to when data-center leases commence.

These are not theoretical constructions. They show that AI infrastructure is becoming part of a broader capital system in which contracts support loans, GPUs function as financeable assets, data centers sit inside project-finance structures, and banks, private-credit funds, infrastructure investors, and capital-markets participants increasingly share the financial burden of expansion.

Groundbreaker is therefore right about one important point: investors can no longer understand the AI buildout by looking only at GPU shipments and total CapEx.

The complication is that this conclusion cannot be applied uniformly across the entire industry.

AI Is Becoming More Financialized, but That Does Not Make the Whole Industry “2008”

There is a fundamental difference between CoreWeave and the major hyperscalers.

Meta, Microsoft, Amazon, and Alphabet have large existing businesses that generate substantial operating cash flow. Their AI investment can be funded through advertising, software, cloud computing, e-commerce, and other mature businesses. Neoclouds are more dependent on external capital, long-term customer commitments, and future project cash flows.

Meta illustrates the distinction particularly well.

In 2025, Meta generated approximately $115.8 billion of operating cash flow and around $43.6 billion of free cash flow. That does not make its AI capital spending risk-free, but it does mean Meta cannot reasonably be described as a company that needs the next financing round simply to keep building.

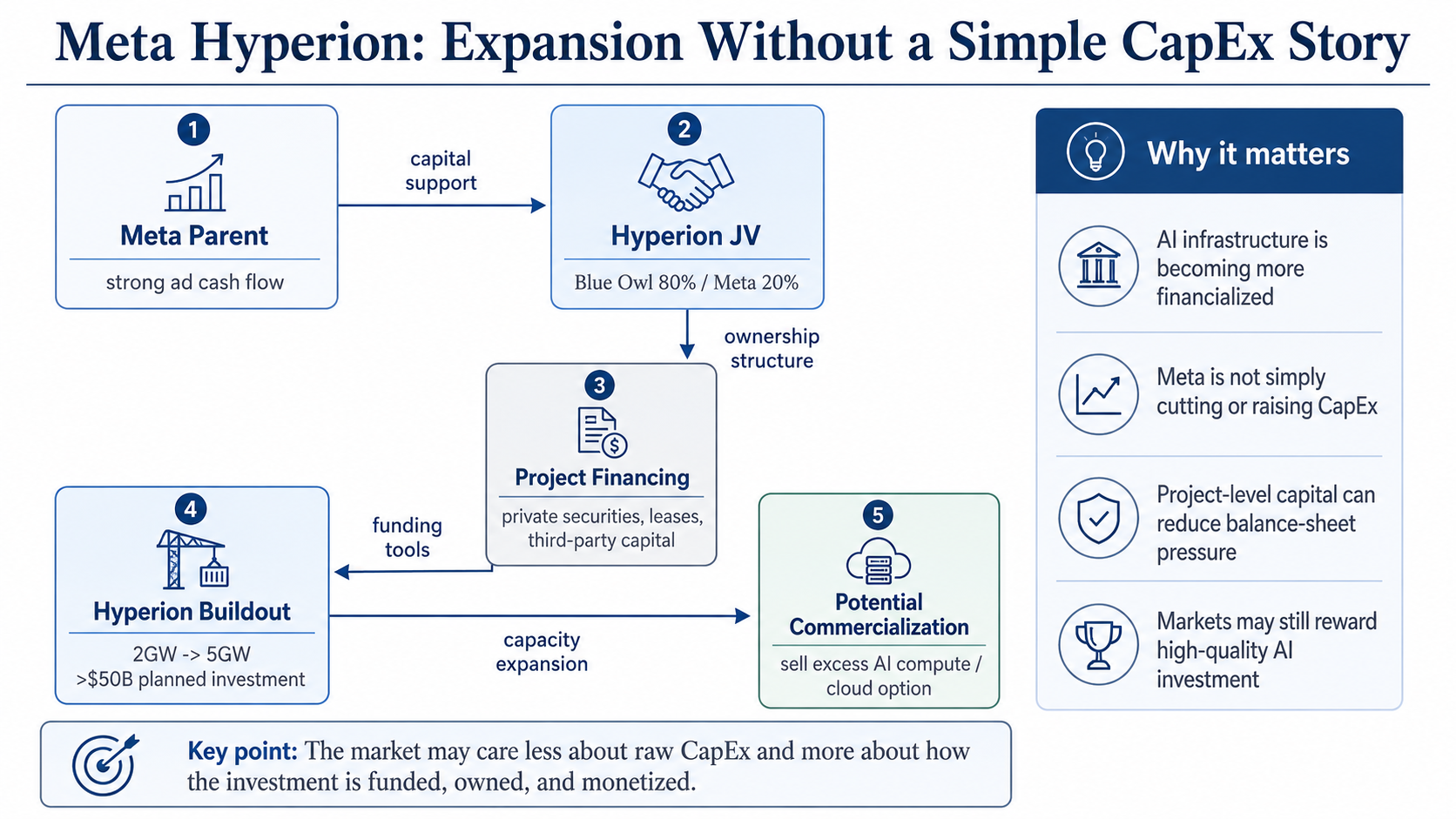

At the same time, Meta is increasingly using sophisticated project-level structures. Hyperion, its large Louisiana data-center project, was placed into a joint venture in which Blue Owl owns 80% and Meta owns 20%. The structure combines private securities, long-term leasing arrangements, and a declining residual-value guarantee of up to roughly $28 billion.

At the project level, Hyperion clearly shows characteristics associated with advanced infrastructure finance. Third-party capital participates in asset ownership, long-term leases support project economics, and Meta’s credit provides protection to external capital through the residual-value guarantee.

For Meta, however, this looks more like capital efficiency and risk allocation than survival financing. The use of a joint venture does not mean Meta depends on refinancing to remain solvent.

That is why there is no single answer to whether AI has become a 2008-style credit bubble. The more accurate answer is that different parts of the industry now sit at very different stages of financial dependence.

The large hyperscaler parents remain primarily supported by operating cash flow and investment-grade corporate credit. Oracle occupies a more complicated middle position because its infrastructure buildout is increasingly tied to long-term AI contracts and external funding, but it still benefits from a large installed software base and recurring cash flow. CoreWeave, Applied Digital, and parts of IREN operate much closer to mature asset-level debt and project-finance structures. OpenAI, Anthropic, and xAI sit at another point in the system entirely: they are potentially important end customers and payment nodes, but their full financial obligations and cash-flow coverage remain difficult to see from the outside.

The better question, therefore, is not how much debt the AI industry uses in aggregate. It is whether the next marginal dollar of AI investment is increasingly being funded by existing cash flow or by claims on future contracts and external financing.

Those may both be called CapEx, but they are not the same risk.

One Dollar of Backlog Can Carry Very Different Credit Quality

Another of Groundbreaker’s most memorable claims is that RPO and backlog should be thought of as a loan book that no one calls a loan book.

The analogy is useful, but taken literally it goes too far.

Remaining performance obligations represent contracted future revenue that has not yet been recognized. A long-term contract with an investment-grade customer that pays in advance can be a very high-quality source of visibility. A contract with a loss-making customer that must complete another financing round before it can continue paying has a very different risk profile.

Oracle provides a useful counterexample to an overly broad interpretation.

In fiscal 2026, Oracle reported roughly $55.7 billion of capital spending, negative free cash flow of about $23.7 billion, and total debt of roughly $156.2 billion. During the same fiscal year, it raised about $43 billion of debt and $5 billion of equity. Its RPO reached approximately $638 billion, with much of the increase coming from large AI contracts.

At first glance, that appears to support Groundbreaker’s narrative perfectly: enormous future contracts are being used to justify enormous infrastructure spending.

But Oracle also disclosed that approximately $75 billion of those arrangements involved customer prepayments or customer-supplied GPUs. For that portion of the business, Oracle is not simply fronting all the capital and waiting for an uncertain customer to pay years later.

The right conclusion is therefore not that RPO is debt in disguise. The more useful question is whether each dollar of backlog carries the same probability of payment and the same degree of financing dependence.

It does not.

A $10 billion contract could be backed by an advance payment. It could be supported by a customer with substantial recurring cash flow. It could depend on a loss-making customer with a strategic backer or parent guarantee. Or it could rely on a customer that must repeatedly access equity or debt markets to meet its obligations.

Financial statements usually present all of these arrangements as backlog or RPO. That headline number alone does not tell investors the underlying credit quality.

This suggests a more useful concept for AI infrastructure research: risk-weighted backlog.

Instead of focusing only on total contracted value, investors should examine who the customer is, whether the customer is profitable, whether there are advance payments, whether a parent guarantee exists, whether contracts can be delayed or terminated, and whether the customer itself depends on fresh financing to perform.

That moves the discussion beyond whether demand exists and toward whether the demand has durable payment capacity.

Why OpenAI Matters: It Concentrates Growth, Losses, Financing, and Compute Commitments in One Place

OpenAI should not be treated as the center of the entire AI industry, nor should every infrastructure risk be reduced to what happens to one company.

It does matter, however, because it concentrates several of the most important credit variables in a single entity: rapid growth, large-scale external financing, ongoing losses, enormous compute commitments, and a dense network of cross-investment relationships.

Public disclosures show that OpenAI’s 2026 funding round involved $122 billion of committed capital. SoftBank also used one-year unsecured bridge financing to fund $10 billion equity investments in OpenAI in both April and July 2026. At the same time, OpenAI has entered into very large compute arrangements with companies including Oracle, CoreWeave, and Microsoft.

That creates a real financial transmission path. Capital flows into a model company. The model company commits to future cloud spending. Cloud providers finance infrastructure on the basis of long-term contracts. Data-center and project companies buy GPUs, servers, power capacity, and networking equipment.

None of this proves that demand is artificial.

OpenAI may have substantial real product revenue, growing usage, and durable demand. The harder problem is that public markets still cannot fully determine how much of its future compute spending will ultimately be covered by product cash flow, customer prepayments, equity financing, strategic investment, or new capital inflows.

That uncertainty is why OpenAI is relevant as a stress-test node.

The AI ecosystem increasingly includes cross-investment relationships that blur the traditional separation between customers, suppliers, and capital providers. A chip supplier may invest in a model company that buys compute built around that supplier’s hardware. A cloud provider may invest in a model company that then pays for cloud services. An infrastructure provider may borrow against a long-term contract whose end customer is itself dependent on fresh financing.

These relationships do not prove that demand is fake. They do make it more important to identify where the ultimate external cash flow comes from.

At the same time, the existence of financing dependence does not justify concluding that OpenAI will fail or that the entire AI industry will experience a credit crisis. The evidence currently shows that transmission channels exist. It does not show that a systemic credit event has begun.

The Real Value of the “Second Derivative” Is That Positive Growth Can Still Be Too Slow

The strongest part of Groundbreaker’s argument remains the second-derivative framework.

A company growing revenue at 40% may appear exceptionally healthy. But if it previously signed long-term contracts, expanded fixed costs, raised debt, and built infrastructure on the assumption of 70% growth, then 40% may still be insufficient.

The important question is not simply whether demand is growing. It is whether actual growth remains high enough to support obligations created during a period of faster expansion.

This is especially relevant for capital-intensive AI infrastructure. GPUs, servers, power, and data centers require capital up front, while financial returns arrive over time. If capital commitments consistently grow faster than end-market revenue and cash flow, the system must eventually depend on greater amounts of new capital.

Still, CapEx growth alone is not enough to diagnose stress.

A slowdown in capital spending can be positive if better chips, lower token costs, and higher utilization allow companies to generate more revenue with less incremental investment. The same slowdown can be negative if demand weakens, utilization falls, and depreciation, interest expense, and fixed contractual payments remain elevated.

The dangerous combination is more specific: demand growth begins to slow, capital commitments remain high, and the system becomes increasingly reliant on debt, long-term contracts, weaker counterparties, or more complex financing structures to sustain expansion.

That is a more useful way to apply the second-derivative idea.

Meta Is Already Complicating One of Groundbreaker’s Most Important Predictions

Groundbreaker argues that the AI capital-spending race may function as a coordination equilibrium. As long as markets reward higher AI spending, management teams have little incentive to be the first to slow down. The true turning point, in this framework, would come when the first major technology company cuts AI CapEx and its stock rises, signaling that the market’s reward function has shifted from expansion toward capital discipline.

The idea is compelling. Meta’s recent behavior, however, suggests that reality may be more complicated than a simple choice between spending more and spending less.

On July 13, Meta announced that the planned capacity of its Hyperion data center in Louisiana would increase from 2 gigawatts to 5 gigawatts, taking the expected project investment above $50 billion. The company has also indicated that it intends to increase total compute capacity substantially and expand its use of internally designed AI chips.

At the same time, Meta’s stock has rebounded. The market has not treated the expansion of AI spending as automatically negative. That is important because it suggests investors have not yet shifted to a simple “less CapEx is better” regime.

Meta is also reportedly exploring a cloud business that would sell excess AI computing capacity. Combined with the Hyperion joint venture, the picture is more complex than a company merely accelerating or cutting spending. Meta is expanding its internal compute base, considering the external commercialization of some capacity, and using project-level financing structures to change who contributes capital, who owns assets, and who bears residual-value risk.

That both supports and modifies Groundbreaker’s thesis.

It supports the thesis because even a cash-generative company such as Meta is using joint ventures, private securities, leasing arrangements, and credit support to finance AI infrastructure. That confirms that the buildout is becoming more financialized.

It modifies the thesis because the market is clearly not yet rewarding capital restraint in a uniform way. At least for Meta, higher AI investment can still coexist with a rising stock price.

The more important distinction may therefore be not between high and low CapEx, but between different qualities of CapEx.

Ten Billion Dollars of AI CapEx Can Mean Three Very Different Things

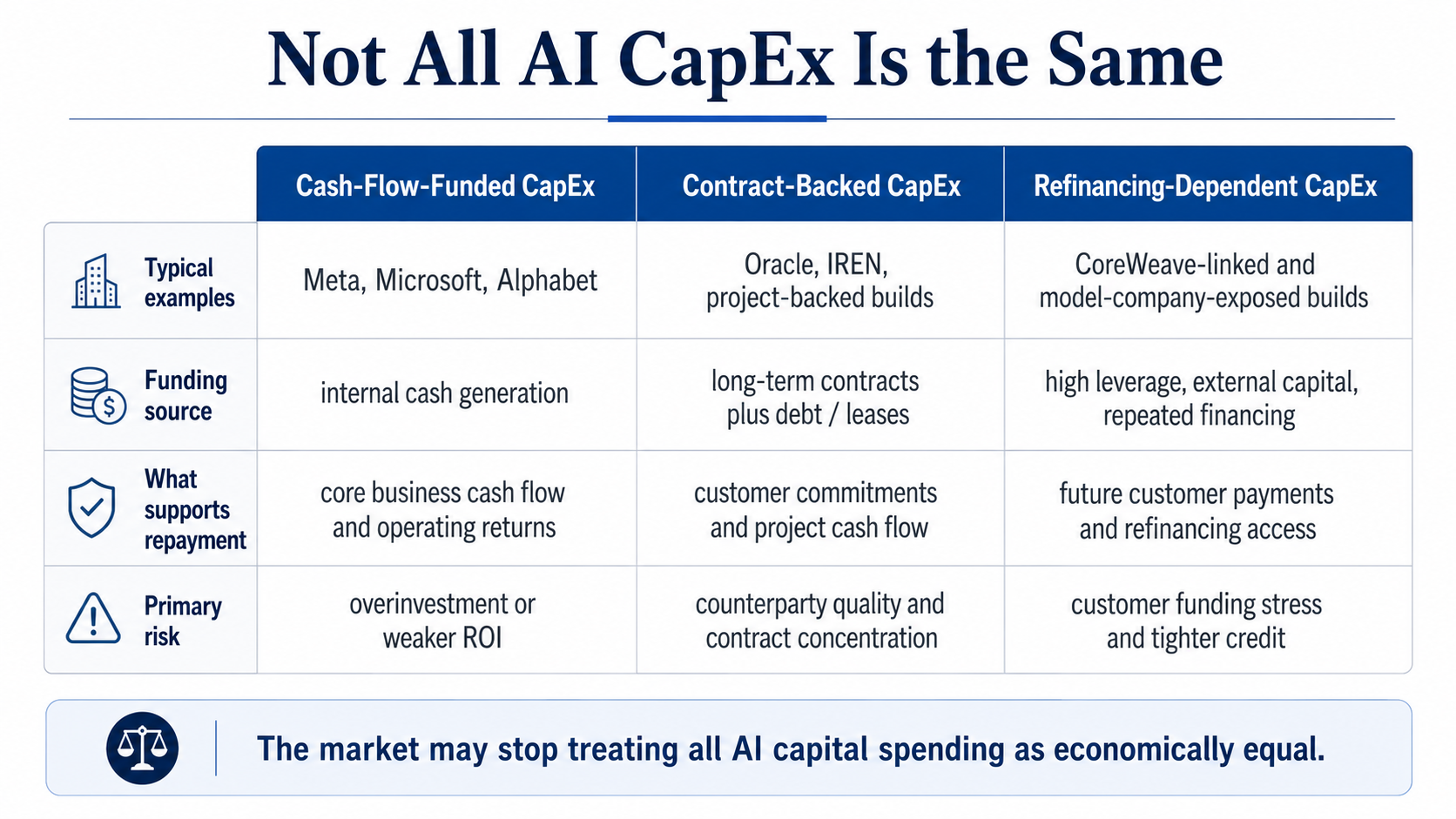

Consider three companies that each announce an additional $10 billion of AI capital spending.

The first has strong operating cash flow, and its core business is already benefiting from better advertising performance, higher cloud revenue, or lower costs as a result of AI. It can finance the investment largely from internal cash generation and can point to measurable commercial returns.

The second relies on a long-term contract with an investment-grade customer to obtain project financing. The capital expenditure is supported by visible contractual cash flow from a strong counterparty.

The third also builds $10 billion of infrastructure, but its ultimate customer is still unprofitable and depends on repeated financing rounds to fulfill long-term commitments. The infrastructure provider then borrows against the future contract to buy GPUs.

All three appear in financial statements as $10 billion of CapEx. The risk embedded in each is very different.

That is why the second-derivative framework should be extended. Investors should track at least three separate dimensions.

The first is demand acceleration: whether AI revenue, token usage, and genuine external demand continue to grow.

The second is capital acceleration: whether CapEx, GPU purchases, and data-center construction continue to expand.

The third is credit quality: whether the next dollar of investment increasingly requires higher leverage, more complex SPVs, weaker end customers, or more capital circulating within the AI ecosystem itself.

If demand remains strong, operating cash flow catches up with investment, and asset utilization improves, large CapEx does not necessarily imply financial fragility.

If demand growth slows while fixed commitments remain elevated and the next phase of expansion increasingly depends on debt or customers that themselves require fresh financing, risk can rise even before reported revenue turns negative.

That may be the more important second derivative for the AI cycle.

GPUs Are Becoming Financial Assets, but There Is No Mature “AI Subprime” Market Yet

One obvious challenge to the 2008 analogy is scale and transmission. Does today’s AI infrastructure market really have a large enough credit mechanism to create systemic contagion?

The evidence increasingly suggests that the answer is “partially.”

CoreWeave, Lambda, Crusoe, and IREN have all used GPUs or GPU-related cash flows to support financing. CoreWeave’s loans have been rated, syndicated, and made available for secondary trading. IREN has placed Microsoft contract cash flows, GPUs, and project assets inside the same secured financing structure.

GPUs are therefore no longer only computing equipment. In some parts of the market, they have become assets capable of supporting credit creation.

That said, the market is still far from the scale and standardization of U.S. mortgage securitization before 2008. There is no large, mature market of standardized GPU ABS with broad issuance histories, deep default datasets, uniform residual-value curves, and repeated securitization programs.

The short technology life of GPUs also creates a difficult underwriting problem. A graphics processor can depreciate economically much faster than real estate, especially when newer generations deliver materially better performance per watt or per dollar. Lenders therefore tend to rely on a combination of customer cash flows, conservative loan-to-cost ratios, debt-service coverage tests, staged draws, restricted cash arrangements, and equipment remarketing rights rather than on expected resale value alone.

The safer conclusion is that the financial transmission infrastructure is emerging, but the market has not yet become an AI equivalent of the pre-2008 mortgage complex.

The channels are nevertheless real. Customer credit can affect contracts. Contracts can affect project cash flow. Project cash flow can affect debt coverage and refinancing. Financing conditions can affect GPU purchases and data-center construction. Those changes can eventually move upstream into chips, networking, memory, power, cooling, and other parts of the supply chain.

The chain exists.

It has not yet broken.

The Real Warning Sign Is Not the Disappearance of AI Demand

There is currently insufficient evidence to conclude that AI demand is collapsing or that major AI infrastructure financing markets have shut down.

Meta is expanding Hyperion to 5 gigawatts and more than $50 billion of investment. CoreWeave continues to access GPU-backed financing. Data-center projects continue to attract project debt and private capital.

A direct conclusion that the AI bubble is about to burst would therefore go beyond the evidence.

The opposite conclusion would also be too comfortable. Real demand does not eliminate capital-allocation risk. Industries can experience genuine structural growth while individual companies overinvest, overborrow, misprice contracts, or rely too heavily on customers with weaker payment capacity.

The warning signs would become more meaningful if several developments occurred at the same time: AI revenue and usage growth slow materially while capital commitments remain elevated; customers shorten contracts, delay payments, or renegotiate obligations; project-finance costs rise and lending standards tighten; GPU utilization or residual values deteriorate; neoclouds become increasingly dependent on new debt to support existing commitments; or end customers require progressively larger financing rounds simply to keep paying for previously contracted capacity.

A single one of these signals would not prove a crisis. A cluster of them would materially strengthen Groundbreaker’s case.

So, Is the AI Bubble About to Break?

The current evidence does not support that conclusion.

AI infrastructure creditization is real. Long-term contracts are already supporting asset-level lending. GPUs are being used as collateral or financed assets. Data centers are being funded through SPVs, JVs, project debt, and private credit. CoreWeave, Lambda, Crusoe, IREN, and Applied Digital provide direct evidence, while Meta’s Hyperion shows that project-level financial engineering has reached the largest technology companies as well.

A systemic credit crisis, however, has not occurred. There is no broad evidence of widespread defaults, frozen financing markets, forced GPU liquidations, large-scale collateral impairment, or cascading losses across the sector.

The more important conclusion is that the market may eventually stop treating all AI CapEx as economically equivalent.

Some companies are investing with operating cash flow and already seeing measurable commercial benefits. Others are financing infrastructure against long-term contracts with investment-grade customers. Still others are exposed to end customers whose payment capacity may depend on continued access to new capital.

Those structures may look similar when aggregated into industry-wide CapEx figures, but they should not receive the same risk assessment.

Groundbreaker’s most useful contribution is therefore not a prediction that an AI crash is imminent. It is the insistence that investors follow the financial architecture underneath real demand: where the money comes from, how contracts are financed, who ultimately pays, and whose balance sheet absorbs the loss if growth slows.

That may be the better way to think about the next phase of the AI cycle. The earliest warning signs may appear before AI revenue falls and before GPU orders disappear. They may emerge first in customer credit quality, financing costs, contractual terms, utilization, residual values, and the market’s willingness to distinguish between high-quality AI investment and expansion that depends on the next round of financing.

Frequently Asked Questions

Is the AI bubble about to burst?

Current evidence does not show a systemic AI credit crisis, but the financing structure behind AI infrastructure is becoming more complex and increasingly dependent on long-term contracts, project finance, and external capital in some parts of the market.

How is AI infrastructure becoming credit-driven?

GPU-backed loans, contract-supported project finance, SPVs, JVs, private credit, and data-center secured debt are increasingly being used to fund AI infrastructure expansion.

Why is CoreWeave important in the AI credit cycle?

CoreWeave is one of the clearest examples of AI infrastructure financed through GPUs, customer contracts, data-center leases, project subsidiaries, and syndicated debt.

Why does Meta matter to the AI CapEx debate?

Meta combines strong internal cash generation with increasingly sophisticated project-level financing. Its Hyperion expansion shows that large AI investment can still be rewarded by markets when the capital structure and commercialization path appear stronger.

What is the biggest warning sign for an AI credit downturn?

The strongest warning would be a cluster of signals: slower AI demand growth, high fixed commitments, tighter financing, weaker customer payments, falling GPU utilization or residual values, and increasing dependence on new capital to meet existing obligations.

Sources

| No. | Source | Publisher | Date | Type | What it supports |

|---|---|---|---|---|---|

| 1 | The Second Derivative: Why No One Understands the AI Boom | Groundbreaker Research | 2026-07-02 | Research essay | Core framework on second derivatives, credit structure, CapEx coordination equilibrium, and OpenAI as a stress-test node. |

| 2 | CoreWeave 2025 Form 10-K | SEC / CoreWeave | 2026-03 | SEC filing | Debt, leases, customer concentration, RPO, committed contracts, and financing structure. |

| 3 | CoreWeave 2026 Q1 Form 10-Q | SEC / CoreWeave | 2026-05 | SEC filing | Debt principal, debt service, capital spending, and current financing exposure. |

| 4 | CoreWeave DDTL 4.0 Overview | CoreWeave | 2026-03-31 | Financing document | Project-level collateral package, customer contract, data-center leases, DSCR, pricing, and non-recourse structure. |

| 5 | CoreWeave DDTL 5.0 credit agreement filing | SEC / CoreWeave | 2026-05-15 | Financing document | Publicly syndicated GPU/HPC-backed lending, pricing, maturity, and use of proceeds. |

| 6 | CoreWeave closes $3.1 billion DDTL 5.0 facility | SEC / CoreWeave | 2026-05-18 | Company financing announcement | Secondary trading, ratings, customer-contract support, and alignment with GPU infrastructure useful life. |

| 7 | Lambda Announces $500M GPU-Backed Facility to Expand Cloud for AI | Lambda / Business Wire | 2024-04-02 | Company financing announcement | GPU-backed special-purpose financing supported by GPU cash flows. |

| 8 | Upper90 closes $225M credit facility to Crusoe | Crusoe | 2025-03-27 | Company financing announcement | GPU asset-backed credit used for NVIDIA GPUs and related cloud infrastructure. |

| 9 | Crusoe secures $750M credit facility from Brookfield | Crusoe | 2025-06-11 | Private credit announcement | Private-credit participation in AI factories, data centers, and AI cloud expansion. |

| 10 | IREN Microsoft-backed project financing | SEC / IREN | 2026-06-01 | SEC filing | Microsoft contract cash flows, GPUs, project assets, DSCR, LTC, and limited parent support used in $3.6B financing. |

| 11 | Applied Digital $2.35B senior secured project notes | SEC / Applied Digital | 2025-11-20 | SEC filing | Project-company secured notes for Polaris Forge 1, including pricing and use of proceeds. |

| 12 | Applied Digital $2.15B senior secured project notes | SEC / Applied Digital | 2026-03-10 | SEC filing | Oracle-leased Polaris Forge 2 financing, lease-linked amortization, and completion guarantee. |

| 13 | Applied Digital $1.59B senior secured project notes | SEC / Applied Digital | 2026-06-16 | SEC filing | ELN-04 project financing, bridge-loan takeout, debt-service reserves, and lease-linked amortization. |

| 14 | Oracle FY2026 Form 10-K | SEC / Oracle | 2026-06 | SEC filing | CapEx, operating cash flow, free cash flow, debt financing, RPO, and customer prepayments. |

| 15 | Oracle fiscal 2026 results and capital funding update | SEC / Oracle | 2026-06 | Earnings disclosure | $638B RPO, $75B of prepaid or customer-supplied hardware, and FY2026/FY2027 funding plans. |

| 16 | Meta announces Hyperion joint venture with Blue Owl Capital | Meta | 2025-10-21 | Company announcement | Blue Owl 80% / Meta 20% ownership, development cost, leases, private securities, and residual-value support. |

| 17 | Meta 2026 Q1 Form 10-Q | SEC / Meta | 2026-04 | SEC filing | Hyperion lease commitments, residual-value guarantee, and project exposure. |

| 18 | Meta expands Louisiana data center to 5 gigawatts, investment crosses $50 billion | Reuters | 2026-07-13 | News | Hyperion expansion from more than 2GW to 5GW and planned investment above $50B. |

| 19 | Meta building cloud business to sell excess AI capacity, Bloomberg News reports | Reuters | 2026-07-01 | News | Potential commercialization of AI compute and contemporaneous stock-market reaction. |

| 20 | Meta market coverage: AI cloud plans | Barron's | 2026-07 | Financial media | Supplementary market-reaction context; Reuters is used for the article's verified stock-reaction statement because the exact Barron's article permalink was not stably indexed. |

| 21 | OpenAI raises $122 billion to accelerate the next phase of AI | OpenAI | 2026-03-31 | Company announcement | $122B of committed capital and participating strategic investors. |

| 22 | SoftBank execution of bridge facility agreement | SoftBank Group | 2026-03-27 | Financing announcement | $40B one-year unsecured bridge facility primarily supporting OpenAI follow-on investments. |

| 23 | SoftBank execution of second OpenAI investment tranche | SoftBank Group | 2026-07-01 | Financing announcement | $10B July OpenAI equity investment funded through borrowings under the bridge facility. |

| 24 | Morningstar DBRS takeaways on securitizable assets | Morningstar DBRS | 2026 | Rating agency research | GPU useful-life, depreciation, residual-value, and securitization challenges. |

Primary filings and company financing documents support the core credit-structure claims. Reuters is used for the July 2026 Meta developments; the Groundbreaker essay is treated as the hypothesis being tested, not as proof of the article's conclusions.

Related Reading

Can AI CapEx Pay Off? Start With Token Cost, Then Watch the Payback Period.

Nvidia is showing that the unit cost of AI production is falling. Investors are asking whether cheaper tokens can turn into visible profits and free cash flow fast enough.

Meta Does Not Have an AI Compute Glut

Meta Compute is not an AI capex retreat. Meta is still expanding data center capacity while turning AI compute into a flexible asset across ads, models, APIs, and external leasing.

Micron Is Trying to Escape the Memory Cycle. The Real Test Begins After 2027.

Micron’s AI memory boom is no longer just about one strong quarter. The real question is whether Strategic Customer Agreements, HBM demand, and record capex can turn a memory cycle into a more predictable AI infrastructure business.

Invest better with thoughtful research.

Join readers who receive our best ideas and insights straight to their inbox.

Disclosure

This article is for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security.

Comments